IT And Telecom Cyber Security Market Research Report – Segmentation by Type (Network Security Solutions, Endpoint Protection Platforms, Cloud Security Services, Identity and Access Management, Security Analytics and Intelligence, Incident Response and Forensics, Compliance and Governance Tools, Mobile Security Solutions); By Distribution Channel (Direct Sales, Channel Partners and Resellers, System Integrators, Managed Security Service Providers, Online Marketplaces and Platforms); By Deployment Model (On-Premises Solutions, Cloud-Based Deployments, Hybrid Cloud Environments, Software-as-a-Service Offerings, Managed Security Services); By Organization Size (Large Enterprises, Medium-Sized Businesses, Small and Medium Enterprises, Government and Public Sector, Critical Infrastructure Operators); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16602

Format:

Region: Global

Market Size and Overview:

The IT And Telecom Cyber Security Market was valued at USD 35.11 Billion in 2024 and is projected to reach a market size of USD 63.24 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 12.49%.

The Information Technology and Telecommunications cybersecurity market has emerged as one of the most critical and rapidly expanding sectors within the global digital economy, representing a fundamental pillar of modern business infrastructure protection. This specialized market segment addresses the unique vulnerabilities and threats that specifically target IT and telecom industries, which serve as the backbone of global digital communications and data transmission. The market encompasses a comprehensive array of security solutions designed to protect telecommunications networks, IT infrastructure, data centers, cloud computing environments, and the vast interconnected systems that enable modern digital communications. The distinctive nature of this market stems from the critical role that IT and telecom companies play in maintaining global connectivity and digital infrastructure, making them exceptionally attractive targets for cybercriminals, nation-state actors, and sophisticated threat groups. These organizations handle massive volumes of sensitive customer data, financial information, personal communications, and critical business intelligence, creating an environment where security breaches can have cascading effects across multiple industries and geographic regions. The market has evolved beyond traditional perimeter security approaches to embrace comprehensive, multi-layered defense strategies that address the complex threat landscape facing modern telecommunications and IT infrastructure.

Key Market Insights:

Industry analysts report that cybersecurity spending by IT and telecom companies has increased by approximately 18% in 2024 compared to the previous year, with organizations allocating an average of 12% of their total IT budgets to cybersecurity initiatives.

The market has experienced a notable shift in investment priorities, with cloud security solutions accounting for approximately 28% of total spending in the IT and telecom cybersecurity market during 2024.

Network security solutions continue to represent the largest market segment, capturing approximately 35% of total market share in 2024, reflecting the critical importance of protecting the core infrastructure that enables IT and telecom operations.

Endpoint protection and response solutions have captured approximately 22% of market share in 2024, driven by the increasing complexity of threats targeting individual devices and access points within IT and telecom networks.

In 2024, healthcare and telecommunications stood out as prime targets for cyber threats, with telecom companies experiencing an average of 1,248 attempted cyberattacks per organization during the year.

Market Drivers:

Digital Transformation Acceleration

The unprecedented pace of digital transformation across IT and telecommunications sectors has created an expansive attack surface that requires sophisticated cybersecurity solutions to adequately protect. Organizations are rapidly adopting cloud computing technologies, implementing software-defined networking architectures, deploying Internet of Things devices at scale, and integrating artificial intelligence and machine learning capabilities into their core operations. This digital evolution has fundamentally changed the threat landscape, creating new vulnerabilities and attack vectors that traditional security approaches cannot adequately address. The convergence of IT and operational technology systems has blurred traditional security boundaries, requiring comprehensive security solutions that can protect both digital assets and physical infrastructure. As organizations become increasingly dependent on digital technologies for their core business operations, the potential impact of cybersecurity incidents has grown exponentially, driving substantial investments in advanced security technologies and services.

Regulatory Compliance Requirements

The IT and telecommunications industries face an increasingly complex web of regulatory requirements that mandate specific cybersecurity controls and practices, creating significant market demand for specialized compliance solutions. Regulations such as the General Data Protection Regulation, telecommunications privacy laws, critical infrastructure protection requirements, and industry-specific security standards require organizations to implement comprehensive cybersecurity programs that go far beyond basic security measures. These regulatory frameworks often include specific requirements for data encryption, access controls, incident response procedures, security monitoring, and regular security assessments, creating substantial demand for specialized cybersecurity solutions that can help organizations achieve and maintain compliance. The financial penalties associated with regulatory non-compliance can be severe, with some organizations facing fines that exceed tens of millions of dollars, creating strong economic incentives for robust cybersecurity investments.

Market Restraints and Challenges:

The IT and telecom cybersecurity market faces significant challenges including the acute shortage of qualified cybersecurity professionals, which has created substantial skills gaps that limit organizations' ability to effectively implement and manage sophisticated security solutions. The rapid pace of technological change often outpaces the development of corresponding security solutions, creating windows of vulnerability that can be exploited by malicious actors. Budget constraints remain a persistent challenge, particularly for smaller IT and telecom organizations that struggle to justify the substantial investments required for comprehensive cybersecurity programs while maintaining competitive pricing for their services.

Market Opportunities:

The emerging deployment of 5G networks and edge computing infrastructure presents substantial growth opportunities for specialized cybersecurity solutions designed to protect these next-generation technologies. The increasing adoption of artificial intelligence and machine learning technologies creates opportunities for innovative security solutions that can leverage these capabilities to improve threat detection and response. The growing recognition of cybersecurity as a business enabler rather than just a cost center is creating opportunities for security solution providers to develop offerings that directly support business objectives and revenue generation.

Market Segmentation:

Segmentation by Type:

Types:

• Network Security Solutions

• Endpoint Protection Platforms

• Cloud Security Services

• Identity and Access Management

• Security Analytics and Intelligence

• Incident Response and Forensics

• Compliance and Governance Tools

• Mobile Security Solutions

Network security solutions maintain their position as the most dominant segment within the IT and telecom cybersecurity market, accounting for the largest share of total market revenue due to the critical importance of protecting the core network infrastructure that enables all digital communications and data transmission activities.

Cloud security services represent the fastest-growing segment within the market, driven by the rapid migration of IT and telecom operations to cloud computing environments and the unique security challenges associated with protecting distributed, multi-tenant cloud infrastructure and hybrid deployment models.

Segmentation by Distribution Channel:

Distribution Channels:

• Direct Sales

• Channel Partners and Resellers

• System Integrators

• Managed Security Service Providers

• Online Marketplaces and Platforms

Direct sales remain the most dominant distribution channel within the IT and telecom cybersecurity market, as organizations typically prefer to work directly with security vendors for complex, mission-critical solutions that require extensive customization and ongoing support.

Managed security service providers represent the fastest-growing distribution channel, as IT and telecom organizations increasingly recognize the benefits of outsourcing specialized security functions to dedicated experts who can provide round-the-clock monitoring and response capabilities.

Segmentation by Deployment Model:

Deployment Models:

• On-Premises Solutions

• Cloud-Based Deployments

• Hybrid Cloud Environments

• Software-as-a-Service Offerings

• Managed Security Services

On-premises deployments continue to dominate the IT and telecom cybersecurity market due to regulatory requirements, data sovereignty concerns, and the need for organizations to maintain direct control over their most sensitive security infrastructure and processes.

Hybrid cloud deployments represent the fastest-growing segment as organizations seek to balance the flexibility and scalability of cloud computing with the control and compliance benefits of on-premises infrastructure.

Segmentation by Organization Size:

Organization Sizes:

• Large Enterprises

• Medium-Sized Businesses

• Small and Medium Enterprises

• Government and Public Sector

• Critical Infrastructure Operators

Large enterprises dominate the IT and telecom cybersecurity market in terms of total spending and solution complexity, as these organizations typically have the most extensive infrastructure, highest risk exposure, and largest budgets for comprehensive security programs.

Medium-sized businesses represent the fastest-growing segment as these organizations increasingly recognize their vulnerability to cyber threats and begin investing in more sophisticated security solutions previously available only to larger enterprises.

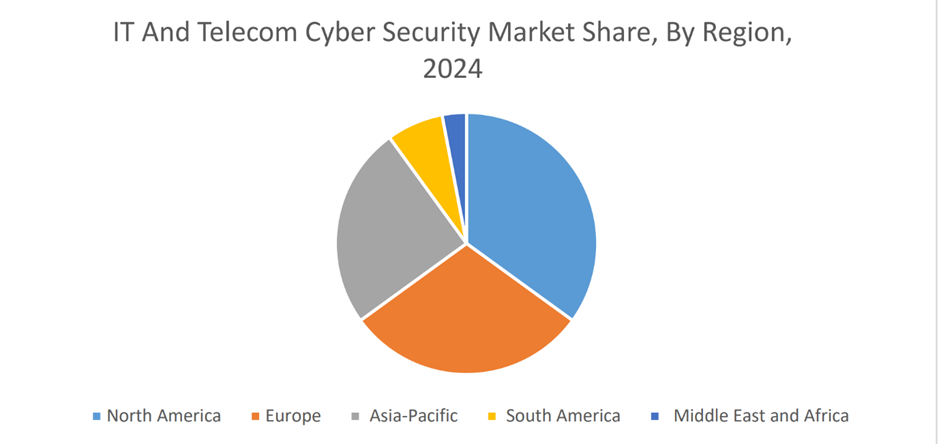

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America maintains its position as the most dominant region in the IT and telecom cybersecurity market, driven by the presence of major telecommunications companies, advanced threat landscapes, substantial cybersecurity investments, and comprehensive regulatory frameworks that mandate robust security controls.

The Asia-Pacific region represents the fastest-growing market for IT and telecom cybersecurity solutions, driven by rapid infrastructure development, increasing cyber threat sophistication, growing awareness of security risks, and substantial investments in digital transformation initiatives across the region.

COVID-19 Impact Analysis:

The COVID-19 pandemic has fundamentally transformed the IT and telecom cybersecurity market, accelerated digital transformation initiatives and created new security challenges that have driven substantial increases in cybersecurity spending. The rapid shift to remote work arrangements has expanded attack surfaces and created new vulnerabilities that require specialized security solutions. Organizations have increased their reliance on digital communications and cloud-based services, creating new security requirements and driving demand for advanced protection capabilities that can secure distributed work environments and digital collaboration platforms.

Latest Trends and Developments:

The IT and telecom cybersecurity market is experiencing significant innovation in artificial intelligence and machine learning applications, with organizations increasingly deploying automated threat detection and response capabilities. Zero-trust security architectures are gaining widespread adoption as organizations recognize the limitations of traditional perimeter-based security approaches. Quantum-resistant cryptography is emerging as a critical consideration as organizations prepare for future threats posed by quantum computing technologies. The integration of cybersecurity with business continuity and disaster recovery planning is becoming increasingly sophisticated as organizations recognize the interconnected nature of these critical business functions.

Key Players in the Market:

• AO Kaspersky Lab

• Broadcom

• Check Point Software Technology Ltd.

• Cisco Systems, Inc.

• CrowdStrike

• IBM Corporation

• McAfee, Inc.

• Microsoft

• Palo Alto Networks, Inc.

• Sophos

Chapter 1. Global IT And Telecom Cyber Security Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global IT And Telecom Cyber Security Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global IT And Telecom Cyber Security Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global IT And Telecom Cyber Security Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global IT And Telecom Cyber Security Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global IT And Telecom Cyber Security Market – By Type

6.1. Introduction/Key Findings

6.2. Network Security Solutions

6.3. Endpoint Protection Platforms

6.4. Cloud Security Services

6.5. Identity and Access Management

6.6. Security Analytics and Intelligence

6.7. Incident Response and Forensics

6.8. Compliance and Governance Tools

6.9. Mobile Security Solutions

6.10. Y-O-Y Growth trend Analysis By Type

6.11. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global IT And Telecom Cyber Security Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Direct Sales

7.3. Channel Partners and Resellers

7.4. System Integrators

7.5. Managed Security Service Providers

7.6. Online Marketplaces and Platforms

7.7. Y-O-Y Growth trend Analysis By Distribution Channel

7.8. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global IT And Telecom Cyber Security Market – By Deployment Model

8.1. Introduction/Key Findings

8.2. On-Premises Solutions

8.3. Cloud-Based Deployments

8.4. Hybrid Cloud Environments

8.5. Software-as-a-Service Offerings

8.6. Managed Security Services

8.7. Y-O-Y Growth trend Analysis By Deployment Model

8.8. Absolute $ Opportunity Analysis By Deployment Model, 2024-2030

Chapter 9. Global IT And Telecom Cyber Security Market – By Organization Size

9.1. Introduction/Key Findings

9.2. Large Enterprises

9.3. Medium-Sized Businesses

9.4. Small and Medium Enterprises

9.5. Government and Public Sector

9.6. Critical Infrastructure Operators

9.7. Y-O-Y Growth trend Analysis By Organization Size

9.8. Absolute $ Opportunity Analysis By Organization Size, 2024-2030

Chapter 10. Global IT And Telecom Cyber Security Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By Deployment Model

10.1.5. By Organization Size

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By Deployment Model

10.2.5. By Organization Size

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By Deployment Model

10.3.5. By Organization Size

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Distribution Channel

10.4.4. By Deployment Model

10.4.5. By Organization Size

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Distribution Channel

10.5.4. By Deployment Model

10.5.5. By Organization Size

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global IT And Telecom Cyber Security Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. AO Kaspersky Lab

11.2. Broadcom

11.3. Check Point Software Technology Ltd.

11.4. Cisco Systems, Inc.

11.5. CrowdStrike

11.6. IBM Corporation

11.7. McAfee, Inc.

11.8. Microsoft

11.9. Palo Alto Networks, Inc.

11.10. Sophos

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Digital Transformation Acceleration serves as the primary growth catalyst, as organizations rapidly adopt cloud computing technologies, software-defined networking architectures, and Internet of Things devices at scale, fundamentally expanding the attack surface and creating new vulnerabilities that require sophisticated cybersecurity solutions.

Critical Skills Shortage represents the most significant concern facing the market, as the acute shortage of qualified cybersecurity professionals has created substantial skills gaps that limit organizations' ability to effectively implement and manage sophisticated security solutions, potentially leaving critical vulnerabilities unaddressed despite substantial technology investments.

Cisco Systems, IBM Corporation, Microsoft Corporation, Palo Alto Networks, Fortinet Inc, Check Point Software Technologies, Symantec Corporation, Trend Micro Incorporated, McAfee LLC, FireEye Inc, CrowdStrike Holdings, Rapid7 Inc, Splunk Inc, Proofpoint Inc, and Zscaler Inc represent the leading vendors in the IT and telecom cybersecurity market, each offering specialized solutions designed to address the unique security challenges facing these critical industries.

North America currently holds the largest market share, estimated at around 35%.

Asia-Pacific has shown significant room for growth in specific segments.