Global LED Driver Market Research Report – Segmentation By Luminaire Type (Reflectors, Type A Lamp, Panel Lights, Decorative Lamps, Others), By Application (General Lighting, Automotive Lighting, Backlighting), By Component (Driver IC, Discrete Component), By Supply Type (Constant Current, Constant Voltage), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-1614

Format:

Region: Global

Market Size and Overview:

The Global LED Driver Market was valued at USD 20.19 billion in 2024 and is projected to reach a market size of USD 56.63 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.91%.

Fast acceptance of energy-efficient LED lighting in the residential, commercial, industrial, and automotive industries drives this expansion. Stringent energy-efficiency requirements, increased demand for smart lighting controls, and the move toward electrified mobility and display backlight applications are all advantages drivers—essential for controlling current and voltage to LEDs.

Key Market Insights:

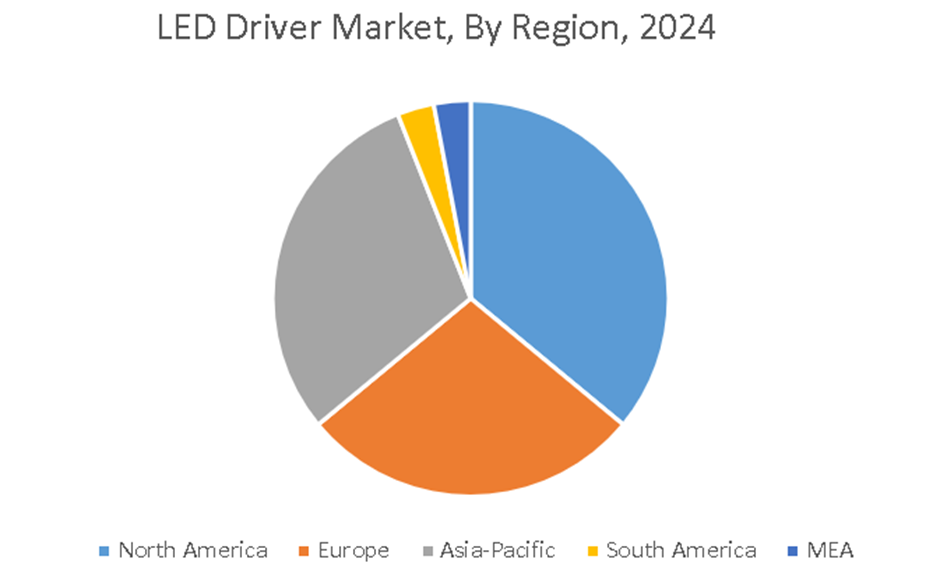

Driven by extensive infrastructure projects in China and India and strong LED retrofitting campaigns, Asia Pacific represented more than 42% of the world's income.

With nearly 42%, driver ICs had the most part share as integration into small, high-efficiency modules is more desirable than discrete solutions.

Driven by commercial and industrial retrofit projects all around, general lighting accounted for 55% of the demand for LED drivers.

Reflecting growing do-it-yourself retrofits and renovations of already installed lights, the aftermarket distribution sector saw a 10. 2% growth rate.

LED Driver Market Drivers:

The latest rules and regulations regarding energy efficiency are considered to drive the growth of this market.

Notably, under the EU’s Ecodesign Regulation for light sources and separate control gears (EU 2019/2020), which came into full effect in September 2021, governments worldwide are phasing out wasteful lights and demanding LED adoption. This rule pushes producers to maximize power factor, efficiency (> 85–90%), and standby losses by requiring all LED drivers sold in the EU to satisfy minimal performance requirements. Effective July 2024, the updated Ecodesign for Sustainable Products Regulation (ESPR) also expands criteria to cover lighting items' digital product passports as well as repairability and durability. According to the European Commission, these regulations taken together have already produced over €120 billion in energy‑bill savings and a ten percent yearly consumption drop for covered items. To comply, LED‑driver vendors are investing in advanced topologies (e.g., synchronous rectification, GaN switches) that maximize lumen output per watt while ensuring long‐term reliability and ease of maintenance.

The integration of IoT with smart lighting is a major market growth driver, bringing in innovation.

Accelerating demand for programmable, dimmable LED drivers capable of following protocols like DALI‑2, Zigbee, and Bluetooth Mesh is the convergence of IoT and lighting controls. Replacing conventional on/off systems with networked dimming and daylight harvesting can help wireless lighting controls save up to 60% of the energy used in commercial buildings. The Bluetooth SIG and DALI Alliance issued the Bluetooth Mesh‑to‑DALI Gateway Specification in May 2020, allowing D4i‑certified luminaires to seamlessly connect with building‑management systems and Bluetooth Mesh networks. Moreover, yearly shipments of Bluetooth-enabled commercial lighting solutions are increasing at a 130% CAGR by 2026, reflecting fast adoption in workplaces, retail locations, and warehouses. These integrated drivers help fine‑grain dimming, firmware updates, and remote diagnosis, therefore establishing lighting as a fundamental component of smart-building energy management.

The shift towards automotive electrification is a major market growth driver.

The switch to electric cars is fueling demand for high-reliability LED drivers in automobile applications: adaptive headlights, ambient cabin illumination, and digital dashboards. According to The Business Research Company, the automotive LED-driver market grew from USD 9.98 billion in 2024 to an expected USD 27. 99 billion by 2029, at a 22 22%. 8% CAGR. Growth is supported by tougher vehicle-lighting regulations (e.g., UNECE R148 adaptive-beam directives), the growth of ADAS systems needing accurate light patterns, and OEM sustainability goals favoring energy-efficient LEDs. Automotive drivers must meet demanding standards for vibration resistance, temperature extremes (–40 °C to +125 °C), and EMI/EMC compliance.

The latest display backlighting trends are driving the development of this market.

The popularity of mini-LED backlights in televisions, monitors, and mobile devices has exploded, therefore calling for accurate, low-ripple constant-current drivers to guarantee even brightness and a wide dynamic range. By dynamically dimming thousands of zones, mini-LED backlit LCDs improve HDR performance and perceived image quality to generate contrast ratios of over 10,000:1, over 100 times that of conventional LED backlights. Through fine-grain local dimming and improved driving strategies, these systems also provide 20–30% energy savings, therefore lowering power draw without sacrificing peak brightness. Driver ICs for mini‑LED arrays include passive‑matrix (PM) or active‑matrix (AM) dimming schemes, therefore reconciling complexity, cost, and resolution. As consumer desire for thinner, brighter displays rises, backlight-driver creativity, such as multi-channel constant-current topologies and embedded thermal-management components, will be essential for next-generation display experiences.

LED Driver Market Restraints and Challenges:

The market faces challenges due to constraints related to the supply of the components.

Direct effects of continuing worldwide semiconductor shortages have on LED driver IC availability; lead times have stretched to 12 to 18 weeks, and pricing has increased by 5 to 10% year over year. Particularly vulnerable has been the lighting industry: by late 2020, 11% of U. S. contractors reported electrical product shortages, including LED drivers, and several significant companies announced price hikes of 2–9% to help cover increased components and logistics expenses. Geopolitically sensitive nodes are still constrained even though inventories for non‑AI sectors are normalizing, which causes rolling shortages that might derail project schedules. These limitations cause lighting‑OEMs to lock long‑term supplier contracts, keep higher safety stocks, and occasionally restructure goods around available ICs, therefore increasing working capital demands and slowing new product introductions.

The existence of complexity in its design is a major drawback for this market.

Including sophisticated capabilities, dimming, color tuning, tunable white spectra, and remote diagnostics into LED drivers greatly increases design complexity and R&D costs. Modern drivers need to support several protocols (DALI‑2, NFC, Bluetooth Mesh) and incorporate firmware‑updatable microcontrollers, therefore extending development cycles beyond 12–18 months for fully validated products. High‑precision analog front ends, digital signal processors, and EMI/EMC filters add complexity to design challenges, frequently requiring many PCB revisions and costly compliance testing. Smaller companies battle to amortize these expenditures over low order volumes, hence favoring major, vertically integrated companies that can absorb design and certification costs.

The requirement of thermal management is a big challenge that is being faced by the market.

High‑power LED drivers generate a lot of heat naturally; hence, strong thermal‑management solutions are needed; these raise enclosure size and cost while complicating compact luminaire designs. In industrial applications, a 50 W driver can dissipate 5–10 W of losses, necessitating heat sinks, thermal interface materials, or perhaps active cooling. Designers must carefully balance thermal routes and air‑flow channels in closely enclosed fixtures, such as downlights or street‑light heads, often sacrificing driver placement or lumen output to keep safe junction temperatures and long‑term reliability. These thermal components not only increase weight and bill‑of‑materials but also impose mechanical constraints limiting miniaturization and aesthetic flexibility.

The existence of price sensitivity, especially in the emerging markets, negatively affects the market.

While LED pricing has decreased steadily, end consumers in cost‑sensitive countries, Southeast Asia, Latin America, and some parts of Africa, still prefer simple, low‑feature drivers costing under USD 3 /unit. Premium modules with sophisticated dimming or IoT features, which can cost 2–3 times more, see limited uptake outside government or big corporate initiatives. Local lighting OEMs and distributors frequently operate on incredibly small margins, so volume takes precedence over added capability, therefore suppressing profitability for feature-rich driver makers. Many international vendors, therefore, create region-specific product lines with stripped-down feature sets to meet price objectives; however, this segmentation lowers the total average selling price and impedes the spread of smart-lighting innovations in these areas.

LED Driver Market Opportunities:

The latest emergence of GaN and SiC power electronics is said to shape the future of the market.

Combining Gallium Nitride (GaN) and Silicon Carbide (SiC) in LED-driver circuits is generating next-generation performance jumps. Compared to silicon counterparts, GaN devices enable switching frequencies over 500 kHz, hence lowering passive‐component sizes by up to 30% and raising conversion efficiencies over 96%. Favored for high-power outdoor and industrial luminaires, where thermal resilience and little cooling are most important, SiC's capability to work at junction temperatures above 175 °C and voltage ratings exceeding 1,200 V helps it to be sought after. To go after LED-driver markets, major semiconductor providers Infineon, ROHM, and GaN Systems are increasing capacity to meet performance requirements as well as sustainability objectives by lowering system-level energy wastage. Premium LED‐driver modules with wide‐bandgap semiconductors will become more prevalent across smart-street, architectural, and automobile lighting as economies of scale and better wafer yields cause GaN‐on‐Si and SiC components to grow in price competitiveness.

The market finds uses in Li-Fi and UV-LED applications, which will help the market grow faster.

Thanks to its chemical-free pathogen inactivation, UV-C LEDs (200–280 nm) for air and water disinfection saw a 78% year-over-year market rise in 2023, especially in healthcare and public-facility installations, which is generating particular demand for pulsed, high-power LED drivers. Emerging Li-Fi communication, lighting, and UV-LED disinfection systems are creating special demand for pulsed, high-power LED drivers. By modulating LED drivers at multi-megahertz frequencies, Li‑Fi prototypes in industrial environments have shown data rates exceeding 10 Gbps, therefore facilitating safe, RF‑free wireless communication for IoT sensors and factory automation. These applications require driver topologies with rapid transient response, broad output current ranges, and little EMI, driving R&D into bespoke, high‐speed ASICs and modular driver stacks. Driver manufacturers are debuting specialized product lines as public health and data-communication applications mature, therefore opening high-margin, niche markets outside of conventional lighting.

The rise of retrofit-ready modules is said to transform the market at a rapid scale.

Among utilities, distributors, and end-users searching for low-risk, quick-turn revenue streams, plug-and-play driver modules for LED-tube and downlight retrofits are gaining traction. Estimated to be worth USD 6.5 billion, retrofit markets are predicted to grow at 11% CAGR by 2030 as traditional fluorescent lights (T8/T12) are phased out under energy laws. Cutting installation time by 50% and removing ballast compatibility problems, these modules have universal 120–277 VAC inputs, integrated surge protection, and tool-free mounting. Wholesalers combine retrofit kits with utility rebate programs to speed conversions in commercial and industrial sites. For lighting OEMs, standardized retrofit drivers reduce SKUs and enable value-added features, dimming, and emergency backup, to propel margin growth in a traditionally low-cost industry.

The growing use of renewable-powered lighting technology is said to be a major market opportunity.

Driven by government rural-electrification programs in Sub-Saharan Africa and South Asia, the world off-grid solar lighting sector hit USD 2 7 billion and is expected to increase at 15% CAGR through 2030. Drivers for these applications incorporate MPPT algorithms to maximize panel output, support Li-ion or lead-acid battery chemistries, and deliver a low-voltage disconnect to protect cells. These systems for rural electrification using off-grid solar and wind-powered LED lighting demand drivers with broad input ranges (12–60 VDC) and built-in battery-management capacity. With IP65+ ratings for reliability, their strong construction has to tolerate intense humidity and temperatures. As decentralized renewable energy projects expand, demand for customized driver solutions combining power conversion, energy storage control, and load scheduling will soar, facilitating sustainable lighting in areas beyond grid reach.

LED Driver Market Segmentation:

Market Segmentation: By Luminaire Type

• Reflectors

• Type A Lamp

• Panel Lights

• Decorative Lamps

• Others

The Reflectors segment is said to dominate this market. This is because they are used in streetlights, high‑bay lighting, and architectural fixtures. With their widespread presence in outdoor and industrial applications necessitating strong drivers and high light output, reflectors make up the majority of their use. The Type A Lamp segment is said to be the fastest-growing one. Type A lights are growing at a faster rate as companies and consumers substitute LED choices for CFLs and incandescents, hence fueling great demand for appropriate plug-and-play drivers.

When it comes to the Panel Lights, they are said to see a steady growth as they are increasingly being adopted in sectors like healthcare and many other offices. This is because of their slim form and uniform illumination. Decorative lamps like pendants, chandeliers employ specialized drivers for color‑tunable and dimmable effects, thereby showing an increasing market in hospitality and residential projects. Linear tubes, strip lights, and special luminaires all belong to the Others category; they can be improved by focused retrofit projects and customized driver options for particular form factors.

Market Segmentation: By Application

• General Lighting

• Automotive Lighting

• Backlighting

Here, the General Lighting segment is said to hold dominance in the market. Driven by retrofit incentives, green‑building requirements, and widespread legacy system replacement, general indoor and outdoor lighting uses the great majority of LED drivers. The Automotive Lighting segment is the fastest-growing segment. From adaptive headlights to inside accent lighting, automotive uses demand strong reliability, vibration-proof drivers, which is driving double-digit expansion next to EV adoption. When it comes to the Backlighting segment, TVs, monitors, and signage based on LCD and mini-LED panels call for accurate current control to guarantee consistent brightness and color fidelity; hence, LED drivers support them.

Market Segmentation: By Component

• Driver IC

• Discrete Component

Here, the Driver IC segment dominates the market, and the Discrete component segment is the fastest-growing segment. Preferred by OEMs to reduce board space and ease thermal management in mass‑market luminaires, integrated circuits provide compact, high‑efficiency driver choices. Discrete MOSFETs, inductors, and capacitors are becoming more common in high-power and industrial luminaires to manage increased voltages and currents, hence enabling bespoke designs.

Market Segmentation: By Supply Type

• Constant Current

• Constant Voltage

The Constant Current segment is said to dominate the market, and the Constant Voltage segment is considered to be the fastest-growing segment of the market. Maintaining consistent LED brightness under diverse load circumstances, constant-current drivers make the standard choice for most applications needing flicker-free performance. Constant‑voltage drivers are most rapidly growing in the LED strip, panel, and retrofit sectors, where standard 12 V/24 V inputs simplify design and installation for end customers.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is said to lead this market. Driven by the extensive use of energy-efficient lighting products across the commercial and residential markets, North America continues to be the main consumer for LED drivers. The Asia-Pacific region is said to be the fastest-growing region of this market. Government programs and incentives fostering energy efficiency help to drive market expansion. Particularly in nations like China, India, and Japan, the Asia-Pacific area is expanding quickly.

The European market is defined by rising disposable income, urbanization, and significant infrastructure investments are driving demand for LED drivers across several sectors, including commercial and industrial lighting. Stringent rules meant to lower energy use and encourage sustainable lighting solutions have helped Europe's growth to be very strong. Adopting LED technology, including smart lighting systems, puts countries like Germany, the UK, and France ahead. Though the South American market is still small compared to other areas, awareness of energy-efficient lighting solutions is growing. Nations like Brazil and Argentina are starting to use LED technology. While the market size of the MEA region is small, as companies and homes try to increase energy efficiency, LED drivers are drawing more and more attention. Adoption of LED lighting systems is propelled by investment in smart city projects as well as infrastructure improvements.

COVID-19 Impact Analysis on the Global LED Driver Market:

Initially, the pandemic interrupted supply chains; semiconductor IC lead times extended by two to three months, and freight expenses soared by 40 to 60%, delaying driver deliveries. Concurrently, lockdown-driven drops in automotive and construction production softened near-term demand. By late 2020, government stimulation programs started funding infrastructure and smart-lighting projects, therefore driving a 15% increase in driver orders. Remote-monitoring capabilities became more important as facility managers gave touchless control and energy savings priority in light of occupancy restrictions. COVID‑19 quickened digital‑lighting changes and highlighted the resilience of LEDs, therefore supporting medium-term market expansion despite causing a shortfall.

Latest Trends/ Developments:

Transitioning to GaN power stages provides for compact form factors and >95% conversion efficiency for high‑power luminaires.

Straight incorporation of Bluetooth Mesh and Thread protocols into drivers enables smart buildings to have scalable, low-latency lighting networks.

Optimizing locations and maintenance schedules, create digital twins of lighting ecosystems using cloud-connected driver telemetry.

Constant-current drivers developed with flicker ratings < 5% satisfy demanding visual-comfort requirements in broadcast studios, healthcare, and retail.

Key Players:

• Osram GmbH (Germany)

• Harvard Engineering (U.K.)

• Texas Instruments (U.S.)

• Maxim Integrated (U.S.)

• Macroblock Inc. (Taiwan)

• Atmel Corporation (U.S.)

• General Electric (U.S.)

• Cree, Inc. (U.S.)

• ROHM Semiconductors (Japan)

• ON Semiconductor (U.S.)

Chapter 1. Global LED Driver Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global LED Driver Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global LED Driver Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global LED Driver Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global LED Driver Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global LED Driver Market- By Luminaire Type

6.1. Introduction/Key Findings

6.2. Reflectors

6.3. Type A Lamp

6.4. Panel Lights

6.5. Decorative Lamps

6.6. Others

6.7. Y-O-Y Growth trend Analysis By Luminaire Type

6.8. Absolute $ Opportunity Analysis By Luminaire Type, 2025-2030

Chapter 7. Global LED Driver Market– By Application

7.1 Introduction/Key Findings

7.2. General Lighting

7.3. Automotive Lighting

7.4. Backlighting

7.5. Y-O-Y Growth trend Analysis By Application

7.6. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global LED Driver Market– By Component

8.1. Introduction/Key Findings

8.2. Driver IC

8.3. Discrete Component

8.4. Y-O-Y Growth trend Analysis By Component

8.5. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 9. Global LED Driver Market– By Supply Type

9.1. Introduction/Key Findings

9.2. Constant Curren

9.3. Constant Voltage

9.4. Y-O-Y Growth trend Analysis By Supply Type

9.5. Absolute $ Opportunity Analysis By Supply Type, 2025-2030

Chapter 10. Global LED Driver Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Luminaire Type

10.1.3. By Application

10.1.4. By Component

10.1.5. By Supply Type

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Luminaire Type

10.2.3. By Application

10.2.4. By Component

10.2.5. By Supply Type

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Luminaire Type

10.3.3. By Application

10.3.4. By Component

10.3.5. By Supply Type

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Luminaire Type

10.4.3. By Application

10.4.4. By Component

10.4.5. By Supply Type

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Luminaire Type

10.5.3. By Application

10.5.4. By Component

10.5.5. By Supply Type

10.5.6. By Region

Chapter 11. Global LED Driver Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Osram GmbH (Germany)

11.2. Harvard Engineering (U.K.)

11.3. Texas Instruments (U.S.)

11.4. Maxim Integrated (U.S.)

11.5. Macroblock Inc. (Taiwan)

11.6. Atmel Corporation (U.S.)

11.7. General Electric (U.S.)

11.8. Cree, Inc. (U.S.)

11.9. ROHM Semiconductors (Japan)

11.10. ON Semiconductor (U.S.)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global LED Driver Market was valued at USD 20.19 billion in 2024 and is projected to reach a market size of USD 56.63 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.91%.

North America is said to dominate the market due to rising demand for energy-efficient lighting solutions, adoption of LED technology in various sectors, and strong support given to the market by the government for initiatives taken for the purpose of energy efficiency.

Miniaturization and integration needs in high‐density luminaires cause driver ICs to be the dominant segment of this market.

The pandemic is said to have a major impact on this market. Longer IC lead times caused by logistics bottlenecks and semiconductor shortages increased project schedules in 2020–2021 by two to three months.

Semiconductor supply shortages and extended lead times plague the market, therefore raising design complexity for intelligent and dimmable drivers, severe thermal-management requirements in small luminaires, and price sensitivity in cost-conscious areas.