QR Code Payment Market Research Report – Segmentation by Type (Static QR Code, Dynamic QR Code); By Distribution Channel (Mobile Wallets, Banking Apps, Merchant-specific Apps, Third-party Payment Aggregators); By End-User (Retail & E-commerce, Hospitality & Tourism, Transportation & Logistics, Healthcare, Others); By Transaction Type (Person-to-Merchant (P2M), Person-to-Person (P2P)); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16560

Format:

Region: Global

Market Size and Overview:

The QR Code Payment Market was valued at USD 12.2 Billion in 2024 and is projected to reach a market size of USD 28.51 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 18.5%.

The QR Code Payment Market represents a paradigm shift in the global financial technology landscape, evolving from a novel concept into a cornerstone of modern digital commerce. This market revolves around the use of Quick Response (QR) codes—two-dimensional matrix barcodes—to initiate, authorize, and complete transactions, effectively creating a frictionless bridge between the physical and digital worlds. The ecosystem is a complex interplay of consumers armed with smartphones, merchants seeking efficient payment solutions, financial institutions adapting to new technologies, and fintech innovators driving the evolution. The market's meteoric rise is fundamentally tethered to the near-universal proliferation of smartphones, which serve as the primary hardware for both scanning and generating these codes. This continuous innovation, combined with its foundational strengths of convenience, cost-effectiveness, and security, ensures that the QR code payment market will remain a dynamic and influential force in the future of global finance.

Key Market Insights:

A significant milestone was reached as an estimated 55% of all smartphone users worldwide made at least one QR code payment during the year.

The average transaction value for Person-to-Merchant (P2M) payments stood at approximately $27, while Person-to-Person (P2P) transfers averaged around $45.

Adoption among small and medium-sized enterprises (SMEs) surged, with nearly 60% of SMEs in developing economies accepting QR payments as their primary digital payment method.

In the retail sector, QR codes accounted for an estimated 18% of all digital payment transactions by volume.

The volume of cross-border QR code transactions grew by over 200% in 2024, facilitated by new interoperability agreements.

Dynamic QR codes, which are generated for each specific transaction, accounted for over 40% of the total transaction value, signaling a shift towards more secure and data-rich payment methods.

Market Drivers:

Surge in Smartphone Proliferation and Digital Literacy

The ubiquity of the smartphone is the bedrock upon which the entire QR code payment market is built. As devices become more affordable and powerful, they have penetrated every demographic and geographic corner of the globe. This widespread ownership, coupled with a steady increase in digital literacy and consumer comfort with app-based services, has created a fertile ground for QR code adoption. Consumers are no longer intimidated by new financial technologies; they expect them. The intuitive "point-and-shoot" nature of QR payments removes significant friction, making it accessible even to those with limited technical skills, thereby driving mass adoption.

Push for Financial Inclusion and Cashless Economies

Governments and financial institutions worldwide are championing QR codes as a powerful tool for economic modernization. For the unbanked and underbanked populations, QR payments offer a simple on-ramp to the formal digital economy, bypassing the need for traditional bank accounts or credit cards. Simultaneously, this technology is a key enabler for national initiatives aimed at reducing reliance on physical cash, which helps curb the grey economy, reduce the costs of printing and managing currency, and enhance transactional transparency. This top-down support, often coupled with national standardized QR systems, provides significant momentum for market growth.

Market Restraints and Challenges:

The market's rapid expansion is not without its hurdles. A primary concern is the potential for security vulnerabilities, such as QR code phishing (quishing), where malicious codes redirect users to fake websites to steal credentials. Another significant restraint is the fragmentation of the market; a lack of interoperability between different payment apps and national standards can create a confusing and siloed user experience. Furthermore, the system's absolute dependence on a stable internet connection and adequate smartphone battery life renders it unusable during outages or in areas with poor connectivity.

Market Opportunities:

Immense opportunities lie in the integration of QR payments with emerging technologies. Embedding QR codes within IoT devices and connected vehicles can automate payments for services like parking, tolling, and electric vehicle charging. The expansion of cross-border interoperable QR networks presents a massive opportunity to simplify payments for international tourists and business travelers. There is also significant untapped potential in value-added services, such as offering instant micro-loans or "buy now, pay later" (BNPL) options at the point of sale, directly through the payment interface.

Market Segmentation:

Segmentation by Type:

• Static QR Code

• Dynamic QR Code

Dynamic QR codes represent the fastest-growing segment, prized for their superior security and data-handling capabilities. Because a unique code is generated for each individual transaction, it significantly reduces the risk of fraud. Merchants favour this type as it can be pre-filled with the exact payment amount, eliminating cashier errors.

Static QR codes remain the most dominant type due to their sheer simplicity and zero-cost implementation. A single printed code can be used for countless transactions, making it the go-to solution for millions of small merchants, street vendors, and individuals for P2P payments, thus commanding the highest volume of adoption.

Segmentation by Distribution Channel:

• Mobile Wallets

• Banking Apps

• Merchant-specific Apps

• Third-party Payment Aggregators

Banking apps are the fastest-growing channel as traditional financial institutions race to integrate QR functionality directly into their existing mobile platforms. This strategy leverages their established customer base and high levels of user trust, effectively retaining clients within their ecosystem and competing directly with fintech-led mobile wallets without requiring a separate download.

Mobile wallets, particularly super-apps like Alipay and WeChat Pay, continue to dominate the market. They pioneered the QR code payment revolution and have built massive, deeply integrated ecosystems that combine payments with social media, e-commerce, and lifestyle services, ensuring high user engagement and massive transaction volumes.

Segmentation by End-User:

• Retail & E-commerce

• Hospitality & Tourism

• Transportation & Logistics

• Healthcare

• Others

The transportation and logistics sector is the fastest-growing adopter of QR code payments. The technology is ideal for the high-volume, low-value transactions common in public transit ticketing, bike-sharing services, and parking fees. Its speed and contactless nature dramatically improve efficiency and customer throughput in these fast-paced environments.

Retail & E-commerce is the most dominant end-user segment by a significant margin. From multinational hypermarkets to local corner stores and online checkouts, QR codes provide a versatile, low-cost alternative to traditional card payments. Their ubiquity in this sector makes it the largest contributor to overall transaction value and volume.

Segmentation by Transaction Type:

• Person-to-Merchant (P2M)

• Person-to-Person (P2P)

P2P transactions are witnessing explosive growth. The sheer convenience of scanning a friend's QR code to split a bill, pay a local service provider, or send money to family has driven rapid adoption. This segment is fueled by social payment trends and the increasing digitization of informal economic activities.

P2M remains the dominant transaction type, forming the commercial backbone of the QR code economy. Every payment for a good or service at a physical or online store falls into this category. This segment represents the largest flow of money from consumers to businesses, defining the market's overall size.

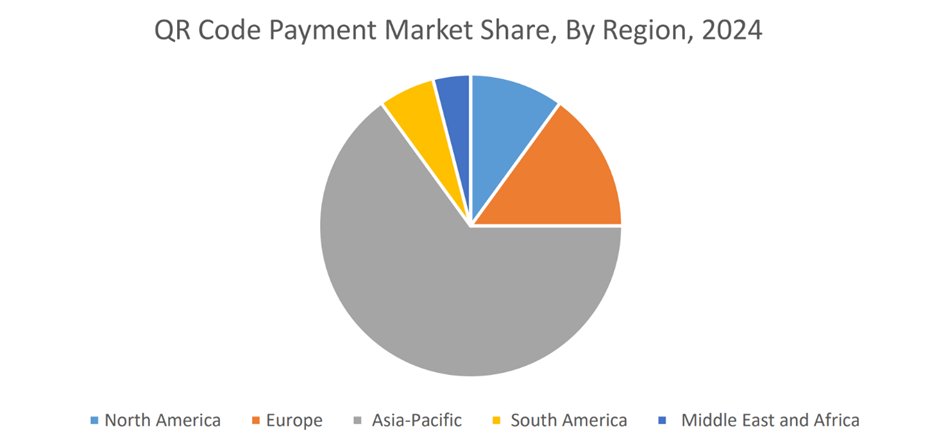

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

The Asia-Pacific region is the undisputed global epicenter of QR code payments. Led by powerhouse markets like China and India, deep-rooted adoption has been driven by government policies promoting digitalization, massive smartphone penetration, and the dominance of super-apps that have made QR codes a default payment method for hundreds of millions.

South America is the market's fastest-growing region, experiencing a surge in adoption fueled by financial inclusion initiatives. Programs like Brazil's Pix system have leveraged QR codes to bring millions into the digital economy, leading to exponential growth in user and merchant uptake as the region embraces a digital-first financial model.

COVID-19 Impact Analysis:

The COVID-19 pandemic served as an unprecedented accelerator for the QR code payment market. The global imperative for contactless interactions transformed the technology from a convenience into a perceived necessity. Consumers and merchants, driven by health and safety concerns, actively shifted away from cash and physical cards. This created a massive surge in adoption as QR codes offered a truly touch-free payment experience. Governments also leveraged the technology for health passes and aid distribution, further normalizing its presence in daily life and cementing its role as a resilient and essential payment method.

Latest Trends and Developments:

The current frontier of innovation involves creating globally interoperable QR networks, a trend allowing travelers to use their domestic payment apps seamlessly in foreign countries. Another key development is the fortification of security through the integration of biometrics; payment apps are increasingly using fingerprint or facial recognition to authorize QR transactions, adding a robust layer of user-specific protection. Furthermore, the "Scan and Go" retail model, where customers self-scan item barcodes and pay via a QR code in-app to bypass checkout queues, is gaining significant traction.

Key Players in the Market:

• Alipay (Ant Group)

• WeChat Pay (Tencent)

• PayPal

• Block, Inc. (Square, Cash App)

• Paytm

• PhonePe

• Google Pay

• Apple Inc.

• Samsung Pay

• UnionPay International

Chapter 1. Global QR Code Payment Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global QR Code Payment Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global QR Code Payment Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global QR Code Payment Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global QR Code Payment Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global QR Code Payment Market – By Type

6.1. Introduction/Key Findings

6.2. Static QR Code

6.3. Dynamic QR Code

6.4. Y-O-Y Growth trend Analysis By Type

6.5. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global QR Code Payment Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Mobile Wallets

7.3. Banking Apps

7.4. Merchant-specific Apps

7.5. Third-party Payment Aggregators

7.6. Y-O-Y Growth trend Analysis By Distribution Channel

7.7. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global QR Code Payment Market – By End-User

8.1. Introduction/Key Findings

8.2. Retail & E-commerce

8.3. Hospitality & Tourism

8.4. Transportation & Logistics

8.5. Healthcare

8.6. Others

8.7. Y-O-Y Growth trend Analysis By End-User

8.8. Absolute $ Opportunity Analysis By End-User, 2024-2030

Chapter 9. Global QR Code Payment Market – By Transaction Type

9.1. Introduction/Key Findings

9.2. Person-to-Merchant (P2M)

9.3. Person-to-Person (P2P)

9.4. Y-O-Y Growth trend Analysis By Transaction Type

9.5. Absolute $ Opportunity Analysis By Transaction Type, 2024-2030

Chapter 10. Global QR Code Payment Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By End-User

10.1.5. By Transaction Type

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By End-User

10.2.5. By Transaction Type

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By End-User

10.3.5. By Transaction Type

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Distribution Channel

10.4.4. By End-User

10.4.5. By Transaction Type

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.4.2. By Type

10.5.3. By Distribution Channel

10.5.4. By End-User

10.5.5. By Transaction Type

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global QR Code Payment Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Alipay (Ant Group) (China)

11.2. WeChat Pay (Tencent) (China)

11.3. PayPal (US)

11.4. Block, Inc. (Square, Cash App) (US)

11.5. Paytm (India)

11.6. PhonePe (India)

11.7. Google Pay (US)

11.8. Apple Inc. (US)

11.9. Samsung Pay (South Korea)

11.10. UnionPay International (China)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary drivers are the massive global proliferation of smartphones and rising digital literacy, which make the technology accessible to billions. Additionally, strong support from governments and financial institutions promoting financial inclusion and the transition to cashless economies provides a significant top-down push for market expansion.

The main challenges include managing security risks like QR code phishing (quishing), overcoming market fragmentation caused by a lack of interoperability between different payment systems, and addressing the system's reliance on stable internet connectivity and smartphone power, which can limit its use in certain conditions.

Key players include Alipay (Ant Group), WeChat Pay (Tencent), PayPal, Block, Inc., Paytm, PhonePe, Google Pay, Apple Inc., Samsung Pay, UnionPay International, Adyen, Stripe, Mercado Pago, Zelle, and GCash.

The Asia-Pacific region holds the largest market share by a significant margin, currently estimated at around 65%, driven by mass adoption in countries like China and India.

South America is the fastest-growing region. This expansion is powered by strong financial inclusion initiatives, such as Brazil's Pix system, which are rapidly bringing millions of new users and merchants into the digital payment ecosystem.