Global Solid-State Transformer Market Research Report – Segmentation by Voltage Level (HV/MV, MV/LV); By Application (Renewable Power Generation, Automotive, Power Grids, Traction Locomotives, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-6954

Format:

Region: Global

Market Size and Overview:

The Global Solid-State Transformer Market was valued at USD 241.9 million in 2024 and is projected to reach a market size of USD 707.18 million by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.9%.

The Solid-State Transformer (SST) market represents a transformative shift in power distribution and energy management, driven by the global need for smarter, more efficient, and flexible electrical grids. Unlike traditional transformers, SSTs leverage advanced power electronics, enabling not just voltage transformation but also functions such as real-time monitoring, power quality management, bidirectional power flow, and integration of renewable energy sources. These capabilities make SSTs crucial for modern smart grids, electric vehicle (EV) charging infrastructure, distributed energy systems, and advanced industrial applications. As energy consumption patterns evolve and grid complexity increases, the demand for SSTs is rising across residential, commercial, and utility-scale sectors, especially in regions focusing on clean energy transitions and grid modernization.

Key Market Insights:

The adoption of solid-state transformers is accelerating due to growing demand for smart grid infrastructure and renewable energy integration. Over 35% of new grid modernization projects in developed regions now include SSTs as part of their advanced power distribution systems. Their ability to enable real-time power flow control and integration of distributed energy resources (DERs) makes them a critical component in the transition toward more decentralized and efficient energy systems.

Electric vehicle (EV) charging infrastructure is another major growth area, with over 25% of high-capacity EV fast-charging stations projected to adopt SST technology by 2027. This is primarily due to the SST's compact size, voltage conversion flexibility, and bidirectional power flow capabilities, which support vehicle-to-grid (V2G) systems and reduce energy losses compared to traditional transformers.

From an industrial perspective, the manufacturing and transportation sectors are increasingly leveraging SSTs to improve energy efficiency and system reliability. Adoption rates in industrial power systems are expected to grow by more than 20% annually, driven by rising automation, increased power demand, and the demand for resilient energy infrastructure that supports smart operations and predictive maintenance.

Solid-State Transformer Market Drivers:

Rising Demand for Smart Grid Infrastructure and Real-Time Power Management

One of the most significant drivers of the solid-state transformer (SST) market is the rising global demand for smart grid infrastructure capable of real-time power monitoring, advanced load management, and two-way energy communication. Traditional transformers lack the intelligence and adaptability needed to support modern energy requirements, particularly in urban environments where dynamic electricity consumption is a daily reality. SSTs offer enhanced digital control, allowing utilities to monitor grid conditions, optimize power flow, and swiftly respond to faults or changes in demand. Their ability to manage voltage fluctuations, improve power quality, and support self-healing grid capabilities positions them as the core enablers of next-generation electrical networks.

Integration of Renewable Energy Sources and Distributed Generation Needs Advanced Transformation Systems

The global transition toward renewable energy sources such as solar and wind has created the need for highly flexible and intelligent transformation systems like SSTs. Unlike conventional transformers, SSTs can efficiently handle fluctuating input and output voltages and frequencies, making them ideal for integrating variable renewable energy resources into the grid. As more distributed generation units are installed across residential, commercial, and industrial sectors, the ability of SSTs to manage decentralized inputs, regulate power quality, and support bidirectional flow becomes essential. Their built-in capability to convert between AC and DC also supports hybrid renewable systems, which are increasingly being deployed in microgrids and off-grid applications. This makes SSTs vital not only for renewable integration but also for achieving broader energy efficiency and sustainability goals set by both private and public entities.

Accelerating Adoption of Electric Vehicles and EV Charging Infrastructure Requires Flexible Power Distribution

The rising global adoption of electric vehicles (EVs) has led to an urgent demand for advanced and flexible EV charging infrastructure, where SSTs are proving to be a game-changing technology. Their ability to support fast charging, provide bidirectional power flow (enabling vehicle-to-grid or V2G applications), and handle high-voltage conversion with minimal energy loss makes them ideal for powering EV networks. SSTs can directly connect to both medium-voltage and low-voltage networks, offering flexibility in installation and operation. As countries aim to expand their EV fleets and reduce carbon emissions from transportation, the role of SSTs in enabling high-performance charging stations is becoming increasingly critical. Furthermore, their compact design and superior thermal management allow them to be installed in space-constrained urban areas, supporting the rapid expansion of EV infrastructure globally.

Industrial Automation and Grid Modernization Efforts Are Fueling SST Deployment in Heavy Industries

With industries undergoing digital transformation and increasing levels of automation, the demand for resilient, efficient, and smart power systems is rising, driving the adoption of solid-state transformers in manufacturing and heavy industrial sectors. SSTs not only offer superior voltage regulation and harmonic reduction but also enhance equipment protection and operational reliability—key concerns for facilities with sensitive electronic systems and continuous operations. They also enable predictive maintenance and remote monitoring, reducing downtime and operational costs. In regions where industrial development is booming, such as Asia-Pacific and parts of the Middle East, SSTs are being viewed as essential assets for future-ready infrastructure.

Solid-State Transformer Market Restraints and Challenges:

High Initial Costs, Complex Integration, and Limited Awareness Continue to Restrain Widespread Adoption

Despite the promising advantages of solid-state transformers, several restraints and challenges are slowing down their widespread adoption across global markets. One of the primary barriers is the high initial cost associated with SST development, manufacturing, and installation, which is significantly greater than that of conventional transformers. These elevated costs stem from the use of advanced semiconductors, power electronics, and cooling systems, making them less accessible for cost-sensitive projects, particularly in developing regions. Moreover, integrating SSTs into existing grid infrastructure poses technical complexities due to compatibility issues, lack of standardized protocols, and the need for skilled personnel for installation and maintenance. In addition, limited industry awareness and hesitation to transition from well-established transformer systems to newer digital alternatives create psychological and organizational resistance among utility providers and industries.

Solid-State Transformer Market Opportunities:

The solid-state transformer market is poised to benefit from a wide array of emerging opportunities driven by the global push toward clean energy, electric mobility, and digital infrastructure. As countries invest heavily in renewable energy projects, SSTs offer the ideal solution for integrating solar and wind power into modern grids with precision, efficiency, and real-time control. Their capability to manage bidirectional power flow and support AC/DC conversion makes them indispensable for fast-growing EV charging networks, especially with the rise of vehicle-to-grid (V2G) technologies. Furthermore, as smart city initiatives expand across the globe, the need for intelligent, compact, and energy-efficient power distribution systems opens up new markets for SSTs in residential, commercial, and municipal applications. Innovations in semiconductor materials, such as silicon carbide and gallium nitride, are also expected to reduce costs and enhance performance, further strengthening the role of SSTs in shaping the next generation of power infrastructure.

Solid-State Transformer Market Segmentation:

Market Segmentation: By Voltage Level:

• HV/MV

• MV/LV

In the solid-state transformer market, the MV/LV (Medium Voltage/Low Voltage) segment currently holds dominance due to its widespread application across commercial buildings, residential infrastructure, renewable energy systems, and electric vehicle charging stations. This voltage level is highly suitable for distribution networks that require compact, efficient, and intelligent transformers to regulate and deliver power effectively at the final stage of the grid. MV/LV SSTs are preferred in smart grid deployments as they offer superior control over local power distribution, power quality improvement, and energy efficiency enhancements. Additionally, they are easier to integrate into existing low-voltage infrastructure, which makes them a practical and scalable solution for urban energy systems, making this segment the most established and widely adopted in the market today.

On the other hand, the HV/MV (High Voltage/Medium Voltage) segment is projected to be the fastest growing in the coming years, driven by rising investments in utility-scale renewable energy projects and the need for long-distance power transmission with minimal loss. As countries upgrade their national grid infrastructure and shift toward centralized renewable energy generation—such as large solar parks or offshore wind farms—HV/MV SSTs offer the necessary voltage regulation and digital control features to handle high-capacity, high-voltage transmission systems. Their ability to replace bulky conventional transformers with more compact and intelligent systems makes them especially attractive for future-ready substations and large-scale industrial applications. As technological advancements reduce their cost and improve their reliability, HV/MV SSTs are expected to see accelerated adoption across power utilities and large industrial operations globally.

Market Segmentation: By Application:

• Renewable Power Generation

• Automotive

• Power Grids

• Traction Locomotives

• Others

Among the various applications, Power Grids remain the dominant segment in the solid-state transformer market due to their critical role in modernizing and stabilizing energy distribution networks worldwide. Utilities and grid operators are increasingly adopting SSTs for their ability to manage power flow, reduce losses, enhance voltage regulation, and enable real-time monitoring across the grid. With rising electricity demand, aging infrastructure, and a strong push for grid digitization, SSTs offer the ideal solution to overcome inefficiencies of traditional transformers and support complex grid requirements. Their use in substations enhances grid resilience, allows better integration of distributed energy resources, and ensures seamless two-way communication of energy—a necessity in today’s smart grid architecture.

The Automotive sector, particularly driven by the surge of electric vehicles (EVs), is emerging as the fastest growing application segment for solid-state transformers. With the exponential growth in EV adoption globally, there is a high demand for efficient and high-speed EV charging infrastructure, where SSTs play a crucial role. Their compact size, advanced voltage conversion capabilities, and ability to handle bidirectional power flow make them ideal for EV fast chargers and vehicle-to-grid (V2G) systems. SSTs also improve the overall energy efficiency of charging stations while reducing installation space and cooling requirements. As automotive manufacturers, charging network providers, and governments invest heavily in expanding EV ecosystems, the automotive application of SSTs is expected to see rapid deployment and innovation, positioning it as the most dynamically growing area within the market.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

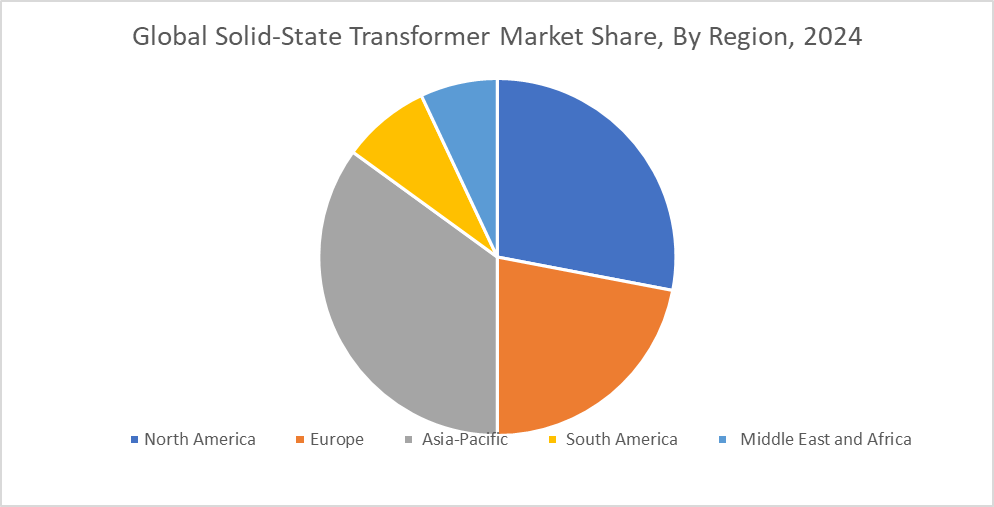

In the regional landscape of the solid-state transformer market, Asia-Pacific holds the dominant position, contributing the largest share at 35%. This dominance is primarily fueled by rapid industrialization, urban expansion, and large-scale government investments in smart grids and renewable energy infrastructure, especially in countries like China, India, Japan, and South Korea. The region is aggressively advancing its energy transformation goals, integrating renewable power at a large scale, and deploying smart city solutions, all of which require advanced power distribution technologies like SSTs. The presence of major electronics and power system manufacturers further accelerates technology adoption, making Asia-Pacific the central hub for both production and deployment of SSTs across a variety of applications.

Meanwhile, North America is emerging as the fastest-growing region in the SST market, driven by a strong focus on grid modernization, electric vehicle infrastructure, and renewable energy integration. With increasing government incentives, pilot projects, and private sector involvement in digital power systems, the U.S. and Canada are rapidly transitioning toward smarter, more resilient energy networks. Solid-state transformers are being adopted to enhance substation performance, support EV charging systems, and improve grid flexibility. The region’s early adoption of advanced technologies, strong regulatory backing, and robust investment in R&D make North America the most dynamic growth engine in the SST market landscape.

COVID-19 Impact Analysis on the Global Solid-State Transformer Market:

The COVID-19 pandemic had a mixed impact on the global solid-state transformer market, initially slowing down growth because of disruptions in supply chains, project delays, and reduced capital expenditure across the energy and utility sectors. Manufacturing activities were paused, and several infrastructure projects were put on hold, affecting short-term demand. However, the crisis also accelerated long-term interest in resilient, digital, and energy-efficient systems, leading to renewed investments in smart grids, renewable integration, and EV infrastructure, all of which rely on advanced technologies like solid-state transformers.

Latest Trends/ Developments:

One of the latest trends in the solid-state transformer market is the rapid advancement in semiconductor technology, particularly the use of wide bandgap materials like silicon carbide (SiC) and gallium nitride (GaN). These materials significantly improve the performance, efficiency, and thermal management of SSTs, allowing them to operate at higher voltages and temperatures with reduced energy loss. This innovation is leading to the development of smaller, more powerful transformers that are well-suited for compact urban installations and mobile applications such as electric buses and trains. Additionally, modular SST designs are gaining popularity, offering scalability and easier integration into existing grid systems or new energy networks.

Another major development is the growing focus on SST-enabled bidirectional energy flow, especially for applications in electric vehicle charging and renewable energy systems. Solid-state transformers are being designed to seamlessly support vehicle-to-grid (V2G) capabilities, allowing stored energy in EVs to be fed back into the grid during peak demand. In the renewable sector, SSTs are playing a vital role in managing fluctuations in solar and wind power generation while maintaining grid stability. These emerging use cases are driving innovation in control software, cybersecurity features, and communication protocols, further pushing the evolution of SSTs from simple power conversion devices to intelligent grid assets.

Key Players:

• Hitachi (Japan)

• Schneider Electric (France)

• Siemens (Germany)

• Mitsubishi Electric (Japan)

• General Electric (US)

• Eaton (Ireland)

• Varentec (US)

• Amantys (UK)

• Ermco (US)

• SPX Transformer Solutions (US)

Chapter 1. Global Solid-State Transformer Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Solid-State Transformer Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Solid-State Transformer Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Solid-State Transformer Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Solid-State Transformer Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Solid-State Transformer Market – By Voltage Level

6.1. Introduction/Key Findings

6.2. HV/MV

6.3. MV/LV

6.4. Y-O-Y Growth trend Analysis By Voltage Level

6.5. Absolute $ Opportunity Analysis By Voltage Level, 2025-2030

Chapter 7. Global Solid-State Transformer Market – By Application

7.1. Introduction/Key Findings

7.2. Renewable Power Generation

7.3. Automotive

7.4. Power Grids

7.5. Traction Locomotives

7.6. Others

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Solid-State Transformer Market, By Geography – Market Size, Forecast, Trends & Insights

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Voltage Level

8.1.3. By Application

8.1.4. Countries & Segments – Market Attractiveness Analysis

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Voltage Level

8.2.3. By Application

8.2.4. Countries & Segments – Market Attractiveness Analysis

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia-Pacific

8.3.2. By Voltage Level

8.3.3. By Application

8.3.4. Countries & Segments – Market Attractiveness Analysis

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Voltage Level

8.4.3. By Application

8.4.4. Countries & Segments – Market Attractiveness Analysis

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. United Arab Emirates (UAE)

8.5.1.2. Saudi Arabia

8.5.1.3. Qatar

8.5.1.4. Israel

8.5.1.5. South Africa

8.5.1.6. Nigeria

8.5.1.7. Kenya

8.5.1.8. Egypt

8.5.1.9. Rest of MEA

8.5.2. By Voltage Level

8.5.3. By Application

8.5.4. Countries & Segments – Market Attractiveness Analysis

Chapter 9. Global Solid-State Transformer Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

9.1 Hitachi (Japan)

9.2 Schneider Electric (France)

9.3 Siemens (Germany)

9.4 Mitsubishi Electric (Japan)

9.5 General Electric (US)

9.6 Eaton (Ireland)

9.7 Varentec (US)

9.8 Amantys (UK)

9.9 Ermco (US)

9.10 SPX Transformer Solutions (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Solid-State Transformer Market was valued at USD 241.9 million in 2024 and is projected to reach a market size of USD 707.18 million by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.9%.

The global solid-state transformer market is driven by increasing smart grid adoption, renewable energy integration, and electric vehicle infrastructure development.

Based on Voltage Level, the Global Solid-State Transformer Market is segmented into HV/MV and MV/LV.

Asia-Pacific is the most dominant region for the Global Solid-State Transformer Market.

Hitachi (Japan), Schneider Electric (France), Siemens (Germany) are the leading players in the Global Solid-State Transformer Market.