Phase Change Materials Market Research Report – By Type (Bio-Based PCM, Organic PCM, and Inorganic PCM); By Form (Encapsulated and Non-Encapsulated); By Application (Textiles, Building and Construction, Cold Chain & Packaging, Electronics, Thermal Energy Storage and Others); and Region - Size, Share, Growth Analysis | Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16586

Format:

Region: Global

Market Size and Overview:

The Phase Change Materials Market was valued at USD 839 million in 2024. Over the forecast period of 2025-2030 it is projected to reach USD 1.75 billion by 2030, growing at a CAGR of 15.9%.

Phase Change Materials (PCMs) play a significant role in promoting energy efficiency across diverse industries such as building construction, automotive systems, electronic devices, and sustainable energy solutions. Their distinctive capability to store and discharge heat during phase transitions allows for efficient temperature control, thereby aiding in minimizing energy usage and optimizing thermal performance.

Key Market Insights:

The increasing focus on sustainable construction and energy efficiency has driven the demand for advanced and innovative building materials. Consequently, phase change materials are being integrated into various applications, including electric underfloor heating systems, PCM-integrated glazing solutions, and thermally enhanced concrete.

One of the primary applications of PCM lies in enhancing thermal comfort within buildings. These materials help stabilize indoor temperatures by minimizing heat loss or gain through building envelopes. The expanding application of phase change materials in construction elements—such as wall panels, roofing systems, concrete mixtures, and thermally efficient polymers like polypropylene and polyolefin elastomers—is significantly contributing to the growth of the PCM market.

Phase Change Materials Drivers:

Rising Integration of Phase Change Materials in Construction to Drive Market Growth.

Phase Change Materials (PCMs) are incorporated into various components of residential infrastructure, including walls, floors, roofs, and other structural elements. In building systems, they are predominantly used in bulk applications such as wallboards or by integrating them directly into concrete or mortar matrices.

Among the different applications, modifying the thermal characteristics of passive building materials has emerged as one of the most significant uses of PCMs. A highly effective approach to enhancing the thermal energy storage capacity of construction materials involves the integration of PCMs. Building components such as wall panels, doors, roofing systems, and concrete are increasingly being combined with these materials to boost thermal performance. The most widely adopted method involves placing PCMs within the inner side of the building envelope, which enables the material to absorb and release heat within interior spaces as needed.

Wallboards and plasterboards serve as ideal substrates for embedding PCMs due to their cost-effectiveness and widespread use in managing indoor temperature fluctuations, particularly in lightweight building structures.

In certain applications, PCMs are embedded within the concrete layer beneath flooring systems. Additionally, PCM panels have been used as surface overlays to substitute conventional flooring. This integration is especially beneficial, as floors often represent a significant point of thermal energy loss due to heat conduction to the ground. By incorporating PCMs into floor structures, overall energy efficiency is markedly improved.

Phase Change Materials Restraints and Challenges:

Market growth is being hindered by technical challenges and the inherently corrosive properties of the product.

One of the key drawbacks of Phase Change Materials is their low thermal conductivity, alongside their high cost. Additionally, issues such as supercooling and phase separation contribute to thermal cycling degradation, ultimately reducing the overall lifespan of the material. These limitations may restrict the applicability of PCMs in construction environments that demand long-term durability. Poor thermal conductivity hampers the rate at which heat is transferred or absorbed within the building structure, which can negatively impact both occupant comfort and the system's overall performance.

Phase Change Materials Opportunities:

Rising Global Energy Demand Expected to Propel Market Expansion.

Global energy demand is rising at a significant pace, with the extensive reliance on fossil fuels contributing to elevated greenhouse gas emissions, particularly carbon dioxide (CO₂). These emissions are major drivers of adverse environmental effects, including ozone layer depletion, global warming, and climate change. The construction sector alone is responsible for over 30% of the world's total energy consumption and contributes to more than 30% of global CO₂ emissions, as reported by the International Energy Agency (IEA).

Shifting lifestyle preferences and increasing demand for thermal comfort in regions with variable climatic conditions are further accelerating energy consumption. Consequently, energy efficiency in buildings has become a central objective of energy policy across local, national, and global frameworks. In response, the manufacturing sector is focusing on the innovation of advanced building materials designed to optimize energy use within structures. In this context, Phase Change Materials (PCMs) are recognized as effective solutions to enhance energy efficiency and achieve substantial energy savings.

Phase Change Materials Segmentation:

By Type:

● Organic PCM

● Inorganic PCM

● Bio-Based PCM

Organic Phase Change Materials (PCMs), comprising both paraffin and non-paraffin types, currently represent the most recognized category within the PCM market. Non-paraffin PCMs are primarily derived from environmentally friendly and food-safe sources, such as vegetable oils. The bio-based PCM segment is expected to witness the highest growth rate, driven by the increasing demand for sustainable solutions. Fatty acids and fatty acid esters, which are renewable and eco-friendly, serve as bio-based PCMs. These materials are sourced from agro-food industry outputs and byproducts, including palm oil, palm kernel oil, soybean oil, and coconut oil—many of which are deemed safe for human consumption. As the industry moves toward environmentally responsible manufacturing, bio-based PCMs play a vital role in advancing sustainability, reducing environmental impact, and lowering carbon footprints across sectors.

In contrast, inorganic PCMs consist mainly of hydrated salt solutions formulated from synthetic natural water salts. These salts possess varying chemical compositions and are engineered to achieve specific phase change temperatures. To enhance their performance, salt hydrates are treated with specialized nucleating agents that help mitigate issues such as supercooling and phase separation during thermal cycling.

Globally, the buildings and construction sector leads the market for advanced phase change materials. These materials are increasingly critical in reducing energy consumption and supporting environmentally sustainable building practices. The rising demand for high-performance thermal insulation materials is largely driven by the implementation of stringent energy efficiency regulations, especially in developed economies. Moreover, the growing emphasis on sustainable construction practices has spurred the integration of advanced PCMs in a range of applications, including thermally optimized concrete, PCM-infused glass windows, and electric underfloor heating systems.

By Form:

● Encapsulated

● Non-Encapsulated

Encapsulated Phase Change Materials (PCMs) have maintained a leading position in the market due to their enhanced safety and reliability in various applications. Their encapsulation—either in micro or macro form—provides a protective barrier that prevents leakage and material degradation, thereby ensuring consistent performance over multiple thermal cycles.

This format is particularly preferred in sectors such as construction, textiles, electronics, and refrigeration, where attributes like hygiene, accurate temperature regulation, and ease of integration are critical. As industries increasingly seek compact and efficient thermal energy storage solutions, the demand for encapsulated PCMs is projected to continue rising through 2025, driven by growing interest from both industrial and consumer product manufacturers.

By Application:

● Building and Construction

● Textiles

● Cold Chain & Packaging

● Electronics

● Thermal Energy Storage

● Others

The Building & Construction sector has maintained a dominant position within the Phase Change Materials (PCM) market. This leadership is largely attributed to increasing demand for energy-efficient buildings and the enforcement of stricter building regulations designed to minimize energy consumption.

This passive thermal regulation significantly reduces reliance on active heating and cooling systems, leading to substantial energy cost savings. The adoption of this approach is projected to grow through 2025, as both residential and commercial developers prioritize sustainable construction practices that align with green certification criteria and offer long-term operational efficiencies.

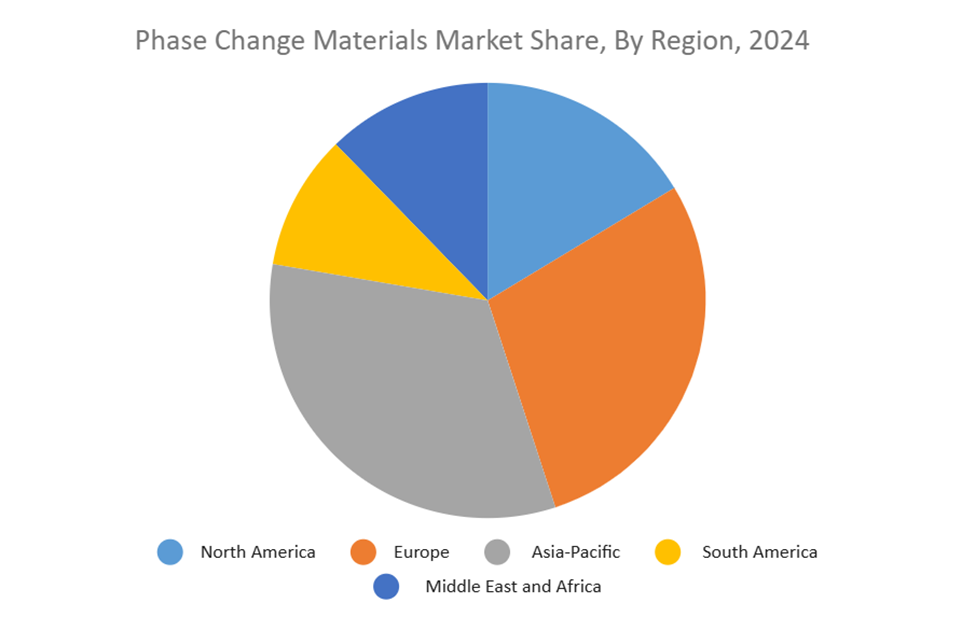

Phase Change Materials Segmentation- by region

● North America

● Europe

● Asia Pacific

● South America

● Middle East & Africa

Europe has established itself as the leading region in the Phase Change Materials (PCM) market, driven by its strong emphasis on energy efficiency, sustainability, and comprehensive regulatory frameworks targeting carbon emission reductions across key sectors such as construction, automotive, and cold chain logistics. European nations have been pioneers in adopting PCM technologies, particularly within green building initiatives where these materials are incorporated into insulation solutions to lower heating and cooling energy demands.

The European Union’s ambitious goal of achieving climate neutrality by 2050 under the European Green Deal has further accelerated the need for advanced energy storage and management technologies. Regional governments have implemented a variety of incentives and funding programs to encourage the integration of PCMs in both new construction and retrofit projects. For instance, Germany’s Energy Saving Ordinance (EnEV) enforces rigorous energy efficiency requirements, prompting builders to utilize materials like PCMs that enhance thermal regulation.

Meanwhile, the North American market is anticipated to experience significant growth, fueled by the increasing adoption of cutting-edge building technologies and rising demand for HVAC systems, particularly in the residential sector. The region’s colder climates necessitate efficient heating and cooling solutions, thereby driving the demand for advanced PCMs.

The Asia-Pacific region is projected to witness the highest growth during the forecast period, supported by expanding demand across diverse end-user industries including construction, packaging, textiles, electronics, and transportation. China, in particular, stands out as the largest packaging consumer globally, propelled by booming e-commerce and rising per capita incomes. Food packaging accounts for approximately 60% of China’s market share, making it a dominant segment within the broader packaging industry.

COVID-19 Pandemic: Impact Analysis

The Phase Change Materials (PCM) market experienced adverse effects as a result of the COVID-19 pandemic. Disruptions within the transportation sector and a temporary suspension of construction activities during pandemic-related lockdowns significantly impacted market growth.

Ongoing lockdown measures in various countries continue to challenge both the residential and commercial construction sectors by disrupting supply chains and logistics. Additionally, rising raw material costs, manufacturing facility closures, and a reduced labor workforce are key constraints likely to hinder overall market expansion.

Europe, recognized as a leading producer and consumer of both organic and inorganic PCMs, faced setbacks during the second wave of COVID-19, which led to a decline in construction projects across several countries. These challenges are anticipated to limit market growth in the coming years.

Latest Trends/ Developments:

In 2024, CCT advanced its product portfolio with the introduction of Koolit® Advanced PCM Gel, a flexible and leak-resistant gel pack designed to deliver consistent thermal protection for temperature-sensitive shipments.

Similarly, in 2024, Climator made further strides in the PCM industry by enhancing the performance and adaptability of its ClimSel™ product line, addressing the increasing demand for energy-efficient and sustainable solutions.

Key Players:

These are top 10 players in the Phase Change Materials :-

- Climator Sweden AB

- Croda International Plc

- Cold Chain Technologies

- Honeywell International Inc.

- Cryopak

- Outlast Technologies LLC

- Laird Technologies, Inc.

- Pluss Advanced Technologies Pvt. Ltd.

- PCM Products Ltd

- Rubitherm Technologies GmbH

Chapter 1. Global Phase Change Materials –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Phase Change Materials – Executive Summary

2.1. Market Size & Forecast – (2024 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Phase Change Materials – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Phase Change Materials Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Phase Change Materials - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Phase Change Materials – By Type

6.1. Introduction/Key Findings

6.2. Organic PCM

6.3. Inorganic PCM

6.4. Bio-Based PCM

6.8. Y-O-Y Growth trend Analysis By Type

6.9. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global Phase Change Materials – By Form

7.1. Introduction/Key Findings

7.2. Encapsulated

7.3. Non-Encapsulated

7.4. Y-O-Y Growth trend Analysis By Form

7.5. Absolute $ Opportunity Analysis By Form, 2024-2030

Chapter 8. Global Phase Change Materials – By Application

8.1. Introduction/Key Findings

8.2. Building and Construction

8.3. Textiles

8.4. Cold Chain & Packaging

8.5. Electronics

8.6. Thermal Energy Storage

8.7. Others

8.8. Y-O-Y Growth trend Analysis By Application

8.10. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 9. Global Phase Change Materials, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Type

9.1.3. By Form

9.1.4. By Application

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Type

9.2.3. By Form

9.2.4. By Application

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Type

9.3.3. By Form

9.3.4. By Application

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Type

9.4.3. By Form

9.4.4. By Application

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Type

9.5.3. By Form

9.5.4. By Application

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Phase Change Materials – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Climator Sweden AB

10.2. Croda International Plc

10.3. Cold Chain Technologies

10.4. Honeywell International Inc.

10.5. Cryopak

10.6. Outlast Technologies LLC

10.7. Laird Technologies, Inc.

10.8. Pluss Advanced Technologies Pvt. Ltd.

10.9. PCM Products Ltd

10.10. Rubitherm Technologies GmbH

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The increasing focus on sustainable construction and energy efficiency has driven the demand for advanced and innovative building materials.

The top players operating in the Phase Change Materials are - Climator Sweden AB, Croda International Plc and Cold Chain Technologies.

The Phase Change Materials (PCM) market experienced adverse effects as a result of the COVID-19 pandemic. Disruptions within the transportation sector and a temporary suspension of construction activities during pandemic-related lockdowns significantly impacted market growth.

What are the potential future trends and opportunities for the Phase Change Materials?

The Asia-Pacific is the fastest-growing region in the Phase Change Materials.