Global Super Junction MOSFET Market Research Report – Segmentation By Voltage Rating (Below 600V, 600V – 1,000V, Above 1,000V); By Application (Consumer Electronics, Electric Vehicles & Automotive, Industrial Power Supplies, Others); By Material Type (Silicon, Others); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16519

Format:

Region: Global

Market Size and Overview:

The Super Junction MOSFET Market was valued at USD 3.3 billion in 2024 and is projected to reach a market size of USD 21.09 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 44.92%.

Super Junction MOSFETs, with their superior efficiency, less space, and minimal energy losses, are transforming power electronics worldwide. These advanced MOSFETs, based on the latest super-junction structure, offer improved performance in electric vehicles, renewable energy systems, industrial power supplies, and data centers. The need for super junction MOSFETs as green and fast solutions pushes the industries to empower next-generation devices with the highest power density and energy savings made possible.

Key Market Insights:

More than 60% of new solar inverters and wind power converters now use super junction MOSFETs to minimize power losses and improve overall energy output. Their efficiency helps meet strict global emission targets.

Super junction MOSFETs have helped reduce data center energy losses by up to 40%, supporting the shift to greener, high-performance server infrastructures. This is crucial as global data traffic grows rapidly.

Super Junction MOSFET Market Drivers:

In today's technology-driven world, there is an urgent need for devices that consume less energy while delivering higher performance.

Today, there is a clarion call for low-energy-consuming devices that are more performant. The super junction MOSFETs, with their design of impressively lower conduction and switching losses over the regular MOSFETs, serve this purpose. With unique architecture, they provide for higher breakdown voltages and faster switching, thus making them suitable for high-voltage and high-frequency applications. The industries, like electric vehicles, data centers, and consumer electronics, are rapidly embracing these components for minimum energy wastage and higher system performance. On a global front, decarbonization and net-zero emissions are lending urgency to the proliferation of these advanced devices. Governments all over the world have launched policies and incentives to promote energy efficiency technologies, indirectly fuelling market growth. Consumers and businesses alike are being conscious of their carbon footprint, encouraging OEMs to develop more efficient power solutions. This indicates a strong upward demand trajectory for super junction MOSFETs in the next few years as they are set to become the enabling backbone of sustainable energy systems.

The global surge in electric vehicle (EV) production and renewable energy installations is a major catalyst for the super junction MOSFET market.

The worldwide trend of ramping up electric vehicle and renewable energy installation is a significant driving force for the super junction MOSFET market. EV manufacturers demand power components with high-voltage capability, which occupy low weight and volume in order to maximize overall vehicle shrinkage and battery life. With high switching performance and lower heat generation, the super junction MOSFET has emerged as one of the key technologies for EV onboard chargers, DC-DC converters, and motor drive inverters. Similarly, renewable energy systems like solar inverters and wind turbine converters depend on these MOSFETs for the efficient conversion and regulation of power under varying load and environmental conditions. Thus, the focus on reducing dependence on fossil fuels and climate targets is manifesting in an accelerated deployment of clean energy solutions. Further support toward the transition to electric and renewables is given by generous government subsidies and favorable regulations in major economies. Thus, the wave of application drives ongoing innovation and scaling up of production in the super junction MOSFET market, a very important pillar of the clean energy revolution.

Super Junction MOSFET Market Restraints and Challenges:

Despite their significant performance advantages, super junction MOSFETs face a major challenge in the form of complex manufacturing processes and higher production costs.

Super junction MOSFETs possess great performance advantages; however, a major challenge always has to do with the complex manufacturing process and a higher cost of production. These high-tech structures call for advanced doping techniques, deep trench etching, and multi-step fabrication processes, all of which are considerably more demanding than their traditional planar counterparts. The intricacy involved renders the whole setup very capital-intensive for the manufacturers and, on top of that, results in lower yields, which make it very difficult to attain cost-competitive scale. Smaller players in the semiconductor field often find it difficult to invest in specialized equipment and expertise, creating an entry barrier. Also, even a minuscule variation from the intended process could prove fairly detrimental to device reliability and performance, and therefore add to quality control costs. This manufacturing difficulty also deepens supply chain vulnerabilities, especially during semiconductor shortages or geopolitical mischief. Technological progress is trying to accelerate these processes and cut costs; however, the initial costs and technicalities involved remain major restraints, which could slow the expansion of the market in some sectors.

Super Junction MOSFET Market Opportunities:

The worldwide wave of electrification and digitalization is venturing into a vast arena for super junction MOSFETs, with a number of vibrant growth opportunities. The ongoing trend toward compact, high-voltage, energy-efficient systems uniquely positions MOSFETs for backbone thrusting into next-generation designs. For instance, in electric vehicles, increasing use of 800V architectures for ultra-fast charging has created a parallel demand for advanced high-voltage components. On similar lines, a smart grid infrastructure and energy storage systems call for low-loss power switches for improved reliability and reduced transmission losses. On the flip side, a booming opportunity exists in the area of advanced consumer electronics, where 5G base stations, ultra-thin laptops, and high-efficiency power adapters are becoming rampant. This situation creates demand for more power in even smaller form factors, giving an edge to switching technologies. Renewable energy and decentralized power generation now reiterated the viability of power conversion solutions, where super junction MOSFETs will come into play. As new materials and packaging techniques continue to evolve, opportunities to cut costs and enter even more mainstream and price-sensitive applications would open up. Anticipating the growth and tech leadership of super junction MOSFETs over the next 10 years may be envisioned owing to the effects of all these market pull trends.

Super Junction MOSFET Market Segmentation:

Market Segmentation: By Voltage Rating

• Below 600V

• 600V – 1,000V

• Above 1,000V

There are three categories into which the super junction MOSFET market is segmented based on voltage rating: up to 600V, from 600V to 1,000V, and above 1,000V. Devices rated below 600V are mainly used in low-to-medium power applications such as adapters, chargers, and consumer electronics, where compact size and efficiency are key requirements. However, the largest growth category is between 600V and 1,000V: electric vehicles, industrial motor drives, and renewable energy systems will be driving much of the demand. This range provides the best trade-off between performance and cost, appealing to a wide variety of high-efficiency applications. Although above 1,000V MOSFETs are a small segment today, they will take on more significance shortly for specific industrial applications and large infrastructure in energy, including high-voltage DC power transmission and grid-level energy storage. As newer applications call for higher voltages to minimize the total cost and footprint of systems even further, this segment expects continued growth. These three voltage segments all play a critical role in the light of an aggressive electrification trend worldwide, together with heightened expectations from end-users for improved delivery time, reliability, and energy savings. Investment in Research and Development is made by the manufacturers across each of the aforementioned segments for further enhancement of voltage endurance and switching speeds. Altogether, segmentation by voltage provides a strategic framework to respond to diversified needs in the market while facilitating relevant innovations.

Market Segmentation: By Application

• Consumer Electronics

• Electric Vehicles & Automotive

• Industrial Power Supplies

• Others

From an application point of view, super junction MOSFETs are used in consumer electronics, electric vehicles and automotive, industrial power supplies, and others (including data centers and telecommunications). Consumer electronics still represent a significant market for this class of MOSFETs in power adapters, LED drivers, and ultra-slim devices for compactness and energy savings. The electric vehicles and automotive segment is the fastest-growing, with super junction MOSFETs finding their way into onboard chargers, DC-DC converters, and traction inverters where high efficiency and minimum heat generation are required. In industrial power supplies, these components are used for the improvement of efficiency, lowering cooling requirements, and enhancing reliability in motor drives, factory automation, and UPS systems. The "others" category-subsuming data centers, telecom base stations, and renewable energy converters also rising really fast, primarily due to the concerted efforts of such organizations in energy loss and operating cost minimization. As worldwide trends evolve towards electrification, renewable integration, and smart grid development, so too continues the expanding application spectrum of super junction MOSFETs. This multi-sector usage greatly increases demand and pushes for technology improvements to meet stringent performance requirements. Application diversification is likely to remain a major growth pillar for this market from 2025 to 2030.

Market Segmentation: By Material Type

• Silicon

• Others

Considering material type segmentation, silicon still dominates the market for super junction MXFETs on account of a mature manufacturing ecosystem, proven reliability, and cost efficiency. Silicon-based super junction MOSFETs have been optimized over the years to exhibit high-performance characteristics in high-voltage applications as well as low cost, which is paramount to mass market adoption. The "others" category is fast emerging, and it includes emerging materials such as silicon carbide (SiC) and gallium nitride (GaN) hybrids. This class of advanced materials possesses excellent thermal conductivity, high breakdown voltage, and fast switching attributes, thus becoming suitable for next-generation high-power applications, particularly in the areas of electric vehicles and renewable energy systems. Although at present they may represent a much smaller share, it is anticipated that with continued investment in material innovation and decreasing cost of production, their adoption would certainly increase. With the industry moving toward higher voltage and faster switching requirements, alternative materials will gain significance alongside silicon. Hence, the material segmentation, therefore, marks a dynamic shift where traditional silicon stands strong but lays the pathway for future breakthroughs through advanced materials.

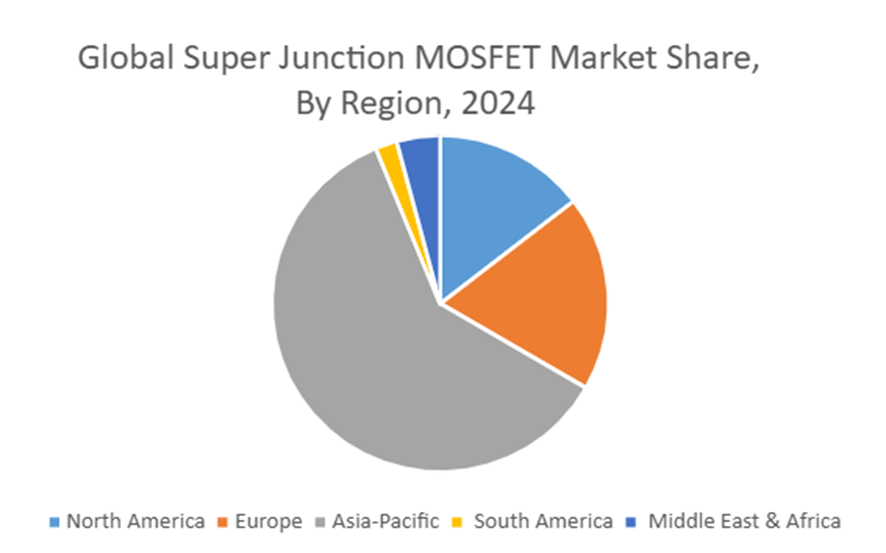

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

The Asia-Pacific region is at the forefront of the super junction MOSFET market, powered by an excellent electronics manufacturing ecosystem and electric vehicle growth in China, Japan, and South Korea. The area also benefits from government incentives meant for green energy and high-volume consumer electronics production in volume. Europe comes next, with massive adoption of electric vehicles, along with imposing renewable energy goals and energy efficiency regulations, hence driving the use of advanced power semiconductors. North America has its fair share as well, benefiting from investments in data centers, industrial automation, and clean energy. Advancement of projects in the Middle East and Africa will gradually follow, as the regions invest in infrastructure modernization and solar energy. South America is slowly emerging with demand growth in the industrial and energy sectors as economies work to strengthen local manufacturing and power reliability. The collective dynamics of these regions, as illustrated, show how different policies and technological uptake are fostering market growth around the globe.

COVID-19 Impact Analysis on the Super Junction MOSFET Market:

The COVID-19 pandemic initially did great disservice to the super junction MOSFET market at a global scale, disrupting the entire supply chain system, halting manufacturing activities, and delaying international shipments of semiconductors. Lockdowns and restrictions in key manufacturing locations, and especially across Asia-Pacific, created shortages for raw materials and bottlenecks during production, causing delayed deliveries to downstream sectors like automotive, industrial, and consumer electronics. Meanwhile, the advancement of the pandemic did push some growth drivers. The demand surge in data centers and cloud computing due to remote work and online services gave rise to the demand for high-efficiency power components such as super junction MOSFETs. Also, revived global focus on electric vehicles and renewable energy under 'green recovery' strategies did assist in offsetting early setbacks and promoting long-term market optimism. A lot of manufacturers became motivated to develop more resilient and geographically diversified supply chains aimed at better operational flexibility. Though the market suffered slowdowns in the short term in 2020, it made an impressive recovery throughout the months in the following years, showing strong adaptability and further proving the importance of super junction MOSFETs in the emergence of energy and digitalization in the new, post-pandemic world.

Latest Trends/ Developments:

The Global Super Junction MOSFET Market is witnessing tremendous advancements owing to rapid technological innovation and changing demands for applications. Major trends involve the adoption of wide bandgap materials like silicon carbide (SiC) and gallium nitride (GaN) combined with conventional silicon to realize even higher levels of efficiency and voltage capability, especially for electric vehicles and high-performance industrial applications. The transition to renewable energy has provided a platform for super junction MOSFETs specifically optimized for solar inverters and energy storage systems towards the global goal of decarbonization. Furthermore, the increase in the adoption of electric vehicles has driven higher-voltage designs such as 800V architectures, enabling faster charging and enhanced energy efficiency. Sustainability is increasingly gaining traction among manufacturers to design eco-friendly, low-loss components that would lower the carbon footprint of the overall system. Such developments are all converging toward super junction MOSFETs becoming leaders in the transition toward smarter, greener, and energy-efficient electronic systems across the globe.

Key Players:

• Alpha and Omega Semiconductor

• PANJIT

• ROHM Co., Ltd.

• Toshiba Corporation

• Magnachip

• Fuji Electric Co., Ltd.

• Vishay Intertechnology, Inc.

• Infineon Technologies AG

• IceMOS Technology Ltd.

• STMicroelectronics N.V.

Chapter 1. Global Super Junction MOSFET Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Super Junction MOSFET Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Super Junction MOSFET Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Super Junction MOSFET Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Super Junction MOSFET Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Super Junction MOSFET Market – By Voltage Rating

6.1. Introduction/Key Findings

6.2. Below 600V

6.3. 600V – 1,000V

6.4. Above 1,000V

6.5. Y-O-Y Growth trend Analysis By Voltage Rating

6.6. Absolute $ Opportunity Analysis By Voltage Rating, 2025-2030

Chapter 7. Global Super Junction MOSFET Market – By Application

7.1. Introduction/Key Findings

7.2. Consumer Electronics

7.3. Electric Vehicles & Automotive

7.4. Industrial Power Supplies

7.5. Others

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Super Junction MOSFET Market – By Material Type

8.1. Introduction/Key Findings

8.2. Silicon

8.3. Others

8.4. Y-O-Y Growth trend Analysis By Material Type

8.5. Absolute $ Opportunity Analysis By Material Type, 2025-2030

Chapter 9. Global Super Junction MOSFET Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Voltage Rating

9.1.3. By Application

9.1.4. By Material Type

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Voltage Rating

9.2.3. By Application

9.2.4. By Material Type

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Voltage Rating

9.3.3. By Application

9.3.4. By Material Type

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Voltage Rating

9.4.3. By Application

9.4.4. By Material Type

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Voltage Rating

9.5.3. By Application

9.5.4. By Material Type

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Super Junction MOSFET Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Alpha and Omega Semiconductor

10.2. PANJIT

10.3. ROHM Co. Ltd.

10.4. Toshiba Corporation

10.5. Magnachip

10.6. Fuji Electric Co., Ltd.

10.7. Vishay Intertechnology, Inc.

10.8. Infineon Technologies AG

10.9. IceMOS Technology Ltd.

10.10. STMicroelectronics N.V.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Super Junction MOSFET Market was valued at USD 3.3 billion in 2024 and is projected to reach a market size of USD 21.09 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 44.92%.

Rising demand for energy-efficient, high-voltage power devices in EVs and renewable energy systems drives market growth. Advancements in compact, high-performance electronics accelerate adoption across industrial and consumer applications.

Key application segments include consumer electronics, electric vehicles & automotive, industrial power supplies, and others such as data centers and telecom systems. These diverse segments drive demand for high-efficiency, compact, and reliable power solutions worldwide.

Asia-Pacific is the most dominant region for the Super Junction MOSFET Market.

Alpha and Omega Semiconductor, PANJIT, ROHM Co., Ltd., Toshiba Corporation, Magnachip, Fuji Electric Co., Ltd., Vishay Intertechnology, Inc., Infineon Technologies AG, IceMOS Technology Ltd., and STMicroelectronics N.V. are the key players in the Super Junction MOSFET Market.