Global Telecom Power Systems Market Research Report – Segmentation By Power Source (On-grid System, Off-grid System, Hybrid System), By Component (Rectifiers, Inverters, Batteries, Power Distribution Units), By Installation Type (Indoor, Outdoor), By Power Output (Up to 10Kw, 10-50Kw, Above 50 Kw), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-1100

Format:

Region: Global

Market Size and Overview:

The Global Telecom Power Systems Market was valued at USD 5.22 billion and is projected to reach a market size of USD 12.49 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 19.06%.

This growth results from the deployment of 5G networks, rising fiber broadband, and the demand for dependable electricity at far-off cell locations. While hybrid solar-diesel systems are gaining ground in off-grid areas to lower carbon footprint and OPEX, on-grid systems remain popular where utilities are consistent. COVID-19 highlighted the requirement for robust electricity in times of restrictions, therefore speeding the switch toward modular, containerized power systems.

Key Market Insights:

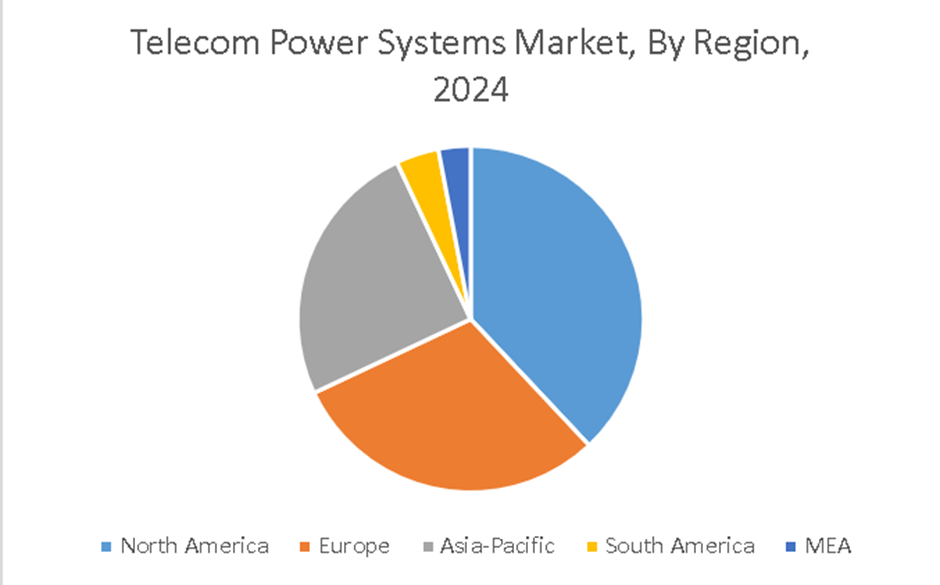

Driven by ambitious 5G and fiber rollouts, strong CAPEX budgets, and strict network‑uptime standards, North America dominates with 35.7% market share in 2024.

As telecom operators give efficient DC power conversion for tower-site workloads first importance, rectifiers account for 45% of the component market.

Reflecting the ubiquity of macro‑cell towers in suburban and rural deployments, outdoor installations almost two to one outperform indoor.

High‑capacity 5G macro‑UPS requirements in thick urban and data‑center edge locations are driving the fastest-growing category, around 14% CAGR, systems above 50 kW.

Telecom Power Systems Market Drivers:

The exponential growth seen in the number of mobile subscribers is considered to be a major market growth driver.

Driven by quick 5G adoption in both developed and developing countries, global mobile subscriptions are expected to reach over 5 billion by 2028; hence, operators must constantly grow tower infrastructure to handle rising data traffic. This subscriber boom translates directly into more cell-site deployments; GSMA estimates over 1 million new base stations will be commissioned globally between 2024 and 2030. To satisfy demanding 99.999 % uptime SLAs required by ultra‑low‑latency 5G services, every new macro‑cell tower needs a resilient power system, sometimes with N+1 redundancy. Critical are energy-efficient DC power units; modern rectifiers achieve > 95 % conversion efficiency, therefore reducing energy losses even under variable load conditions. Dual rectifier strings and parallel battery banks, among other redundant power paths, guarantee unbroken service during component failures or maintenance, therefore preserving QoS for billions of consumers. The persistent expansion in mobile subscriptions drives a sustained demand for modern telecoms power systems able to provide high efficiency, redundancy, and scalability.

The expansion of the remote area network helps the market to increase its reach worldwide.

Driving hybrid solar-diesel and battery-backup power system installation where grid dependability might be under 60 %, especially in sections of Africa and South Asia, bridging the "last mile" in rural and underserved areas has become a strategic goal. With diesel generators and battery banks providing uninterrupted service during low-sunlight periods, operators use solar panels built to satisfy 30–50 % of daily tower energy needs. By allowing monthly or quarterly refueling instead of weekly deliveries, such hybrid microgrids lower diesel‑fuel logistics expenses, formerly up to US$ 0.50/liter in remote locations. By up to 60 %, they also cut yearly fuel consumption, thereby generating significant OPEX savings and fewer site visits for maintenance teams. Satellite-linked non-terrestrial networks (NTNs) currently backhaul performance and power-system telemetry at US$ 5/device/year, therefore guaranteeing 99.9 % data availability for remote-site management. Real-time monitoring via satellite IoT allows predictive analytics on generator health and battery state-of-charge, hence lowering unscheduled downtime by 30 %. In Latin America, pilot projects in the Andes and Amazon areas show 98 % service uptime after hybrid deployment, compared to less than 80 % with diesel-only systems.

Rules and regulations regarding energy efficiency are seen as a great market growth driver.

Reacting to worldwide sustainability requirements, regulators in the EU (Ecodesign Directive) and North America (EPA Energy Star) are phasing out low-efficiency telecom power components, requiring > 95 % efficient rectifiers and outlawing lead-acid batteries with subpar cycling performance. Strict greenhouse-gas emissions targets for carriers—reducing tower-site carbon footprints by 30 % by 2030—are driving the adoption of lithium-ion energy-storage systems (ESS) with greater cycle life and energy density. Smart standby modes and adaptive fan controls found in next-generation power conversion units reduce tower HVAC energy usage by 15 % during off-peak times. Many operators now demand third-party energy audit certifications for new sites to guarantee local efficiency code compliance and qualify for carbon credits under programs like China's MIIT, which has established minimum performance criteria for telecom rectifiers, driving average site energy consumption to fall by 20 % within two years of regulatory execution. The Section 179D tax incentive in the U.S. provides deductions for energy-efficient power equipment at telecom-data-center hybrids, hence lowering CAPEX by as much as 25 %. Predictive-maintenance systems use AI-enabled sensor data to schedule component replacements before efficiency degrades, hence preventing 10–15 % energy loss owing to aging hardware.

The rising adoption of green energy has helped the market to be environmentally friendly, helping the market to grow.

Since 2022, environmental targets and increasing fuel costs have driven 30 % of new tower locations worldwide to include solar PV panels matched with advanced ESS. Hybrid solar-diesel-battery systems reduce diesel usage by up to 70 %, therefore offering both carbon-emission reductions and OPEX savings in areas where diesel can cost over US$ 1.20/liter. With a levelized cost of energy (LCOE) dropping below diesel-only alternatives, solar insolation of 5–7 kWh/m²/day makes PV‑dominant hybrids financially feasible in desert and plateau areas. Wind-PV hybrids are becoming popular in coastal and high-elevation areas since they use complementary generating profiles to raise renewable self-sufficiency to 80 percent of annual energy needs. Emerging fuel‑cell combinations using green hydrogen are being piloted in Europe, providing silent, emission-free backup power satisfying strict noise and emission criteria. Life cycle analyses show hybrid sites achieve 50 percent lower total-cost-of-ownership (TCO) over 10 years than diesel-generator equivalents. Tier-1 operators in South America report reductions up to 40 percent in scope-1 emissions after turning 500 locations to solar-battery hybrids.

Telecom Power Systems Market Restraints and Challenges:

The existence of high upfront costs presents a major challenge for the market.

Depending on capacity and supplier, hybrid and renewable‑hybrid power systems for telecom towers, combining solar PV arrays, battery energy‑storage systems (BESS), and diesel generators, carry starting prices ranging from US$ 50,000 to US$ 100,000 per site. With a price of US$20,000–40,000 per tower, conventional diesel-only installations are much less expensive; this poses a severe financial obstacle for operators in low-ARPU rural areas. Driven by the amortization of PV modules and sophisticated BESS, extended ROI periods of 3–5 years hamper investment when cash flows are restricted by restricted subscriber income. Even with governmental subsidies or carbon‑credit incentives, the net present value (NPV) of hybrid projects often falls below internal hurdle rates of 8–10 %, therefore slowing adoption. Consequently, telecom tower companies need alternative financing, such as green bonds or PPAs, to bridge the CAPEX gap, hence complicating project construction. Although they presently serve under 25% of rural locations due to perceived counterparty risk and contractual complexity, leasing schemes for BESS and solar technology exist. Furthermore, the great initial expense restricts scalability across emerging-market portfolios, where operators could forego hybrid changes in favor of patch generator maintenance.

The existence of a fragmented grid infrastructure is a major drawback faced by this market.

Utility grid reliability in many areas, especially Latin America and sections of Africa, can be below 70 % uptime, with frequent voltage dips and long-lasting outages interfering with tower operations. Operators utilize custom off‑grid solutions from solitary diesel‑generator sets to microgrids, increasing O&M expenditures by 25 percent over those for grid‑tied sites to preserve service continuity. Complex power-system designs combining many energy sources are required by these broken infrastructures, therefore raising engineering hours and spare parts inventories. Furthermore, increasing fuel use and OPEX is the need for operators to oversize diesel generators sometimes by 20–30 % to handle peak loads. Seasonal weather occurrences, such as monsoon flooding or dust storms, frequently damage grid assets, therefore necessitating the quick deployment of temporary gensets and increasing supply‑chain logistics difficulties.

Strict rules and regulations pose a major challenge for the market as they hamper its growth.

Telecom power systems have to follow a web of regional and international rules, including ETSI EN 300 386 for electromagnetic compatibility (EMC) and local environmental guidelines, which call for site-specific design inspections and certifications. Navigating data-sovereignty legislation for remote-monitoring telemetry adds yet another level of complexity since fine-grained power-system data often qualifies as national security infrastructure under legislation. Different nations uphold separate telecom-power regulatory systems (e.g., NFPA 110 in the U.S. vs. IEC 62040 series in Europe), therefore requiring multi-variant equipment setups and raising inventory SKUs. Environmental impact assessments, required in several nations for solar-panel and battery installations, include public consultation phases that can stretch project schedules by 3–6 months.

The shortage of skilled labour required affects the market’s smooth functioning.

Just 15% of tower-site technicians have hybrid microgrid and smart-ESS operation expertise, therefore, 85% depend on traditional diesel-generator repair abilities. The scarcity of skilled certifications, including those for high‑voltage battery-handling and renewable‑systems commissioning, with fewer than 200 accredited training facilities worldwide, means that operators must employ third-party service providers at premium margins of 20–30 %, therefore reducing the OPEX savings from fuel and maintenance efficiency. Technician turnover rates in rural areas might reach more than 40 %, thereby impeding maintenance continuity as qualified personnel seek urban-center chances. To fully realize the advantages of hybrid and renewable-hybrid telecom power systems, it is imperative to bridge this skilled-labor gap via scalable e-learning and regional training centers.

Telecom Power Systems Market Opportunities:

The use of Edge-AI Predictive Maintenance helps in reducing cost by 50%, which is a major market opportunity.

Using lightweight neural accelerators, telecoms operators are embedding edge‑AI sensors straight into rectifier and battery cabinets to process performance data in situ, therefore removing the necessity for continual high‑bandwidth backhaul. These on‑device models examine temperature, voltage, and current trends in real time, detecting aberrant deviations that precede hardware failures by up to 30 days. Sites can plan maintenance visits proactively by anticipating rectifier or battery module degradation with 85–90 % accuracy, hence lowering unexpected downtime by 40 %. Through optimized spare‑parts inventory and fewer emergency generator runs, edge‑AI predictive‑maintenance deployments cut OPEX by 15 %. Edge‑AI also lowers data‑transmission costs by up to 50⠯% because only health‑status summaries and alerts are uplinked rather than raw high‑frequency telemetry. Modern TinyML frameworks allow these AI workloads to run on sub‑watt sensor nodes, so extending battery‑operated hub lifetimes to over 5 years without maintenance. By 2030, edge‑AI predictive‑maintenance deployments are projected to cover 70 % of new and retrofitted tower sites worldwide, a tenfold increase from 2023 levels.

The deployment of Satellite-IoT NTN presents a great market growth opportunity.

Offered at US$5 per device per year, deployment of LEO‑satellite IoT connectivity enables remote monitoring of off‑grid power cabinets in places devoid of terrestrial coverage, therefore assuring 99.9 % data availability for telemetry and alarms. Hybrid IoT modules buffer local measurements, battery SOC, rectifier load, generator runtime, and transmit only consolidated status reports via satellite, therefore maximizing airtime expenses and preserving node battery life. This continuous link enables core NOC systems to perform AI-driven analyses on gen-set fuel consumption patterns, hence activating refueling and maintenance dispatch before service degradation sets in. For edge‑AI sensors, LEO‑backhaul also enables Firmware‑Over‑The‑Air (FOTA) upgrades, ensuring that predictive‑maintenance algorithms stay abreast of changing tower‑hardware profiles. Operators in experiments spanning distant ranch and plantation locations in Canada's Yukon and Australia's Outback attained 98% uptime over 12 months, a significant increase above sporadic VSAT connections.

The advent of onshore module production helps in reducing module costs and protecting the supply chain.

Domestic semiconductor and power-module manufacturing is accelerating under the US$ 50 billion under the U.S. CHIPS and Science Act, halving lead times for DC-rectifier and inverter assemblies from 16 weeks to 8 weeks. Tax credits and milestone-based incentives help onshore manufacturing plants, lowering module unit prices by 20% compared to imports and shielding supply networks from geopolitical disturbances. Localized assembly lines close to important telecom hubs, such as Austin, TX, and Phoenix, AZ, allow just-in-time deliveries that lower inventory carrying expenses by 25%. These CHIPS-funded projects also promote collaboration between module OEMs and telecom-equipment integrators, thereby speeding NPI cycles for novel power-system designs by 30 %. Data from the U.S. Department of Commerce reveal that 95 % of CHIPS-funded projects have met first-article manufacturing on time, emphasizing program effectiveness. U.S. Department of Commerce data reveals 95% of CHIPS-funded initiatives to have first-article production on schedule, therefore highlighting program effectiveness. Onshore lines follow strict quality-management criteria, ISO 9001 and IPC-610, guaranteeing module dependability in demanding outdoor and indoor telecom settings.

The use of private 5 G and LTE Networks helps the market to expand its reach.

Enterprises and now telecom tower operators are deploying private LTE/5G networks in the CBRS (3550–3700 MHz) band to guarantee 35 % higher uptime than public networks, crucial for real‑time tower‑maintenance applications such as drone inspections and remote‑switchgear control. CBRS‑based private networks provide dedicated spectrum slices, ensuring minimal interference and predictable latency (< 10 ms) for mission‑critical feeds like high‑definition CCTV streams and edge‑AI data uplinks. By coupling private‑network MEC nodes with tower‑site power‑system controllers, operators can execute local fault‑isolation and configuration changes autonomously, reducing mean‑time‑to‑repair (MTTR) by 40 %. Neutral‑host CBRS deployments enable multi‑tenant sharing of the same small‑cell infrastructure, serving both operator and third‑party maintenance crews, cutting per‑tenant CapEx by 25 %. Case studies from port and mining colleges show 99.99% private-network availability even in RF-congested industrial environments, thereby confirming CBRS dependability for interior and outdoor tower-site applications. For private networks, regulators have simplified FCC SAS certification, therefore decreasing authorization times from 90 days to 30 days and hence speeding up deployments for time-sensitive projects.

Telecom Power Systems Market Segmentation:

Market Segmentation: By Power Source

• On-grid System

• Off-grid System

• Hybrid System

The On-grid Systems segment is said to dominate this market. Favored where dependable utility electricity is accessible, on-grid systems represented roughly 60% of overall installations because of less upfront CAPEX and easier integration. The Hybrid System segment is the fastest-growing segment of the market. Hybrid (diesel-solar, diesel-wind, solar-battery) solutions are expected to rise at around 16% CAGR between now and 2030 as carriers try to reduce fuel usage by up to 70% and meet carbon-reduction objectives. For ultra-remote areas, off-grid (diesel-only, battery backup) continues to be vital; they account for around 25% of fresh tower electrifications, however, OPEX and environmental considerations restrict expansion.

Market Segmentation: By Component

• Rectifiers

• Inverters

• Batteries

• Power Distribution Units

Here, the Rectifiers segment is dominant, and the Batteries segment is the fastest-growing segment for this market. Particularly in dense urban deployments, carriers give top priority to high-efficiency modular rectifiers to reduce energy losses. Driven by a move toward lithium‑ion chemistries that provide longer cycle life (4,000+ cycles) and lower maintenance, the battery sector (lead‑acid and lithium‑ion) is expanding at about 12 percent CAGR. When it comes to Power Distribution Units and the Inverters segments, accounting for the other about 40%, inverters (AC-DC/ DC-AC conversion) and PDUs aid AC loads (HVAC, lighting) and enable detailed power control at the site level.

Market Segmentation: By Installation Type

• Indoor

• Outdoor

The Outdoor segment dominates this market, reflecting the widespread macro-cell tower presence in rural and suburban areas where integrated outdoor cabinets are preferred. Outdoor (dominating) power systems comprise roughly 65 % of tower-site power systems. The Indoor segment is said to be the fastest-growing segment of the market. Driven by the spread of small cells and interior DAS (Distributed Antenna Systems) in metropolitan locations, offices, and public areas, indoor installations are growing at around 10% CAGR.

Market Segmentation: By Power Output

• Up to 10 kW

• 10-50 kW

• Above 50 kW

The 10-50 kW segment is said to dominate this market, holding around 55% share. The 10–50 kW segment matches standard macro‑cell power needs (transceivers, cooling) at medium‑density sites. The Above 50 kW segment is said to be the fastest-growing segment of the market. High‑capacity 5G macro‑sites, edge‑compute base stations, and data‑center colocation within telecom estates are driving a 14 percent CAGR in systems over 50 kW. The Up to 10 kW segment is suitable for campus and in-building coverage needs, small-cell and enterprise-site power (up to 10 kW) accounts for approximately 15% of installs.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

Here North America is said to lead this market due to advanced 5 G technology, strong budget for the market and latest initiatives taken regarding fiber-to-the-tower initiative. The Asia-Pacific region is said to be the fastest-growing region, this is driven by increasing mobile penetration, schemes regarding rural connectivity in India and China, increasing use of renewable hybrid power in rural regions.

Europe holds the second-largest market share due to a strong regulatory framework, use of power-efficient telecom power, and renewable energy directives. South America and the MEA regions are said to be the emerging markets. This is due to expansion into underserved areas, increased reliance on hybrid power and microgrid.

COVID-19 Impact Analysis on the Global Telecom Power Systems Market:

Early in 2020, supply-chain interruptions caused 3–6-month delays in shipment of rectifier modules and batteries; however, the pandemic also emphasized the need for resilient, modular power solutions as remote work and online services increased by 70 %, therefore speeding deployment of containerized power equipment at cell locations. Operators increased inventory buffers and switched to hybrid power collaborations to guarantee network uptime under global lockdowns.

Latest Trends/ Developments:

Cutting energy costs by 10%, platforms like Vertiv's Environet maximize real-time load balancing.

For its increased cycle life and reduced maintenance against lead-acid, adoption increased by 25%.

Supported by government incentives, solar-wind-diesel hybrids on rural towers reduce fuel usage by 70%.

For predictive analytics and scenario testing, pilots by Eaton and Huawei construct virtual duplicates of power locations.

Key Players:

• Ascot

• Alpha Technologies

• Eaton

• General Electric

• Huawei Technologies Co.

• ZTE Corporation

• Schneider Electric

• Services, Inc.

• Cummins Inc.

• Vertiv Group

Chapter 1. Global Telecom Power Systems Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Telecom Power Systems Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Telecom Power Systems Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Telecom Power Systems Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Telecom Power Systems Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Telecom Power Systems Market– By Power Source

6.1. Introduction/Key Findings

6.2. On-grid System

6.3. Off-grid System

6.4. Hybrid System

6.5. Y-O-Y Growth trend Analysis By Power Source

6.6. Absolute $ Opportunity Analysis By Power Source , 2025-2030

Chapter 7. Global Telecom Power Systems Market– By Component

7.1 Introduction/Key Findings

7.2. Rectifiers

7.3. Inverters

7.4. Batteries

7.5. Power Distribution Units

7.6. Y-O-Y Growth trend Analysis By Component

7.7. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 8. Global Telecom Power Systems Market– By Installation Type

8.1. Introduction/Key Findings

8.2. Indoor

8.3. Outdoor

8.4. Y-O-Y Growth trend Analysis By Installation Type

8.5. Absolute $ Opportunity Analysis By Installation Type, 2025-2030

Chapter 9. Global Telecom Power Systems Market– By Power Output

9.1. Introduction/Key Findings

9.2. Up to 10Kw

9.3. 10-50Kw

9.4. Above 50 Kw

9.5. Y-O-Y Growth trend Analysis By Power Output

9.6. Absolute $ Opportunity Analysis By Power Output, 2025-2030

Chapter 10. Global Telecom Power Systems Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Power Source

10.1.3. By Component

10.1.4. By Installation Type

10.1.5. By Power Output

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Power Source

10.2.3. By Component

10.2.4. By Installation Type

10.2.5. By Power Output

10.2.6. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Power Source

10.3.3. By Component

10.3.4. By Installation Type

10.3.5. By Power Output

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Power Source

10.4.3. By Component

10.4.4. By Installation Type

10.4.5. By Power Output

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Power Source

10.5.3. By Component

10.5.4. By Installation Type

10.5.5. By Power Output

10.5.6. By Region

Chapter 11. Global Telecom Power Systems Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Ascot

11.2. Alpha Technologies

11.3. Eaton

11.4. General Electric

11.5. Huawei Technologies Co.

11.6. ZTE Corporation

11.7. Schneider Electric

11.8. Services, Inc.

11.9. Cummins Inc.

11.10. Vertiv Group

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Telecom Power Systems Market was valued at USD 5.22 billion and is projected to reach a market size of USD 12.49 billion by the end of 2030 with a CAGR of 19.06%.

Lower CAPEX and easier operations, where utility grids are dependable, cause on‑grid systems to lead this market with a 60% market share.

Driven by rural connection initiatives and hybrid power requirements, Asia Pacific is the fastest growing area at around 14% CAGR.

Although causing initial supply-chain delays, COVID‑19 brought attention to the need for resilient, modular power solutions, sped hybrid and microgrid implementations at distant cell sites.

Often US$ 50,000–100,000 per site, high initial CAPEX for hybrid and renewable-hybrid systems continues to be an obstacle in low-ARPU countries.