Global Wireless Charging Market Research Report – Segmentation by Technology (Inductive Charging, Resonant Charging, Radio Frequency (RF) Based Charging, Microwave/Infrared Charging); by Application (Consumer Electronics, Automotive, Healthcare, Industrial); by Industry Vertical (Automotive Industry, Healthcare Sector, Consumer Electronics Manufacturers, Industrial & Defense Sectors); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-98

Format:

Region: Global

Market Size and Overview:

The Wireless Charging Market was valued at USD 26.10 billion in 2024 and is projected to reach a market size of USD 114.33 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 34.37%.

The wireless charging market encompasses technologies that enable the transfer of power from a charging source to a device without physical connectors or cables. It primarily relies on electromagnetic fields to deliver energy, with inductive and resonant charging being the most widely used methods. This market serves a broad range of applications across consumer electronics, automotive, healthcare, and industrial sectors. In consumer electronics, wireless charging is commonly integrated into smartphones, smartwatches, earbuds, and tablets. The automotive sector has adopted wireless charging for both in-cabin device charging and electric vehicle (EV) power systems.

In healthcare, wireless power is used for charging implanted medical devices and equipment that require sealed systems. Industrial uses include robotics, drones, and tools in environments where wired connections are impractical or hazardous. Key players in this market include technology providers, hardware manufacturers, and automotive OEMs. The ecosystem also involves standardization bodies like the Wireless Power Consortium, which promotes interoperability through standards like Qi. As innovation continues, new technologies such as long-range RF charging and integrated smart surfaces are emerging to broaden the potential of wireless power delivery.

Key Market Insights:

As of 2023, over 50% of flagship smartphones from major brands like Apple, Samsung, and Google supported wireless charging. The Qi standard has been adopted by over 900 devices, making it the most widely used protocol. Consumer electronics account for more than 60% of all wireless charging-enabled devices sold globally.

By 2023, more than 100 car models included wireless charging pads for in-cabin devices. Automakers such as BMW, Audi, and Hyundai began piloting wireless EV charging systems, with test deployments offering 3–11 kW of wireless power. Wireless EV charging remains niche but is projected to grow significantly as infrastructure evolves.

Wireless charging reduces contamination risks in medical settings by eliminating exposed connectors. Over 70% of new implantable devices under FDA trials by 2023 featured wireless power capabilities. This technology is especially valuable for sealed devices like pacemakers and insulin pumps that require long-term power access without physical ports.

China, South Korea, and Japan collectively manufacture over 60% of the world's wireless charging hardware. These countries have also seen rapid consumer adoption, driven by strong mobile ecosystems and fast-paced innovation cycles. Government-supported R&D initiatives in China have accelerated commercial deployment, especially in urban mobility.

While the Qi standard dominates the market, interoperability issues still exist between brands and charging platforms. Less than 30% of wireless chargers support fast charging above 15W across multiple device ecosystems. The emergence of newer standards like Qi2 aims to address alignment, speed, and cross-device compatibility limitations.

Wireless Charging Market Drivers:

Rising Adoption of Wireless Charging in Consumer Electronics

The widespread integration of wireless charging in smartphones, smartwatches, and earbuds is a major driver of market growth. Leading brands like Apple and Samsung have made wireless charging a standard feature in their flagship devices, encouraging consumers to expect this functionality. As the number of connected devices per user increases, so does demand for convenient, clutter-free charging solutions.

Expansion of Electric Vehicles (EVs) and Smart Mobility Solutions

Wireless charging is gaining momentum in the EV sector, where convenience and automation are crucial for adoption. Automakers and infrastructure providers are piloting wireless EV charging pads for both residential and public use. These systems eliminate the need for physical connectors, reducing wear and making charging more accessible for autonomous or fleet vehicles.

Advancements in Charging Efficiency and Standards

Recent improvements in resonant and RF-based wireless charging technologies have increased energy transfer efficiency and range. New standards like Qi2 aim to unify the market and improve compatibility across devices, driving greater consumer trust and adoption. As these innovations reduce heat loss and charging time, they make wireless power a more viable alternative to traditional wired solutions.

Wireless Charging Market Restraints and Challenges:

Lower Charging Efficiency Compared to Wired Solutions

Wireless charging typically delivers 60–80% efficiency, whereas wired charging often exceeds 90%. This energy loss results in longer charging times and increased heat generation, which can affect both performance and device lifespan. For high-power applications like laptops or electric vehicles, this inefficiency remains a major barrier.

Limited Interoperability and Standard Fragmentation

Although the Qi standard is dominant, many devices and chargers still face compatibility issues, especially with fast charging capabilities. Proprietary technologies used by some manufacturers can restrict users to brand-specific accessories. This lack of universal functionality slows adoption and increases consumer confusion.

High Cost of Infrastructure and Integration

Wireless charging modules and systems are generally more expensive to manufacture and install than traditional wired alternatives. In sectors like automotive and public infrastructure, costs related to alignment mechanisms, embedded coils, and safety systems add significant overhead. For many businesses and municipalities, the return on investment is not yet compelling.

Wireless Charging Market Opportunities:

The wireless charging market presents several compelling opportunities across industries. One major opportunity lies in next-generation consumer electronics, where integration with laptops, smart home devices, and AR/VR headsets is expected to increase. As Qi2 and similar standards mature, they will enable faster, safer, and more efficient charging, improving user experience and accelerating adoption. The electric vehicle (EV) segment offers a high-potential growth area, particularly with autonomous fleets and smart city infrastructure where hands-free charging is essential.

There is also a strong opportunity in healthcare, where wireless charging supports sealed, sterilizable medical devices and implants, reducing infection risk. In the industrial sector, wireless power can improve safety and uptime for robots, drones, and tools used in hazardous environments. Retail and hospitality spaces are adopting wireless charging tables and stations to enhance customer experience and dwell time. Emerging long-range wireless technologies, such as RF or infrared-based charging, could unlock use cases for IoT devices and smart sensors that operate without battery replacements. Furthermore, developing regions offer untapped markets where wireless solutions can help leapfrog unreliable power infrastructure. With the continued miniaturization and cost reduction of components, wireless power could soon become embedded into furniture, vehicles, and public environments, transforming how energy is accessed.

Wireless Charging Market Segmentation:

Market Segmentation: by Technology

• Inductive Charging

• Resonant Charging

• Radio Frequency (RF) Based Charging

• Microwave/Infrared Charging

Inductive charging is the most mature and widely adopted wireless charging method, using magnetic fields between closely aligned coils to transfer energy. It is commonly found in smartphones, smartwatches, and toothbrushes due to its safety, efficiency (typically 70–80%), and simplicity. However, it requires tight alignment and close proximity between the transmitter and receiver, limiting mobility. This segment accounts for approximately 70% of the overall wireless charging market.

Resonant charging uses magnetic resonance to transfer energy over greater distances and with more spatial freedom than inductive systems. It allows for multiple devices to be charged simultaneously and can tolerate misalignment between the charging surface and the device. This method is well-suited for electric vehicles, tablets, and industrial tools. It represents about 20% of the market share.

Market Segmentation: by Application

• Consumer Electronics

• Automotive

• Healthcare

• Industrial

Consumer electronics is the largest application segment for wireless charging, driven by widespread adoption in smartphones, smartwatches, wireless earbuds, and tablets. Major brands like Apple, Samsung, and Xiaomi have integrated wireless charging across their premium product lines, encouraging ecosystem-wide growth. Charging pads, docks, and furniture-integrated solutions are now common in homes, offices, and public spaces. This segment accounts for approximately 65% of the total wireless charging market.

Wireless charging in the automotive industry is growing in two key areas: in-cabin wireless charging for devices and wireless power transfer for electric vehicles (EVs). While in-cabin solutions are already standard in many premium models, EV wireless charging is still in the early adoption phase, with pilot projects underway from manufacturers like BMW, Hyundai, and Tesla. The technology improves convenience, especially for autonomous and fleet vehicles, by eliminating the need for physical plugs. This segment contributes about 20% of the market.

Market Segmentation: by Industry Vertical

• Automotive Industry

• Healthcare Sector

• Consumer Electronics Manufacturers

• Industrial & Defense Sectors

Wireless charging in the automotive industry is primarily used for in-car device charging and emerging electric vehicle (EV) wireless charging systems. Automakers are integrating wireless pads into vehicle consoles to improve user convenience, while some are developing infrastructure for dynamic and stationary EV charging. This segment is gaining traction as EV adoption rises and automakers seek to differentiate with tech-friendly interiors. This segment holds approximately 20% of the wireless charging market share.

Consumer Electronics is the largest segment, with wireless charging being widely adopted in smartphones, smartwatches, earbuds, and tablets. Major brands are standardizing Qi-based wireless charging in flagship devices, driving both consumer demand and third-party accessory development. The convenience of cable-free charging has made it a key differentiator in consumer tech. This segment commands approximately 65% of the wireless charging market.

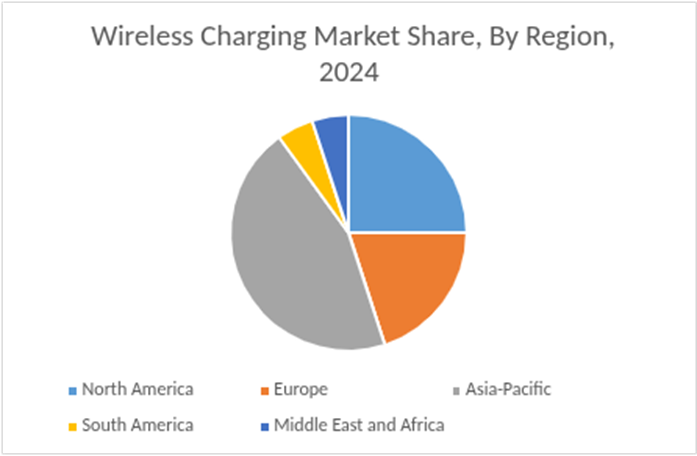

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is a mature market driven by high adoption of consumer electronics and strong investments in electric vehicles and healthcare technologies. The presence of key tech players and early adoption of wireless charging standards contribute to steady growth. Government incentives for EV infrastructure also support expansion. This region holds approximately 25% of the global wireless charging market.

Asia-Pacific dominates the global wireless charging market, led by countries like China, Japan, and South Korea. The region benefits from large-scale manufacturing of smartphones, EVs, and electronic components, along with high R&D activity. Rapid urbanization and consumer tech demand continue to drive aggressive growth. This region accounts for around 45% of the total market.

Europe is seeing significant growth in wireless EV charging due to strict environmental policies and strong EV adoption, especially in countries like Germany, Norway, and the Netherlands. Consumer electronics and industrial applications also support demand. The region emphasizes sustainability and innovation in wireless energy transfer. Europe holds approximately 20% of the market share.

COVID-19 Impact Analysis on the Global Wireless Charging Market:

The COVID-19 pandemic had a mixed impact on the wireless charging market. In the short term, global supply chain disruptions and factory shutdowns delayed the production and delivery of consumer electronics and automotive components, leading to slowed growth in 2020. Reduced consumer spending and shifting priorities away from non-essential tech purchases also impacted demand, especially in the premium smartphone and automotive sectors.

However, the healthcare sector saw increased interest in wireless charging for contactless and sterile medical device applications, helping sustain niche growth during the pandemic. Remote work and digital lifestyles led to sustained demand for personal electronics, keeping the consumer electronics segment relatively stable despite initial slowdowns. Companies accelerated R\&D for wireless technologies, anticipating post-COVID shifts toward more hygienic, cable-free solutions.

In the automotive sector, while EV sales dipped initially, government stimulus programs and renewed sustainability goals post-pandemic reignited interest in EV infrastructure, including wireless charging. The pandemic also increased awareness of touchless solutions across public spaces, which indirectly supported adoption in retail and hospitality.

Latest Trends/Developments:

The wireless charging market in 2025 is witnessing rapid innovation across multiple fronts. The rollout of Qi 2.2 is a major development, with Apple’s upcoming iPhone 17 and MagSafe chargers supporting up to 45–50 W, significantly boosting charging speeds. Android players like Samsung are also embracing Qi 2, with the Galaxy S25 labeled "Qi 2 Ready," indicating growing cross-platform adoption. Magnetic alignment, a key feature of Qi 2, enhances efficiency and user convenience by ensuring precise device positioning. Fast wireless charging (up to 50 W) is becoming mainstream, rivaling wired solutions in speed and convenience. In the EV space, wireless charging standards like SAE J2954 and Qi Ki are enabling real-world deployment of dynamic and stationary EV charging systems.

Simultaneously, wireless power is being integrated into public infrastructure, vehicles, office furniture, and smart kitchens, supporting high-power applications up to 2,200 W. Long-range wireless charging, including RF and over-the-air (OTA) systems, is being explored for IoT, wearables, and sensor networks. Emerging segments like textile-based charging and smart clothing are also under active development. Overall, wireless charging is evolving beyond smartphones into a universal, embedded power delivery ecosystem for the future.

Key Players:

• Infineon Technologies AG (Germany)

• WiTricity Corporation (US)

• Renesas Electronics Corporation (Japan)

• Leggett & Platt, Incorporated (US)

• SAMSUNG (South Korea)

• PUTURN

• Plugless Power Inc. (US)

• Qualcomm Technologies, Inc. (US)

• Texas Instruments Incorporated (US)

• Ossia Inc. (US)

Chapter 1. Global Wireless Charging Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Wireless Charging Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn/$Tn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Wireless Charging Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Wireless Charging Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Wireless Charging Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Wireless Charging Market – By Technology

6.1. Introduction/Key Findings

6.2. Inductive Charging

6.3. Resonant Charging

6.4. Radio Frequency (RF) Based Charging

6.5. Microwave/Infrared Charging

6.6. Y-O-Y Growth trend Analysis By Technology

6.7. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 7. Global Wireless Charging Market – By Application

7.1. Introduction/Key Findings

7.2. Consumer Electronics

7.3. Automotive

7.4. Healthcare

7.5. Industrial

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Wireless Charging Market – By Industry Vertical

8.1. Introduction/Key Findings

8.2. Automotive Industry

8.3. Healthcare Sector

8.4. Consumer Electronics Manufacturers

8.5. Industrial & Defense Sectors

8.6. Y-O-Y Growth trend Analysis By Industry Vertical

8.7. Absolute $ Opportunity Analysis By Industry Vertical, 2025-2030

Chapter 9. Global Wireless Charging Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Technology

9.1.3. By Application

9.1.4. By Industry Vertical

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Technology

9.2.3. By Application

9.2.4. By Industry Vertical

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Technology

9.3.3. By Application

9.3.4. By Industry Vertical

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Technology

9.4.3. By Application

9.4.4. By Industry Vertical

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Technology

9.5.3. By Application

9.5.4. By Industry Vertical

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Wireless Charging Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Infineon Technologies AG (Germany),

10.2. WiTricity Corporation (US)

10.3. Renesas Electronics Corporation (Japan)

10.4. Leggett & Platt Incorporated (US)

10.5. SAMSUNG (South Korea)

10.6. PUTURN

10.7. Plugless Power Inc. (US)

10.8. Qualcomm Technologies, Inc. (US)

10.9. Texas Instruments Incorporated (US)

10.10. Ossia Inc. (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Wireless Charging Market was valued at USD 26.10 billion in 2024 and is projected to reach a market size of USD 114.33 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 34.37%.

Rising Adoption of Wireless Charging in Consumer Electronics, Expansion of Electric Vehicles (EVs) and Smart Mobility Solutions, Advancements in Charging Efficiency and Standards are some of the key market drivers in the Wireless Charging Market.

Consumer Electronics, Automotive, Healthcare, Industrial are the segments by Application in the Wireless Charging Market.

Asia-Pacific is the most dominant region for the Global Wireless Charging Market.

Infineon Technologies AG (Germany), WiTricity Corporation (US), Renesas Electronics Corporation (Japan), Leggett & Platt, Incorporated (US), SAMSUNG (South Korea), PUTURN, Plugless Power Inc. (US), Qualcomm Technologies, Inc. (US), Texas Instruments Incorporated (US), Ossia Inc. (US) etc.