Natural Gas Storage Tanks Market Research Report – By Type (Above-ground Atmospheric Tanks, Pressurized Spherical Vessels, Bullet Tanks (Horizontal Pressure Vessels), Underground Storage Systems, Cryogenic LNG Storage Tanks, Floating Storage Units, Semi-refrigerated Storage), By Distribution Channel (Direct Equipment Manufacturers, Engineering, Procurement and Construction (EPC) Contractors, System Integrators, Specialized Storage Infrastructure Developers, Energy Infrastructure Investment Funds); By End User (Natural Gas Utilities, LNG Terminal Operators, Industrial Gas Consumers, Power Generation Facilities, Energy Trading Companies, Gas Transportation Sector, Municipal Gas Distributors); By Material (Carbon Steel, Stainless Steel, Nickel Alloys, Aluminum Alloys, Composite Materials, Concrete (for containment structures), Special Cryogenic Materials); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-7026

Format:

Region: Global

Natural Gas Storage Tanks Market Market Size (2025 – 2030)

The Natural Gas Storage Tanks Market was valued at USD 12.41 Billion in 2024 and is projected to reach a market size of USD 14.74 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 3.50%.

Market Size and Overview:

The natural gas storage tanks market stands at a pivotal juncture in 2024, characterized by evolving energy transition dynamics, supply security priorities, and technological innovation. These specialized containment systems, designed to safely store natural gas in various forms and conditions, constitute a critical component of the global energy infrastructure network. The market encompasses a diverse spectrum of storage solutions including pressurized vessels, cryogenic tanks for liquefied natural gas (LNG), underground facilities, and emerging modular options that cater to different capacity requirements, pressure specifications, and operational contexts from industrial applications to utility-scale energy management. Natural gas remains a cornerstone of the global energy mix despite accelerating decarbonization efforts, valued particularly for its lower carbon intensity compared to other fossil fuels and its role as a transitional energy source.

Key Market Insights:

Total global storage capacity now exceeds 13.2 trillion cubic feet, with approximately 385 major storage facilities operating worldwide. Steel remains the dominant construction material, accounting for 68% of fabricated tanks by volume, though composite and specialized alloy alternatives continue gaining market share due to their enhanced performance characteristics.

The average construction cost for large-scale LNG storage tanks has reached $220 million per unit, representing a 12% increase from previous year figures primarily due to material cost inflation and enhanced safety specifications.

Underground storage facilities, including depleted gas fields, aquifers, and salt caverns, comprise approximately 70% of total global capacity despite representing only 22% of total facilities by count.

The industry has witnessed 48 major new tank installations in 2024, predominantly concentrated in export terminals and receiving facilities designed to enhance energy security in import-dependent regions.

Cryogenic LNG storage tanks operating at temperatures around -162°C now account for 23% of new installations, reflecting the growing importance of the global LNG trade in natural gas markets.

Average tank construction timelines span 18-24 months from groundbreaking to commissioning, though regulatory approvals frequently extend overall project development cycles to 3-5 years.

Market Drivers:

Energy Security and Supply Resilience

Energy security concerns have emerged as a paramount driver for the natural gas storage tanks market in 2024, fundamentally reshaping investment patterns and strategic priorities across multiple regions. The vulnerability of just-in-time supply chains has been starkly exposed by recent geopolitical tensions, creating renewed appreciation for robust storage infrastructure that can buffer against supply disruptions. Import-dependent nations are particularly motivated to expand storage capacity, with many implementing mandatory minimum reserve requirements that directly translate to tank demand. The buffer function provided by adequate storage capacity enables greater negotiating leverage in supply contracts while mitigating price volatility during demand spikes or supply constraints. Beyond physical security, financial considerations also support expanded storage as it enables strategic purchasing during favourable price environments. The risk-mitigation value of storage has been increasingly quantified in investment models, supporting capital allocation even in regions previously reliant on continuous supply arrangements. This fundamental revaluation of energy security assumptions has accelerated approval processes for previously stalled projects and redirected government support toward critical infrastructure, including natural gas storage tanks.

LNG Market Expansion and Trade Flexibility

The dramatic expansion of global LNG trade volumes has created substantial demand for specialized cryogenic storage tanks at both export terminals and receiving facilities worldwide. Unlike pipeline-constrained natural gas, LNG enables truly global trade patterns that require sufficient storage capacity to manage loading schedules, shipping logistics, and regasification operations. The evolution toward greater contract flexibility, shorter delivery terms, and spot market transactions further increases storage requirements as buffer capacity becomes essential for optimizing trading opportunities. Modern LNG facilities typically allocate 35-45% of total project capital expenditure to storage infrastructure, reflecting its critical importance in the value chain. The growing trend toward smaller-scale and distributed LNG applications for transportation, industrial, and remote power generation applications has similarly expanded demand for appropriately sized storage solutions beyond traditional large terminal configurations. Floating storage and regasification units (FSRUs) represent a particularly dynamic market segment, offering faster deployment and location flexibility compared to conventional land-based terminals, though still requiring substantial storage capacity within their integrated designs. As LNG continues displacing pipeline gas in certain markets and opening entirely new consumption possibilities in others, the associated storage infrastructure represents a foundational enabler of this transformative market shift.

Market Restraints and Challenges:

The natural gas storage tanks market confronts several significant barriers to expansion despite favourable demand fundamentals. Capital intensity presents a primary challenge, with large-scale facilities requiring substantial upfront investment that can exceed $500 million, creating financing hurdles particularly in emerging markets with less developed capital infrastructure. Regulatory complexity has intensified with environmental review processes, safety requirements, and permitting procedures extending development timelines well beyond five years in many jurisdictions. Land availability constraints near demand centers complicate siting decisions, particularly for above-ground facilities with substantial footprints and mandatory safety buffer zones. Technical expertise limitations create bottlenecks in specialized engineering, fabrication, and construction capabilities required for these highly specialized containment systems. Long-term utilization uncertainty amid energy transition scenarios creates investment hesitation, with questions about potential stranded assets dampening enthusiasm despite current demand. Public acceptance challenges have intensified with local opposition frequently delaying or derailing proposed facilities based on safety concerns and environmental considerations. Supply chain vulnerabilities for specialized materials and components create schedule risks and cost volatility that complicate project economics and execution planning.

Market Opportunities:

The natural gas storage tanks market presents compelling opportunities driven by evolving energy system requirements and technological capabilities. Multi-purpose infrastructure designed for potential future repurposing represents a particularly promising segment, with systems engineered to accommodate hydrogen blending or eventual conversion to pure hydrogen storage enjoying premium valuations due to their extended asset life potential in decarbonization scenarios. Modular and scalable designs are gaining traction by offering phased capacity expansion possibilities that align capital deployment with actual demand development rather than speculative forecasts. Integration capabilities with renewable gas production, including biomethane and synthetic methane facilities, create differentiated value propositions as these alternative gas sources gain market share. Advanced materials applications, particularly in composite technologies, enable performance specifications previously unachievable with traditional materials while potentially reducing lifetime maintenance requirements. Digitalization presents opportunities throughout the value chain, from design optimization using computational fluid dynamics to operational enhancement through integrated monitoring platforms providing predictive maintenance capabilities and safety assurance. Specialized solutions for emerging applications in transportation, particularly marine and heavy road transport utilizing LNG or compressed natural gas, represent high-growth niches despite smaller individual project scales compared to utility infrastructure.

Market Segmentation:

Segmentation by Type:

• Above-ground Atmospheric Tanks

• Pressurized Spherical Vessels

• Bullet Tanks (Horizontal Pressure Vessels)

• Underground Storage Systems

• Cryogenic LNG Storage Tanks

• Floating Storage Units

• Semi-refrigerated Storage

Underground Storage Systems Underground storage systems dominate the market with 70% of global capacity, leveraging geological formations including depleted gas fields, aquifers, and salt caverns to create massive storage volumes at relatively favourable economics. These systems offer unparalleled capacity-to-surface-footprint ratios, enhancing their feasibility near population centers where land constraints would otherwise prohibit large-scale storage.

Cryogenic LNG Storage Tanks Cryogenic LNG storage tanks represent the fastest-growing segment with 31% annual expansion, supporting the rapidly evolving global LNG trade that requires specialized containment at approximately -162°C. These sophisticated double-walled structures utilize advanced insulation systems including perlite, vacuum spaces, and multi-layer technologies to maintain extreme low temperatures while minimizing boil-off gas.

Segmentation by Distribution Channel:

• Direct Equipment Manufacturers

• Engineering, Procurement and Construction (EPC) Contractors

• System Integrators

• Specialized Storage Infrastructure Developers

• Energy Infrastructure Investment Funds

Engineering, Procurement and Construction (EPC) Contractors EPC contractors dominate the market distribution landscape with 58% share, leveraging their comprehensive project execution capabilities spanning design, procurement, construction, and commissioning for these complex infrastructure assets. These organizations typically maintain long-standing relationships with utilities, energy majors, and governments, positioning them as preferred channels for large-scale storage projects requiring extensive coordination across multiple disciplines and stakeholders.

Energy Infrastructure Investment Funds Energy infrastructure investment funds represent the fastest-growing distribution channel at 43% annual growth, transforming the market through innovative financing models that separate infrastructure ownership from operational responsibilities. These specialized investment vehicles, typically structured to generate stable long-term returns for institutional investors, have identified natural gas storage assets as attractive portfolio additions due to their essential role in energy systems and relatively predictable cash flows.

Segmentation by End-User:

• Natural Gas Utilities

• LNG Terminal Operators

• Industrial Gas Consumers

• Power Generation Facilities

• Energy Trading Companies

• Gas Transportation Sector

• Municipal Gas Distributors

Natural Gas Utilities Natural gas utilities represent the dominant end-user segment commanding 39% market share, operating storage infrastructure as core assets supporting their fundamental service obligations to maintain continuous supply regardless of consumption variability. These organizations leverage storage to manage seasonal demand fluctuations, optimize purchasing strategies across price environments, and provide essential reliability during peak demand periods or supply disruptions.

Gas Transportation Sector The gas transportation sector emerges as the fastest-growing end-user segment with 38% annual expansion, driven by accelerating adoption of natural gas as a lower-emission alternative to diesel and heavy fuel oil in shipping, trucking, and rail applications. This segment requires specialized storage infrastructure at fueling locations, distribution hubs, and bunkering facilities, typically utilizing medium-scale pressurized or cryogenic systems rather than utility-scale facilities.

Segmentation by Material:

• Carbon Steel

• Stainless Steel

• Nickel Alloys

• Aluminum Alloys

• Composite Materials

• Concrete (for containment structures)

• Special Cryogenic Materials

Carbon Steel Carbon steel dominates the market with 68% share by volume, delivering the optimal combination of strength, fabrication compatibility, cost efficiency, and established performance history for most storage applications. Modern high-strength low-alloy variants enable reduced wall thicknesses while maintaining pressure ratings, progressively improving the economics of steel storage solutions. Advanced coating systems and cathodic protection have significantly extended service lifespans by addressing traditional corrosion vulnerabilities, particularly for buried and subsea applications.

Composite Materials Composite materials represent the fastest-growing segment with 47% annual expansion, offering breakthrough performance capabilities through engineered combinations of fiber reinforcement within specialized polymer matrices. These advanced materials deliver exceptional strength-to-weight ratios, corrosion resistance, and design flexibility that enable novel tank configurations previously unachievable with traditional materials.

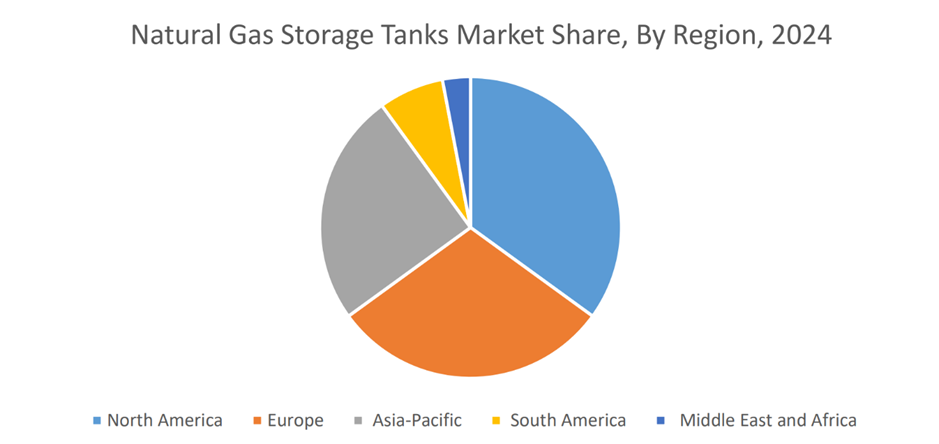

Segmentation by Regional Analysis:

• North America

• Europe

• Asia Pacific

• South America

• Middle East and Africa

North America dominates the natural gas storage tank market with 32% global share, leveraging its extensive production capacity, sophisticated distribution infrastructure, and favourable underground storage geology. The region's massive salt dome formations along the Gulf Coast provide ideal conditions for developing high-deliverability storage assets that support both domestic flexibility and export operations. Regulatory frameworks in both the United States and Canada have historically supported storage infrastructure development through various market mechanisms that appropriately value flexibility services

Asia-Pacific region represents the fastest-growing market for natural gas storage tanks with 37% annual expansion, driven by massive investments in LNG import infrastructure serving rapidly expanding consumption centers. China leads regional development with its strategic shift toward natural gas in urban environments to address air quality concerns, supporting over 40 major storage projects currently under construction. Limited suitable geology for underground storage in many Asia-Pacific countries necessitates greater reliance on above-ground tank systems, particularly cryogenic LNG storage associated with import terminals.

COVID-19 Impact Analysis:

The natural gas storage tanks market experienced significant disruption during the COVID-19 pandemic, though effects varied substantially across regions and market segments. Construction delays impacted approximately 65% of ongoing projects as workforce restrictions, supply chain disruptions, and financing uncertainties forced schedule revisions averaging 8-14 months. Equipment manufacturing faced similar challenges with specialized component lead times extending by 30-40%, particularly for cryogenic systems requiring precision fabrication under controlled conditions. The pandemic-induced economic contraction temporarily reduced global gas demand, with industrial consumption particularly affected, leading to historically high storage inventory levels that paradoxically demonstrated the value of adequate storage capacity during market disruptions. Financial uncertainty prompted reassessment of numerous proposed projects, with approximately 22% of pre-FID (Final Investment Decision) developments postponed beyond original timelines as sponsors adopted more conservative capital allocation approaches. The most resilient market segment proved to be security-oriented storage investments in import-dependent regions, which continued advancing despite broader market uncertainties due to their strategic rather than purely commercial justification. Recovery patterns have emerged asymmetrically, with projects supporting export infrastructure and energy security objectives resuming more rapidly than those primarily serving anticipated demand growth or optimization objectives.

Latest Trends and Developments:

The natural gas storage tank market is experiencing transformative technological and strategic developments that are reshaping industry approaches and capabilities. Advanced materials engineering has enabled breakthrough designs including carbon fiber reinforced polymer tanks offering unprecedented strength-to-weight ratios for high-pressure applications, while graphene-enhanced coatings are extending corrosion protection for conventional steel vessels. Modularization has accelerated with factory-built standardized units reducing on-site construction requirements by up to 60% while improving quality control and shortening project timelines from groundbreaking to commissioning. Digitalization has transformed operational capabilities through comprehensive instrumentation packages enabling real-time monitoring of structural integrity, content conditions, and environmental parameters with predictive analytics identifying maintenance requirements before physical manifestation of issues. Multifunctional design approaches are gaining prominence, with new facilities incorporating hydrogen compatibility from initial construction to accommodate potential future energy carrier transitions without requiring complete infrastructure replacement. Integration with renewable gas production including biomethane and power-to-gas hydrogen facilities represents an emerging hybrid approach creating flexibility within evolving energy systems. Floating storage concepts continue advancing beyond traditional LNG applications to include various compressed gas alternatives, particularly serving island nations and coastal population centers where land constraints or geological limitations prevent conventional storage development.

Key Players in the Market:

• McDermott International

• Chart Industries

• Linde Engineering

• Air Products

• Tokyo Gas Engineering Solutions

• Wartsila

• Vopak

• TGE Gas Engineering

• IHI Corporation

• JGC Holdings

Chapter 1. Natural Gas Storage Tanks Market – Scope & Methodology

1.1 Market Segmentation

1.2 Assumptions

1.3 Research Methodology

1.4 Primary Sour

1.5 Secondary Sources

Chapter 2. Natural Gas Storage Tanks Market – Executive Summary

2.1 Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2 Key Trends & Insights

2.3 COVID-19 Impact Analysis

2.3.1 Impact during 2023 – 2030

2.3.2 Impact on Supply – Demand

Chapter 3. Natural Gas Storage Tanks Market – Competition Scenario

3.1 Market Share Analysis

3.2 Product Benchmarking

3.3 Competitive Strategy & Development Scenario

3.4 Competitive Pricing Analysis

3.5 Supplier - Distributor Analysis

Chapter 4. Natural Gas Storage Tanks Market - Entry Scenario

4.1 Case Studies – Start-up/Thriving Companies

4.2 Regulatory Scenario - By Region

4.3 Customer Analysis

4.4 Porter's Five Force Model

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Powers of Customers

4.4.3 Threat of New Entrants

4.4.4 .Rivalry among Existing Players

4.4.5 Threat of Substitutes

Chapter 5.Natural Gas Storage Tanks Market - Landscape

5.1 Value Chain Analysis – Key Stakeholders Impact Analysis

5.2 Market Drivers

5.3 Market Restraints/Challenges

5.4 Market Opportunities

Chapter 6. Natural Gas Storage Tanks Market - By Type

6.1 Above Ground

6.2 Under Ground

Chapter 7. Natural Gas Storage Tanks Market - By Storage Type

7.1 Depleted Gas Reservoir

7.2 Salt Cavern

7.3 Aquifer Reservoir

Chapter 8. Natural Gas Storage Tanks Market – By Region

8.1 North America

8.2 Europe

8.3 Asia-Pacific

8.4 Latin America

8.5 The Middle East

8.6 Africa

Chapter 9. Natural Gas Storage Tanks Market - Company Profiles – (Overview, Product Portfolio, Financials, Developments)

9.1 Company 1

9.2 Company 2

9.3 Company 3

9.4 Company 4

9.5 Company 5

9.6 Company 6

9.7 Company 7

9.8 Company 8

9.9 Company 9

9.10 Company 10

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The natural gas storage tanks market is primarily driven by growing energy security concerns amid geopolitical uncertainties and supply disruptions. The expanding global LNG trade requires specialized storage infrastructure at both export and import terminals.

The natural gas storage tanks market faces significant challenges including extremely high capital costs creating financing barriers for new projects. Complex regulatory approval processes extend development timelines and increase uncertainty.

Major players include McDermott International, Chart Industries, Linde Engineering, Air Products, Tokyo Gas Engineering Solutions, Wartsila, Vopak, TGE Gas Engineering, IHI Corporation, JGC Holdings, CB&I (a subsidiary of McDermott), Enbridge, Kinder Morgan, TransCanada, and Chevron Phillips Chemical.

North America currently holds the largest market share, estimated at around 32%.

Asia Pacific has shown significant room for growth in specific segments.