Power Grid Systems Market Research Report - Segmentation by Component (Hardware, Software, Services); By Grid Type (Smart Grid, Traditional Grid); By Voltage (High Voltage, Medium Voltage, Low Voltage); By Application (Generation, Transmission, Distribution); By End-User (Utilities, Industrial, Commercial, Residential); Region - Forecast (2025 - 2030)

Published: 2025 - June

Report Code: IM-16583

Format:

Region: Global

Market Size and Overview:

The Power Grid Systems Market was valued at USD 289.45 billion in 2024 and is projected to reach a market size of USD 400.31 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 6.7%.

Power Grid Systems represent the interconnected network of electrical components used to supply, transmit, and distribute electric power from producers to consumers. This critical infrastructure has undergone significant transformation in the 21st century with the integration of smart technologies, renewable energy sources, and advanced monitoring systems. With the continuous evolution of energy demands and the global shift toward sustainable power generation, the demand for modernized grid infrastructure is rapidly increasing and is anticipated to create substantial opportunities across various sectors including utilities, industrial applications, and residential energy management.

Key Market Insights:

According to the International Energy Agency (IEA), global electricity grid investments reached USD 310 billion in 2022, representing a 12% increase from the previous year.

Approximately 64% of these investments were allocated to grid modernization projects, with smart grid technologies accounting for 28% of total grid infrastructure spending. This substantial investment trend reflects the critical importance of upgrading aging power infrastructure to support renewable energy integration.

A comprehensive survey conducted by the Global Smart Grid Federation involving 750 utility executives revealed that 78% of utilities experienced a 23% reduction in power outages after implementing smart grid technologies. Additionally, 71% of respondents reported average energy efficiency improvements of 18% across their distribution networks, resulting in significant operational cost savings and enhanced customer satisfaction metrics.

Research from the Electric Power Research Institute (EPRI) indicates that utilities deploying advanced grid management systems achieved an average 34% improvement in fault detection and restoration times. The study also found that modern grid systems with integrated automation capabilities reduced maintenance costs by approximately 27% while increasing system reliability ratings by 31% compared to traditional grid infrastructure implementations.

Power Grid Systems Market Drivers:

The increasing global electricity demand coupled with aging power infrastructure and the urgent need for grid modernization are fundamentally driving the expansion of the power grid systems market worldwide.

Global electricity consumption has grown exponentially, with the International Energy Agency projecting a 28% increase in electricity demand by 2030, driven primarily by industrialization in emerging economies, electrification of transportation systems, and the proliferation of digital technologies requiring reliable power supply. This surge in demand is placing unprecedented stress on existing power grid infrastructure, much of which was designed and installed decades ago with significantly lower capacity requirements. In the United States alone, approximately 70% of transmission lines are over 25 years old, while many distribution systems exceed their original design lifespans, creating urgent replacement and upgrade requirements. The European Union has identified over EUR 584 billion in grid infrastructure investment needs through 2030 to support decarbonization goals and ensure reliable electricity supply. Aging infrastructure presents multiple challenges including increased maintenance costs, higher failure rates, and reduced efficiency, with utilities reporting average annual maintenance cost increases of 8-12% for grid assets over 20 years old. Modern grid systems offer substantial improvements in efficiency, reliability, and controllability, with advanced monitoring and automation capabilities enabling utilities to optimize power flows, reduce losses, and respond more quickly to system disturbances. The integration of renewable energy sources requires sophisticated grid management capabilities that traditional infrastructure cannot provide, including real-time load balancing, voltage regulation, and frequency control across distributed generation sources.

The rapid integration of renewable energy sources and the advancement of smart grid technologies are accelerating the transformation of traditional power grid systems into intelligent, adaptive networks.

The global transition toward renewable energy has created fundamental changes in power generation patterns, with solar and wind capacity additions accounting for over 90% of new power generation capacity in 2022. This shift presents significant technical challenges for traditional grid systems, which were designed for centralized, controllable power generation rather than the variable, distributed nature of renewable sources. Modern grid systems incorporate advanced forecasting algorithms, energy storage integration, and demand response capabilities that enable utilities to manage renewable energy variability while maintaining grid stability. Smart grid technologies have demonstrated the ability to accommodate up to 50% renewable energy penetration without compromising system reliability, compared to 15-20% limits for traditional grid configurations.

Power Grid Systems Market Restraints and Challenges:

The power grid systems market faces significant challenges that could impede its growth trajectory, particularly the substantial capital investment requirements and lengthy regulatory approval processes. Grid modernization projects typically require investment periods of 10-15 years with complex financing structures that can strain utility balance sheets and require regulatory rate adjustments. Cybersecurity concerns have intensified with increased digitalization, as utilities face approximately 40,000 cyberattacks annually according to security reports, necessitating substantial investments in protective systems and protocols. Technical integration challenges persist when connecting legacy infrastructure with modern smart grid components, often requiring extensive system testing and gradual migration approaches that extend implementation timelines. Skilled workforce shortages in electrical engineering and grid operations have become critical bottlenecks, with the Edison Electric Institute reporting that 25% of utility workers will reach retirement age within the next five years. Regulatory complexity varies significantly across jurisdictions, creating uncertainty for manufacturers and utilities planning large-scale deployments.

Power Grid Systems Market Opportunities:

The power grid systems market presents substantial growth opportunities driven by the global energy transition and emerging technology integration requirements. Energy storage system integration represents a particularly promising opportunity, with battery storage deployments growing at 34% annually and requiring sophisticated grid interface technologies to optimize performance and revenue streams. Electric vehicle infrastructure development creates demand for specialized grid solutions including high-power charging networks, vehicle-to-grid integration capabilities, and load management systems that can accommodate transportation electrification without destabilizing power systems. Developing nations present significant market opportunities as they build new power infrastructure, with many countries leapfrogging to modern grid technologies rather than installing traditional systems. Microgrids and distributed energy resource management offer growing market segments, particularly for industrial and commercial customers seeking energy independence and resilience.

Power Grid Systems Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

The hardware segment dominated the global power grid systems market with approximately 58.7% revenue share. This dominance reflects the capital-intensive nature of grid infrastructure, where physical components such as transformers, switchgear, transmission lines, and distribution equipment represent the largest portion of project costs. The hardware segment includes both traditional electrical equipment and modern smart grid devices, with advanced metering infrastructure and intelligent electronic devices showing particularly strong growth rates.

The services segment is projected to grow at the fastest CAGR of approximately 8.9% during the forecast period, driven by increasing complexity of modern grid systems and the need for specialized expertise in deployment, maintenance, and optimization. This growth encompasses system integration services, consulting, maintenance contracts, and managed services offerings. The software segment, while smaller in absolute terms, is experiencing rapid expansion due to the increasing digitalization of grid operations and the deployment of advanced analytics, automation, and control systems across utility networks.

Market Segmentation: By Grid Type

• Smart Grid

• Traditional Grid

The smart grid segment accounted for approximately 39.3% of the market share in 2024 and is projected to grow at the highest CAGR of 9.7% during the forecast period. This accelerated growth is driven by government initiatives promoting grid modernization, the need for renewable energy integration, and increasing focus on energy efficiency and reliability. Smart grid deployments offer utilities advanced monitoring, control, and optimization capabilities that traditional systems cannot provide.

The traditional grid segment, while still representing a significant portion of the market, is experiencing slower growth as utilities gradually transition to modernized infrastructure. However, this segment remains important in regions with developing power infrastructure and areas where immediate smart grid deployment is not economically feasible. Many traditional grid projects now incorporate some smart technologies, creating a hybrid approach to grid development that balances cost considerations with modernization objectives.

Market Segmentation: By Voltage

• High Voltage (Above 35 kV)

• Medium Voltage (1 kV to 35 kV)

• Low Voltage (Below 1 kV)

The high voltage segment dominated the market with a 46.8% share, reflecting the critical importance of transmission infrastructure in power system operations. High voltage systems carry bulk power over long distances and require sophisticated equipment and monitoring systems to ensure stability and reliability. This segment includes major transmission line projects, substations, and interconnection facilities that form the backbone of power systems.

The medium voltage segment is projected to experience the highest growth rate during the forecast period, driven by distribution system modernization and the integration of distributed energy resources. Medium voltage systems serve as the critical link between high voltage transmission and low voltage distribution, requiring advanced control and monitoring capabilities to manage bidirectional power flows and maintain system stability in increasingly complex distribution networks.

Market Segmentation: By Application

• Generation

• Transmission

• Distribution

The distribution segment held the largest market share of approximately 41.2%, reflecting the extensive nature of distribution networks that directly serve end customers. Distribution system modernization requires significant investment in smart meters, automated switches, voltage regulators, and communication infrastructure to enable advanced grid management capabilities. This segment benefits from regulatory initiatives promoting customer choice and renewable energy integration at the distribution level.

The transmission segment is expected to grow at a CAGR of 7.8% during the forecast period, driven by the need for long-distance renewable energy transport and grid interconnection projects. Transmission infrastructure requires high-capacity, reliable equipment capable of managing variable power flows from distributed renewable sources while maintaining system stability across large geographic areas.

Market Segmentation: By End-User

• Utilities

• Industrial

• Commercial

• Residential

The utilities segment dominated the power grid systems market with a 67.4% share, as electric utilities are the primary operators and investors in power grid infrastructure. Utility investments encompass generation, transmission, and distribution assets, with increasing focus on smart grid technologies, renewable integration, and system resilience. Regulatory frameworks typically require utilities to maintain and upgrade grid infrastructure to meet reliability and service quality standards.

The industrial segment is projected to witness the highest growth rate during the forecast period, driven by increasing demand for reliable power supply, energy efficiency improvements, and on-site generation capabilities. Industrial customers are investing in private distribution networks, microgrids, and energy management systems that require sophisticated grid interface technologies and control systems to optimize operations and costs.

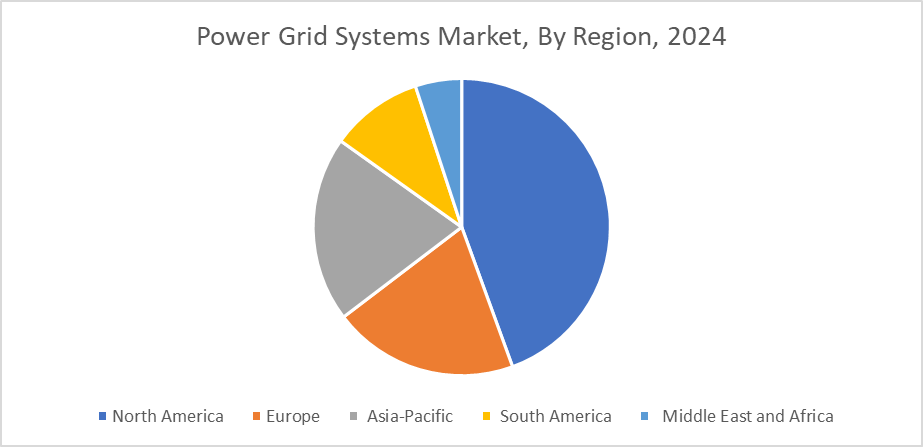

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America led the global power grid systems market in 2024 with approximately 34.6% of the total market share. This leadership position is attributed to extensive grid modernization initiatives, substantial utility capital expenditure programs, and supportive regulatory frameworks promoting smart grid deployment. The United States has invested over USD 130 billion in grid infrastructure since 2010, with continued emphasis on resilience and renewable integration driving ongoing market growth.

The Asia-Pacific region is anticipated to witness the highest CAGR of 8.2% during the forecast period, driven by rapid industrialization, urbanization, and electrification initiatives across emerging economies. Countries such as China, India, and Southeast Asian nations are making substantial investments in power infrastructure to support economic development, with China alone accounting for over 40% of global grid investment in recent years. The region's focus on renewable energy deployment and smart city initiatives further supports accelerated market growth.

COVID-19 Impact Analysis on the Global Power Grid Systems Market:

The COVID-19 pandemic initially created disruptions in power grid system projects due to supply chain interruptions, workforce restrictions, and delayed regulatory approvals. However, the crisis ultimately highlighted the critical importance of reliable electricity infrastructure for supporting remote work, healthcare systems, and essential services. Many utilities accelerated their digital transformation initiatives and smart grid deployments to improve operational efficiency and enable remote monitoring and control capabilities.

Government stimulus packages worldwide included substantial allocations for infrastructure modernization, with many countries prioritizing clean energy and grid resilience projects as part of economic recovery efforts. The pandemic also accelerated trends toward distributed energy resources and microgrids as organizations sought greater energy security and independence. Long-term impacts include increased focus on grid cybersecurity, remote operations capabilities, and resilient infrastructure design that can maintain service during future disruptions. These changes have created lasting market opportunities for advanced grid technologies and services that support flexible, reliable power system operations in an increasingly uncertain environment.

Latest Trends/ Developments:

The integration of artificial intelligence and machine learning technologies into grid operations is revolutionizing power system management through predictive analytics, automated optimization, and intelligent fault detection capabilities. Leading utilities are deploying AI-powered systems that can analyze vast amounts of sensor data to predict equipment failures, optimize power flows, and automatically respond to system disturbances, resulting in significant improvements in reliability and operational efficiency.

Blockchain technology adoption is gaining momentum for peer-to-peer energy trading applications and renewable energy certificate management, enabling new business models and market structures that support distributed energy resource participation. Several pilot projects have demonstrated blockchain's potential for facilitating energy transactions between prosumers and creating transparent, automated settlement systems for grid services.

Key Players:

• Siemens AG

• General Electric Company

• ABB Ltd.

• Baker Huges

• Prysimian

• Nexans.

• Schlumberger

• Hitachi Energy Ltd.

• Mitsubishi Electric Corporation

• Toshiba Corporation

Chapter 1. Power Grid Systems Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Power Grid Systems Market – Executive Summary

2.1. Market Application & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Power Grid Systems Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Power Grid Systems Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Power Grid Systems Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Power Grid Systems Market – By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Power Grid Systems Market – By Voltage

7.1. Introduction/Key Findings

7.2. High Voltage

7.3. Medium Voltage

7.4. Low Voltage

7.5. Y-O-Y Growth trend Analysis By Voltage

7.6. Absolute $ Opportunity Analysis By Voltage, 2025-2030

Chapter 8. Power Grid Systems Market – By Grid Type

8.1. Introduction/Key Findings

8.2. Smart Grid

8.3. Traditional Grid

8.4. Y-O-Y Growth trend Analysis By Grid Type

8.4. Absolute $ Opportunity Analysis By Grid Type, 2025-2030

Chapter 9. Power Grid Systems Market – By Application

9.1. Introduction/Key Findings

9.2. Generation

9.3. Transmission

9.4. Distribution

9.5. Y-O-Y Growth trend Analysis By Application

9.6. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 10. Power Grid Systems Market – By End User

10.1. Introduction/Key Findings

10.2. Utilities

10.3. Industrial

10.4. Commercial

10.5. Residential

10.6. Others

10.7. Y-O-Y Growth trend Analysis By End User

10.8. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 11. Power Grid Systems Market, By Geography – Market Application, Forecast, Trends & Insights

11.1. North America

11.1.1. By Country

11.1.1.1. U.S.A.

11.1.1.2. Canada

11.1.1.3. Mexico

11.1.2. By Component

11.1.3. By Voltage

11.1.4. By Grid System

11.1.5. By Application

11.1.6. By End User

11.1.7. Countries & Segments – Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Component

11.2.3. By Voltage

11.2.4. By Grid System

11.2.5. By Application

11.2.6. By End User

11.2.7. Countries & Segments – Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.1. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Component

11.3.3. By Voltage

11.3.4. By Grid System

11.3.5. By Application

11.3.6. By End User

11.3.7. Countries & Segments – Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Component

11.4.3. By Voltage

11.4.4. By Grid System

11.4.5. By Application

11.4.6. By End User

11.4.7. Countries & Segments – Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.8. Egypt

11.5.1.9. Rest of MEA

11.5.2. By Component

11.5.3. By Voltage

11.5.4. By Grid System

11.5.5. By Application

11.5.6. By End User

11.5.7. Countries & Segments – Market Attractiveness Analysis

Chapter 12. Power Grid Systems Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

12.1. Siemens AG

12.2. General Electric Company

12.3. ABB Ltd.

12.4. Baker Hughes

12.5. Prysmian

12.6. Nexans

12.7. Schlumberger

12.8. Hitachi Energy Ltd.

12.9. Mitsubishi Electric Corporation

12.10. Toshiba Corporation

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Power Grid Systems Market was valued at USD 289.45 billion in 2024 and is projected to reach a market size of USD 400.31 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 6.7%.

The increasing global electricity demand coupled with aging power infrastructure and the urgent need for grid modernization are the primary drivers propelling the global power grid systems market.

Based on Component, the Global Power Grid Systems Market is segmented into Hardware, Software, and Services.

North America is the most dominant region for the Global Power Grid Systems Market.

Siemens AG, General Electric Company, ABB Ltd., and Schneider Electric SE are the key players operating in the Global Power Grid Systems Market.