Lithium-Ion-Battery Market Research Report -- Segmentation by Type (Lithium Cobalt Oxide, Lithium Iron Phosphate, Lithium Nickel Manganese Cobalt, Others); By Application (Consumer Electronics, Automotive, Energy Storage Systems, Industrial, Others); By Capacity (0-3000mAh, 3000-10000mAh, 10000-60000mAh, Above 60000mAh); By End-User (Automotive, Consumer Electronics, Grid Storage, Industrial, Others); Region - Forecast (2025 - 2030)

Published: 2024 - January

Report Code: IM-7218

Format:

Region: Global

Market Size and Overview:

The Lithium-Ion Battery Market was valued at USD 54.87 billion in 2024 and is projected to reach a market size of USD 116.24 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.2%.

Lithium-Ion Battery technology has revolutionized energy storage across multiple industries since its commercial introduction in the early 1990s. This advanced electrochemical energy storage solution has become the cornerstone of modern portable electronics, electric vehicles, and renewable energy systems. With the accelerating global transition toward sustainable energy solutions and the exponential growth in electric vehicle adoption, lithium-ion batteries have emerged as a critical enabling technology for the decarbonization of transportation and energy sectors. The continuous advancement in battery chemistry, manufacturing processes, and cost reduction initiatives has made lithium-ion technology increasingly accessible across diverse applications, from consumer electronics to grid-scale energy storage systems.

Key Market Insights:

According to the International Energy Agency (IEA), electric vehicle sales reached 10.5 million units globally in 2022, representing a 55% increase from the previous year, with lithium-ion batteries powering over 95% of these vehicles. This surge in EV adoption directly correlates with battery demand, as automotive applications now account for approximately 64% of total lithium-ion battery consumption, compared to just 23% in 2015.

A comprehensive industry survey conducted by BloombergNEF revealed that lithium-ion battery pack prices have declined by 89% since 2010, falling from $1,191 per kWh to $132 per kWh in 2022. This dramatic cost reduction has been a primary catalyst for widespread adoption, with industry analysts projecting prices to reach $90 per kWh by 2025, marking the critical threshold for electric vehicle cost parity with internal combustion engine vehicles.

Research from Wood Mackenzie indicates that global battery manufacturing capacity reached 1.1 TWh in 2022, with an additional 2.4 TWh of capacity under construction or planned through 2025. China dominates this manufacturing landscape, controlling approximately 77% of global production capacity, while the United States and Europe are rapidly expanding their domestic manufacturing capabilities to reduce supply chain dependencies and support regional EV market growth.

Lithium-Ion Battery Market Drivers:

The global transition toward electric mobility and the implementation of stringent environmental regulations are fundamentally reshaping the automotive industry and driving unprecedented demand for Lithium-Ion-Battery technology.

The automotive sector's transformation represents the most significant growth driver for the Lithium-Ion-Battery market, with governments worldwide implementing ambitious targets for electric vehicle adoption and internal combustion engine phase-outs. The European Union has mandated that all new passenger cars sold after 2035 must be zero-emission vehicles, while China, the world's largest automotive market, requires that new energy vehicles represent 40% of total sales by 2030. These regulatory frameworks have compelled automakers to accelerate their electric vehicle development programs and secure substantial battery supply contracts. Major automotive manufacturers have committed over $330 billion in electric vehicle investments through 2030, with companies like Volkswagen, General Motors, and Ford planning to transition their entire passenger vehicle portfolios to electric powertrains within the next decade. The competitive landscape has intensified as traditional automakers compete with electric vehicle specialists like Tesla, BYD, and emerging players such as Rivian and Lucid Motors. This competition has driven continuous innovation in battery technology, with manufacturers pursuing improvements in energy density, charging speed, and thermal management to differentiate their products.

The accelerating deployment of renewable energy systems and the growing need for grid-scale energy storage solutions are creating substantial demand for Lithium-Ion-Battery technology in stationary applications.

The intermittent nature of renewable energy sources such as solar and wind power requires sophisticated energy storage systems to ensure grid stability and enable higher penetration of clean energy technologies. Lithium ion batteries have emerged as the preferred technology for grid-scale energy storage due to their high round-trip efficiency, rapid response times, and declining costs. The increasing frequency of extreme weather events and aging grid infrastructure have highlighted the importance of energy resilience, driving investments in distributed energy storage systems that can provide backup power during outages while optimizing energy costs through peak shaving and load shifting applications. Commercial and industrial customers are increasingly adopting behind-the-meter energy storage solutions to reduce demand charges and participate in grid services programs, creating a rapidly expanding market segment for lithium ion batteries.

Lithium-Ion-Battery Market Restraints and Challenges:

The Lithium-Ion-Battery market faces significant challenges related to raw material supply chain constraints and geopolitical risks associated with critical mineral dependencies. Lithium, cobalt, and nickel prices have experienced extreme volatility, with lithium carbonate prices increasing by over 400% between 2020 and 2022 before moderating. The concentration of lithium production in South America and Australia, combined with cobalt mining primarily in the Democratic Republic of Congo, creates supply chain vulnerabilities that could impact battery production and pricing. Additionally, the environmental and social impacts of mining operations have raised sustainability concerns among consumers and regulatory bodies. Technical challenges persist in battery safety, particularly regarding thermal runaway risks and the need for sophisticated battery management systems to prevent fires and explosions.

Lithium-Ion-Battery Market Opportunities:

The Lithium-Ion-Battery market presents substantial growth opportunities across emerging applications and geographic regions as technology costs continue to decline and performance characteristics improve. The electrification of commercial vehicles, including delivery trucks, buses, and heavy-duty transport, represents a significant untapped market with unique requirements for high-capacity, fast-charging battery systems. Marine and aviation electrification initiatives are creating new market segments, with companies developing specialized battery solutions for electric boats, ships, and aircraft that require exceptional energy density and safety characteristics. The integration of artificial intelligence and advanced battery management systems creates opportunities for enhanced performance optimization, predictive maintenance, and extended battery life through intelligent charging and usage patterns. Emerging markets in Southeast Asia, Africa, and Latin America present substantial growth potential as economic development drives increased adoption of electric vehicles and renewable energy systems.

Lithium-Ion-Battery Market Segmentation:

Market Segmentation: By Type

• Lithium Cobalt Oxide (LCO)

• Lithium Iron Phosphate (LFP)

• Lithium Nickel Manganese Cobalt (NMC)

• Others

In 2024, the Lithium Nickel Manganese Cobalt (NMC) segment dominated the global Lithium-Ion-Battery market with approximately 47.3% revenue share. This dominance is attributed to NMC's superior energy density characteristics, making it ideal for automotive applications where range and weight are critical factors. The balanced combination of nickel, manganese, and cobalt provides excellent performance characteristics including high energy density, good thermal stability, and extended cycle life, making NMC the preferred choice for premium electric vehicles and energy storage systems.

The Lithium Iron Phosphate (LFP) segment is projected to experience the highest growth rate during the forecast period, with a CAGR of 21.7%. This accelerated growth is driven by LFP's superior safety characteristics, longer cycle life, and significantly lower cost compared to cobalt-containing chemistries. The segment has gained particular traction in China and is expanding globally as automakers seek cost-effective solutions for mass-market electric vehicles and stationary energy storage applications where energy density requirements are less stringent than premium automotive applications.

Market Segmentation: By Application

• Consumer Electronics

• Automotive

• Energy Storage Systems

• Others

The automotive segment accounted for the largest market share of approximately 64.2% in 2024, reflecting the rapid growth in electric vehicle adoption and the high battery content per vehicle compared to other applications. Electric vehicles typically require battery packs ranging from 40-100 kWh, significantly larger than consumer electronics applications, driving higher revenue per unit and overall market value. The segment's dominance is expected to continue as automotive manufacturers accelerate their electrification strategies and expand their electric vehicle portfolios across all vehicle categories.

Energy Storage Systems represent the fastest-growing application segment with a projected CAGR of 24.8% during the forecast period. This growth is driven by increasing renewable energy installations, grid modernization initiatives, and the growing demand for backup power solutions in both residential and commercial applications.

Market Segmentation: By Capacity

• 0-3000mAh

• 3000-10000mAh

• 10000-60000mAh

• Above 60000mAh

The Above 60000mAh segment dominated the market with approximately 52.7% revenue share in 2024, primarily driven by automotive applications that require large-capacity battery packs for electric vehicles. This segment includes automotive battery modules and packs, grid-scale energy storage systems, and industrial applications requiring substantial energy storage capacity. The high capacity requirements and corresponding high unit values make this segment the largest revenue contributor despite representing fewer individual battery units compared to smaller capacity segments.

The 10000-60000mAh segment is projected to grow at the fastest CAGR of 18.9% during the forecast period. This growth is attributed to the expanding market for electric motorcycles, e-bikes, power tools, and medium-scale energy storage applications that require mid-range capacity batteries. The segment benefits from the proliferation of electric two-wheelers in emerging markets and the growing adoption of cordless power tools in professional and consumer applications.

Market Segmentation: By End-User

• Automotive

• Consumer Electronics

• Grid Storage

• Industrial

• Others

The automotive end-user segment maintained the largest market share of 64.8% in 2024, driven by the accelerating transition to electric mobility across passenger cars, commercial vehicles, and two-wheelers. This segment's dominance reflects the high-value nature of automotive battery applications and the substantial battery capacity requirements for electric vehicles. The segment is expected to maintain its leadership position as automotive electrification accelerates globally and battery costs continue to decline.

Consumer Electronics represents a mature but stable market segment, with steady demand driven by smartphones, laptops, tablets, and wearable devices. While unit volumes remain high, the segment's revenue growth is limited by the relatively small battery capacity requirements and intense price competition. However, the segment continues to drive innovation in battery energy density and charging speed to meet consumer demands for longer battery life and faster charging capabilities.

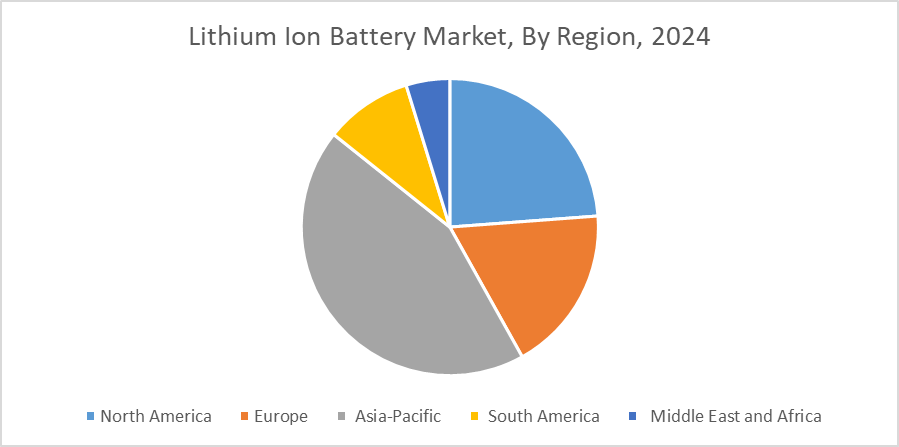

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

Asia-Pacific dominated the global Lithium-Ion-Battery market in 2024, accounting for approximately 67.4% of the total market share. This dominance is primarily attributed to China's position as the world's largest battery manufacturer and electric vehicle market, with companies like CATL, BYD, and Gotion High-Tech leading global production capacity. The region also benefits from established supply chains for raw materials and components, lower manufacturing costs, and supportive government policies promoting electric vehicle adoption and renewable energy deployment.

Europe is projected to witness the highest growth rate during the forecast period, with a CAGR of 19.3%. This accelerated growth is driven by aggressive electric vehicle adoption targets, substantial investments in domestic battery manufacturing capacity, and stringent environmental regulations promoting clean energy transitions. The European Union's Green Deal and the establishment of the European Battery Alliance have created a supportive policy environment for battery technology development and manufacturing, attracting significant investments from both domestic and international companies.

COVID-19 Impact Analysis on the Global Lithium-Ion-Battery Market:

The COVID-19 pandemic initially disrupted Lithium-Ion-Battery supply chains due to factory shutdowns and raw material supply constraints, particularly affecting production in China during the first quarter of 2020. However, the pandemic ultimately accelerated the market's growth trajectory as governments worldwide implemented economic stimulus packages that included substantial investments in electric vehicle infrastructure and clean energy technologies. The crisis highlighted the strategic importance of domestic battery manufacturing capabilities, leading to increased investments in regional production facilities and supply chain localization initiatives.

The pandemic also accelerated the adoption of electric vehicles in many markets as consumers became more environmentally conscious and governments implemented policies promoting clean transportation solutions. Additionally, the increased focus on energy resilience and backup power solutions during the pandemic drove demand for residential and commercial energy storage systems. The shift toward remote work and increased reliance on electronic devices sustained demand for consumer electronics batteries, while the acceleration of e-commerce and last-mile delivery services created new opportunities for electric commercial vehicles and their associated battery systems. These pandemic-induced changes in consumer behavior and government priorities are expected to have lasting positive impacts on Lithium-Ion-Battery demand across multiple application segments.

Latest Trends/ Developments:

The development of silicon nanowire anodes and solid-state electrolytes represents a significant technological breakthrough that could increase energy density by 40-50% while improving safety characteristics. Major manufacturers including Samsung SDI, QuantumScape, and Solid Power are advancing toward commercial production of solid-state batteries, with initial deployments expected in premium automotive applications by 2025-2026.

Battery recycling and circular economy initiatives are gaining momentum as the industry addresses sustainability concerns and raw material supply constraints. Companies like Redwood Materials and Li-Cycle are developing advanced recycling technologies that can recover over 95% of critical materials from end-of-life batteries, creating closed-loop supply chains that reduce dependence on virgin raw materials.

Key Players:

• Contemporary Amperex Technology (CATL)

• BYD Company Limited

• LG Energy Solution

• Panasonic Corporation

• Samsung SDI

• Tesla, Inc.

• SK Innovation

• Gotion High-Tech

• CALB (China Aviation Lithium Battery)

• EVE Energy

Chapter 1. Lithium-Ion-Battery Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Lithium-Ion-Battery Market – Executive Summary

2.1. Market Capacity & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Lithium-Ion-Battery Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Lithium-Ion-Battery Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Lithium-Ion-Battery Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Lithium-Ion-Battery Market – By Type

6.1. Introduction/Key Findings

6.2. Lithium Cobalt Oxide

6.3. Lithium Iron Phosphate

6.4. Lithium Nickle Manganese Cobalt

6.4. Y-O-Y Growth trend Analysis By Type

6.5. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Lithium-Ion-Battery Market – By Application

7.1. Introduction/Key Findings

7.2. Consumer Electronics

7.3. Automotive

7.4. Energy Storage Systems

7.5. Industrial

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Lithium-Ion-Battery Market – By Capacity

8.1. Introduction/Key Findings

8.2. 0-3000mAh

8.3. 3000-10000mAh

8.4. 10000-60000mAh

8.5. Above 60000mAh

8.6. Y-O-Y Growth trend Analysis By Capacity

8.7. Absolute $ Opportunity Analysis By Capacity, 2025-2030

Chapter 9. Lithium-Ion-Battery Market – By End User

9.1. Introduction/Key Findings

9.2. Automotive

9.3. Consumer Electronics

9.4. Grid Storage

9.5. Industrial

9.6. Others

9.7. Y-O-Y Growth trend Analysis By End User

9.8. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 10. Lithium-Ion-Battery Market, By Geography – Market Capacity, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Application

10.1.4. By Capacity

10.1.5. By End User

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Application

10.2.4. By Capacity

10.2.5. By End User

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Application

10.3.4. By Capacity

10.3.5. By End User

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Application

10.4.4. By Capacity

10.4.5. By End User

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Application

10.5.4. By Capacity

10.5.5. By End User

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Lithium-Ion Battery Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Contemporary Amperex Technology (CATL)

11.2. BYD Company Limited

11.3. LG Energy Solution

11.4. Panasonic Corporation

11.5. Samsung SDI

11.6. Tesla, Inc.

11.7. SK Innovation

11.8. Gotion High-Tech

11.9. CALB (China Aviation Lithium Battery)

11.10. EVE Energy

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Lithium-Ion Battery Market was valued at USD 54.87 billion in 2024 and is projected to reach a market size of USD 116.24 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.2%.

The global transition toward electric mobility and the implementation of stringent environmental regulations are the primary drivers propelling the global Lithium-Ion-Battery market.

Based on Type, the Global Lithium-Ion Battery Market is segmented into Lithium Cobalt Oxide, Lithium Iron Phosphate, Lithium Nickel Manganese Cobalt, Lithium Manganese Oxide, Lithium Titanate, and Others.

Asia-Pacific is the most dominant region for the Global Lithium-Ion-Battery Market.

Contemporary Amperex Technology (CATL), BYD Company Limited, LG Energy Solution, and Panasonic Corporation are the key players operating in the Global Lithium-Ion-Battery Market.