Residential Lithium-ion Battery Energy Storage Systems Market Research Report – Segmentation by Type (Lithium-ion Phosphate (LFP), Nickel Manganese Cobalt (NMC), Other Chemistries); By Distribution Channel (Direct Sales, Installers/EPCs, Online Retailers, Third-Party Resellers); By Capacity (Less than 5 kWh, 5-10 kWh, Greater than 10 kWh); By Application (Solar Energy Storage, Backup Power, Grid Services, EV Charging Integration); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16551

Format:

Region: Global

Market Size and Overview:

The Residential Lithium-ion Battery Energy Storage System Market size was valued at USD 2.39 billion in 2024 and is projected to reach a market size of USD 4.67 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.36%.

The Residential Lithium-ion Battery Energy Storage Systems (BESS) market is undergoing a profound transformation, emerging as a pivotal component in the global shift towards decentralized and sustainable energy solutions. This dynamic market encompasses the development, manufacturing, distribution, and installation of lithium-ion battery systems specifically designed to store energy for residential applications. As the world increasingly embraces renewable energy sources like rooftop solar, these battery storage systems become indispensable, enabling homeowners to maximize self-consumption, achieve energy independence, and ensure power reliability. The market is characterized by rapid technological advancements, leading to more efficient, safer, and cost-effective battery solutions. These systems not only provide backup power during grid outages but also allow for energy arbitrage, where electricity is stored during off-peak hours when prices are low and discharged during peak demand. This evolution highlights a broader trend towards a more intelligent, resilient, and distributed energy infrastructure, with residential lithium-ion BESS at its core.

Key Market Insights:

Lithium-ion batteries held a dominant share of around 66.7% within the broader BESS market. Approximately 78% of new residential solar installations in developed markets were paired with battery storage systems.

Systems with a capacity of 3 kW to 5 kW accounted for over 52.6% of the residential market share.

Asia-Pacific emerged as the leading region, holding an estimated 42.6% market share in 2024.

The adoption of smart home energy management systems integrated with BESS increased by 35% in 2024. Roughly 70% of homeowners considering solar installations in 2024 also inquired about battery storage.

The U.S. residential lithium-ion battery energy storage system market was valued at USD 1,520.00 million in 2024. The Indian residential lithium-ion battery energy storage systems market was estimated at USD 144.78 million in 2024.

Global utility-scale energy storage cell shipments reached 180 GWh in the first three quarters of 2024, indicating overall strong battery manufacturing. Small-scale energy storage cell shipments, relevant to residential, reached 22.3 GWh in the first three quarters of 2024.

Market Drivers:

Growing Demand for Energy Independence and Resilience:

The increasing frequency of power outages due to aging grid infrastructure, extreme weather events, and natural disasters is a significant driver. Homeowners are increasingly seeking reliable backup power solutions to ensure uninterrupted electricity supply for essential appliances and systems. Beyond emergency preparedness, there's a growing desire for energy independence, allowing households to reduce their reliance on the centralized grid and gain more control over their energy consumption, especially when coupled with rooftop solar installations. This pursuit of resilience and autonomy fundamentally drives the adoption of residential lithium-ion battery energy storage systems.

Declining Battery Costs and Technological Advancements:

The continuous decline in the manufacturing cost of lithium-ion batteries, largely driven by economies of scale in electric vehicle production, has made residential energy storage systems more affordable and accessible. Coupled with this, ongoing technological advancements are enhancing battery efficiency, energy density, and lifespan. Innovations in battery chemistry, such as the increasing prevalence of Lithium Iron Phosphate (LFP) batteries, offer improved safety and longevity. These cost reductions and performance improvements make the return on investment more attractive for homeowners, accelerating market adoption.

Market Restraints and Challenges:

The residential lithium-ion battery energy storage market faces hurdles such as high initial upfront costs despite recent price drops, which can deter a significant portion of potential homeowners. Complex installation procedures requiring specialized expertise can also add to overall project expenses. Additionally, safety concerns related to thermal runaway and fire hazards, although rare with modern systems, can impact consumer perception and lead to stringent regulatory requirements. Developing adequate recycling infrastructure for end-of-life batteries also presents an environmental and logistical challenge.

Market Opportunities:

The integration of residential BESS with smart home energy management systems presents a major opportunity for optimized energy usage and seamless control. The expansion of virtual power plant (VPP) models allows homeowners to earn revenue by sharing their stored energy with the grid during peak demand. Furthermore, the growing adoption of electric vehicles (EVs) creates opportunities for bidirectional charging solutions (V2H/V2G), where residential batteries and EVs can form an integrated energy ecosystem. The development of more compact, modular, and aesthetically pleasing designs will also unlock new market segments.

Market Segmentation:

Segmentation by Type:

• Lithium-ion Phosphate (LFP)

• Nickel Manganese Cobalt (NMC)

• Other Chemistries

Lithium-ion Phosphate (LFP) batteries are rapidly gaining traction as the fastest-growing type due to their enhanced safety characteristics, longer cycle life, and lower cost compared to other lithium-ion chemistries. Their thermal stability reduces the risk of thermal runaway, making them a preferred choice for residential applications where safety is paramount, while their cost-effectiveness further accelerates adoption.

Nickel Manganese Cobalt (NMC) batteries currently hold the most dominant position in the market, largely due to their higher energy density, which allows for smaller and lighter battery packs. While LFP is rapidly growing, NMC's established market presence and performance characteristics, particularly in applications requiring a balance of energy density and power delivery, have maintained its lead.

Segmentation by Distribution Channel:

• Direct Sales

• Installers/EPCs

• Online Retailers

• Third-Party Resellers

The Installers/EPCs channel is experiencing the fastest growth. This is driven by the increasing complexity of integrating residential BESS with solar PV systems and home electrical infrastructures, necessitating professional installation and system design. Homeowners often prefer a complete, hassle-free solution provided by specialized energy system installers, fostering strong growth in this channel.

Direct sales remain the most dominant distribution channel, particularly for established battery manufacturers with strong brand recognition. This channel allows for direct engagement with customers, providing comprehensive product information, customized solutions, and direct support. For high-value purchases like residential battery systems, direct sales often foster greater trust and ensure tailored solutions for specific homeowner needs.

Segmentation by Capacity:

• Less than 5 kWh

• 5-10 kWh

• Greater than 10 kWh

The "Greater than 10 kWh" capacity segment is the fastest-growing. This trend is fueled by homeowners' increasing desire for extended backup power durations, larger solar PV installations necessitating more storage, and the pursuit of higher levels of energy independence. As more energy-intensive appliances and electric vehicle charging become common, larger storage capacities are becoming increasingly necessary.

The 5-10 kWh capacity range is the most dominant segment in the residential lithium-ion battery energy storage market. This capacity strikes an optimal balance between meeting the average household's daily energy needs for self-consumption and backup, while also remaining relatively cost-effective. It provides sufficient energy independence for most residential applications without excessive upfront investment.

Segmentation by Application:

• Solar Energy Storage

• Backup Power

• Grid Services

• EV Charging Integration

EV Charging Integration is rapidly emerging as the fastest-growing application. With the surging adoption of electric vehicles, homeowners are looking to integrate their EV charging with their home energy systems, often utilizing solar-plus-storage. This allows for optimized charging during off-peak hours or from self-generated solar power, minimizing utility costs and maximizing sustainability.

Solar Energy Storage is the most dominant application for residential lithium-ion battery energy storage systems. The widespread adoption of rooftop solar panels creates a fundamental need for battery storage to capture excess solar generation during the day for use during evenings or cloudy periods, maximizing self-consumption and reducing reliance on the grid. This symbiotic relationship is a primary market driver.

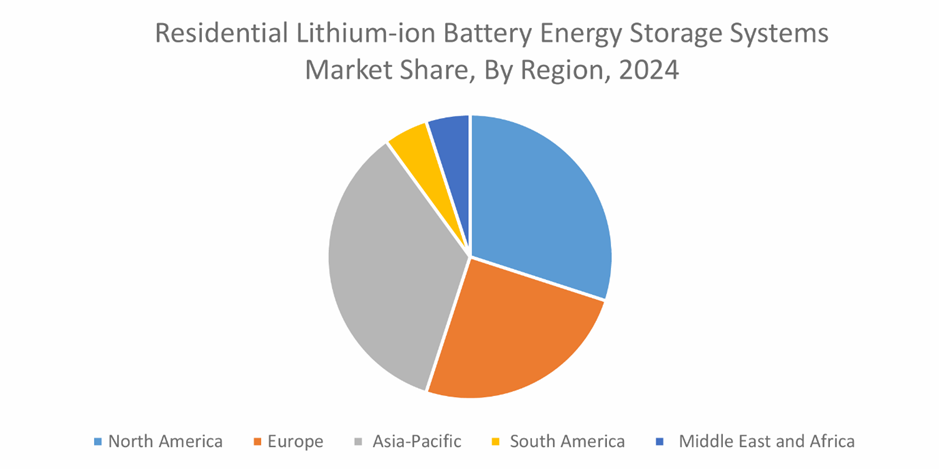

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

Asia-Pacific currently holds the largest market share in the residential lithium-ion battery energy storage systems market, estimated at around 42.6% in 2024. This dominance is attributed to robust government support for renewable energy, rapid urbanization, and a high rate of solar PV installations in countries like China, Japan, and Australia, coupled with increasing energy demand.

Asia-Pacific is also the fastest-growing region. This accelerated growth is propelled by ambitious renewable energy targets, significant investments in smart grid infrastructure, and the declining cost of lithium-ion batteries making storage solutions more accessible. Government incentives and increasing consumer awareness regarding energy independence further contribute to its rapid expansion.

COVID-19 Impact Analysis:

The COVID-19 pandemic significantly underscored the importance of energy resilience and home-based energy solutions, boosting the residential lithium-ion battery energy storage market. Supply chain disruptions initially posed challenges, but the increased focus on self-sufficiency and uninterrupted power during lockdowns led to a surge in demand. Consumers became more aware of grid vulnerabilities, accelerating investments in solar-plus-storage systems for enhanced energy security and independence in their homes.

Latest Trends and Developments:

The market is witnessing a strong trend towards modular and scalable battery systems, allowing homeowners to easily expand their storage capacity as needs evolve. The integration of artificial intelligence (AI) and machine learning (ML) for intelligent energy management is optimizing battery performance, predicting consumption patterns, and enabling seamless participation in virtual power plants. Furthermore, advancements in battery chemistry, particularly the growing prominence of Lithium Iron Phosphate (LFP) due to its safety and cost-effectiveness, are reshaping product offerings. The development of aesthetically pleasing, compact designs that blend into residential environments is also a key focus for manufacturers.

Key Players in the Market:

• HAIKAI

• Enphase Energy

• E3/DC

• Panasonic

• sonnen Holding GmbH

• Tesla

• Pylon Technologies Co., Ltd

• LG Chem

• AlphaESS

• Generac Power Systems

Chapter 1. Global Residential Lithium-ion Battery Energy Storage Systems –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Residential Lithium-ion Battery Energy Storage Systems – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Residential Lithium-ion Battery Energy Storage Systems – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Residential Lithium-ion Battery Energy Storage Systems Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Residential Lithium-ion Battery Energy Storage Systems - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Residential Lithium-ion Battery Energy Storage Systems Market – By Type

6.1. Introduction/Key Findings

6.2. Lithium-ion Phosphate (LFP)

6.3. Nickel Manganese Cobalt (NMC)

6.4. Other Chemistries

6.5. Y-O-Y Growth trend Analysis By Type

6.6. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global Residential Lithium-ion Battery Energy Storage Systems Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Direct Sales

7.3. Installers/EPCs

7.4. Online Retailers

7.5. Third-Party Resellers

7.6. Y-O-Y Growth trend Analysis By Distribution Channel

7.7. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global Residential Lithium-ion Battery Energy Storage Systems Market – By Capacity

8.1. Introduction/Key Findings

8.2. Less than 5 kWh

8.3. 5-10 kWh

8.4. Greater than 10 kWh

8.5. Y-O-Y Growth trend Analysis By Capacity

8.6. Absolute $ Opportunity Analysis By Capacity, 2024-2030

Chapter 9. Global Residential Lithium-ion Battery Energy Storage Systems Market – By Application

9.1. Introduction/Key Findings

9.2. Solar Energy Storage

9.3. Backup Power

9.4. Grid Services

9.5. EV Charging Integration

9.6. Y-O-Y Growth trend Analysis By Application

9.7. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 10. Global Residential Lithium-ion Battery Energy Storage Systems , By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By Capacity

10.1.5. By Application

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By Capacity

10.2.5. By Application

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By Capacity

10.3.5. By Application

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Application

10.4.4. By Capacity

10.4.5. By Application

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Distribution Channel

10.5.4. By Capacity

10.5.5. By Application

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Residential Lithium-ion Battery Energy Storage Systems – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. HAIKAI

11.2. Enphase Energy

11.3. E3/DC

11.4. Panasonic

11.5. sonnen Holding GmbH

11.6. Tesla

11.7. Pylon Technologies Co., Ltd

11.8. LG Chem

11.9. AlphaESS

11.10. Generac Power Systems

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The increasing demand for energy independence and resilience due to grid vulnerabilities, coupled with the continuous decline in lithium-ion battery costs and ongoing technological advancements enhancing efficiency and lifespan, are the primary drivers.

The market faces challenges such as the relatively high initial upfront installation costs, the complexity involved in system integration, and ongoing concerns regarding the safety of lithium-ion batteries, necessitating robust safety standards and consumer education.

Prominent players include LG Energy Solution, Enphase Energy, Tesla, Sonnen GmbH, BYD Company Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Alpha ESS Co., Ltd., Huawei Technologies Co., Ltd., GoodWe Technologies Co., Ltd.,Solaredge Technologies Inc., Generac Power Systems, Inc., Pylon Technologies Co., Ltd., E3/DC GmbH, and SolaX Power Network Technology (Zhejiang) Co., Ltd.

Asia-Pacific currently holds the largest market share, estimated at around 42.6% in 2024, driven by strong government support for renewables and high solar PV adoption.

. Asia-Pacific is also expanding at the highest rate, fueled by ambitious renewable energy targets, significant investments in smart grid infrastructure, and declining battery costs making solutions more accessible to homeowners across the region.