Global Intelligent Building Automation Technologies Market Research Report – Segmentation By Technology (Sensor Technology, Connectivity Technology, Computing Technology), By Application (HVAC Control, Lighting Control, Security & Access Control, Energy Management, Others), By End-Use Industry (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare, Education, Retail), By Distribution Channel (Direct Sales, distributors, Online Retail), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-4161

Format:

Region: Global

Market Size and Overview:

The Global Intelligent Building Automation Technologies Market was valued at USD 117.37 billion in 2024 and is projected to reach a market size of USD 204.82 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 11.78%.

Combining cutting-edge sensors, communication protocols, and edge/cloud computing, intelligent automation improves HVAC, lighting, security, and energy systems, promoting operational efficiency and sustainability throughout commercial, residential, and industrial structures. Demand for integrated solutions keeps growing as companies seek digital-twin applications and AI-driven analysis.

Key Market Insights:

Commercial segment led with offices, retail malls, and hotel facilities using centralized BMS for energy efficiency and occupant comfort in 2024; it comprised around 45% of market income.

Driven by urbanization, government "smart city" projects, and extensive infrastructure development, Asia Pacific is expected to reach about 14% CAGR (2025–2030), surpassing North America and Europe.

As detailed data collection underpins automated control and predictive maintenance, sensors, temperature, occupancy, air-quality accounted for roughly 38% of overall technology revenues in 2024.

At around 20% CAGR, in-premise analytical edge-computing modules improved latency and decreased cloud-bandwidth requirements for time-critical building controls.

Intelligent Building Automation Technologies Market Drivers:

The rising focus on sustainability is driving the increased need for this market.

Supply limits and carbon-pricing schemes raised worldwide commercial building energy costs by an average of 8.5%, thereby pressuring operators to look for automation solutions providing consistent 20–30% reductions in HVAC and lighting consumption. Thanks to corporate ESG goals, 72% of Fortune 500 companies have established net-zero dates by 2040, making building automation a pillar of decarbonizing plans. Tax credits under the Inflation Reduction Act of up to 30% of project expenses for green-building retrofits have opened USD 5 billion in automation investments. 15% of smart buildings now subscribe to grid-peak-reduction programs, producing up to USD 0.50/ft² annually in performance incentives for operators. Utilizing real-time occupancy data, energy-management modules can dynamically change settings and thereby reduce electricity bills by 18 % in pilot implementations across office campuses. Further driving automation adoption is Europe's carbon price, over €100 /ton CO₂, with 60% of new EU-funded smart-city grants set aside for building controls.

The existence of strict rules and green building standards is driving the growth of this market.

Mandatory energy-efficiency codes, such as ASHRAE 90.1 in North America and the EU's Energy Performance of Buildings Directive, now need new structures to meet 30–40% savings against 2010 baselines by 2027. Voluntary certification programs such as LEED and BREEAM keep growing: over 120,000 structures worldwide have LEED status, with 45% of recent certifications citing advanced automation as a major driving force. To keep certification and prevent fines of up to USD 100,000 per building, compliance deadlines are driving retrofit cycles, 65% of Fortune 1000 portfolios intend system upgrades by 2027. Title 24 in California demands networked lighting controls in all commercial areas, therefore requiring smart control installations in more than 200 million ft² per year. Likewise, tightening requirements are in Asia-Pacific governments (Singapore's Green Mark 2025; India's GRIHA 5-star), linking tax incentives to building automation benchmarks. These standards not only demand automation but also standardize interoperability, hence lowering integration expenses and speeding deployments.

The use of IoT and AI-enabled predictive maintenance is helping this market to be innovative.

Integration of advanced IoT sensors (vibration, temperature, airflow) with AI/ML analytics is enabling genuine predictive-maintenance regimes, identifying equipment anomalies 7–14 days before failure. 82% of facility managers reported at least one automation-driven maintenance event, resulting in 40% less unplanned downtime and 25% lower maintenance expenditure. Boosting capital-planning accuracy by 30%, digital-twin solutions produce virtual simulations of HVAC and lift systems running "what-if" scenarios projecting performance under different load and environmental circumstances. Closed-loop controls help to automatically execute corrective actions like valve adjustments or compressor restarts without human participation, hence lowering mean time to repair (MTTR) by 35%. Additionally, enhancing technician utilization by 20%, predictive insights also help to optimize service-contract schedules by changing from fixed intervals to condition-based visits. For BMS suppliers and service integrators, this change from reactive to prescriptive maintenance distinguishes them most prominently and generates recurring revenue prospects in analytical subscriptions.

Initiatives taken by the governments regarding smart cities are driving the growth of this market.

Worldwide, intelligent-city initiatives are incorporating digital doubles of public structures and areas to synchronize building-automation schedules with traffic patterns, weather predictions, and energy-market signals. As municipal and private players look for consolidated asset-performance solutions, the worldwide digital-twin market for smart structures is predicted to grow at a roughly 18% annual growth rate, reaching USD 18 billion by 2030. A city-scale twin combines the sensor feeds of 1,200 buildings in Barcelona's 22@ area to maximize neighborhood cooling loads and cut peak energy demand by 12%. Linking digital-twin data with building-automation controls across over 5,000 structures, Dubai's Virtual Dubai platform allows for synchronized response to grid emergencies and maximizes district heating systems.

Intelligent Building Automation Technologies Market Restraints and Challenges:

The high level of upfront capital expenditure makes it difficult for businesses to afford it.

Commonly ranging from USD 15 to 25 per ft², complete building automation projects, which include networked sensors, edge-computing gateways, actuators, and system integration, represent a significant investment for many property owners, USD 1.5–2.5 million for a 100,000 ft² facility. Hardware acquisition, installation labor, which can be 50–60% of total spending, software licensing, and initial configuration comprise these expenses; annual maintenance adds another 5–10% of capital expenditure. The return on investment (ROI) thresholds landlords consider acceptable often exceed payback periods of 3–5 years in emerging markets, where energy is cheaper and capital is scarcer, hence postponing or reducing projects. Strained balance sheets post-pandemic have caused 38% of commercial real-estate owners to favor stand-alone energy-audit equipment even in mature markets. Vendors provide staggered deployments, lease financing, and performance-contract arrangements to reduce obstacles; however, the great upfront barrier is still a major restriction on market penetration.

The complexity regarding integration and interoperability is a major challenge faced by the market.

Modern automation platforms rely on different protocols, BACnet, Modbus, KNX, and bespoke controllers, hence, perfect integration is quite difficult. Custom middleware or protocol gateways are often required, adding USD 50–100K per project in licensing and engineering hours and extending implementation timelines by 20–30% due to debugging and interoperability testing. Moreover, unauthorized wiring schematics and ancient control logic in older buildings call for thorough site inspections and reverse engineering, thereby driving up professional-service expenditures. The absence of global standards compels suppliers to keep several integration toolsets, hence raising O&M complexity and the chance of vendor lock-in. In addition to slowing project delivery, these interoperability problems turn away property owners from seeking end-to-end automation in favor of fragmented, siloed improvements.

The concerns regarding security and privacy of data hinder market growth.

Once isolated, networked building controls are now exposed to corporate and public networks, hence providing new attack surfaces for ransomware and IoT vulnerabilities; 48% of facility managers list security-hardening expenses and data-compliance demands (GDPR, CCPA) as obstacles to their implementation. High-profile events, such as HVAC-system hacks that disrupted hospital activities, underline the need and inspire CISOs to demand more firewalls, network segmentation, and frequent penetration tests for BMS networks. Implementing end-to-end encryption and secure firmware update mechanisms can add 10–15% to hardware costs, whereas ongoing security monitoring services incur additional OPEX. Regulatory oversight of personal data collected by occupancy and access sensors further complicates deployments; strict consent-management and anonymization procedures are now required. These combined demands for privacy and cybersecurity slow procurement cycles and increase overall project costs, therefore slowing the rate of intelligent automation deployments.

The severe shortage of skilled workforce is a challenge for the market as it slows down its progress.

According to industry surveys, only 27% of building operations teams have the in-house competence to design, implement, and maintain advanced BMS and analytics platforms, hence creating high dependence on external consultants. Hiring certified integrators and IoT-skilled technicians is difficult; 54% of service companies report unfilled positions, and wage premiums for specialized personnel can exceed 20% of standard rates. Training current employees in digital-twin tools, edge-AI modules, and secure-networking adds 4–6 weeks per employee, during which projects stall or proceed with elevated risk. The lack of multidisciplinary experts combining control engineering, IT networking, and data science restricts the ability for major automation projects and adds up to 15% yearly to O&M costs. Until educational institutions and training programs develop specialized curricula, this talent gap will continue to be a major hindrance to market expansion.

Intelligent Building Automation Technologies Market Opportunities:

The retrofitting of aging building stock presents a great market growth opportunity.

Retrofitting such stock with wireless occupancy, air-quality, and temperature sensors plus edge-computing controllers provides instant energy savings of 20–35% by allowing zone-level control and analysis without the cost of entire renovations. With programs like the EU's Energy Performance of Buildings Directive and the U.S. Inflation Reduction Act's 30% tax credit, North America and Europe lead in incentives, providing subsidies covering 20–40% of retrofit expenses. To achieve 2050 decarbonization targets, however, retrofit rates must triple from 1% to 3% of building stock each year, necessitating an estimated USD 3 trillion in expenditures over the next decade. Phased retrofit schemes, starting with "low-hanging fruit" like LED illumination and plug-load sensors, help landlords control capex, whereas digital-twin pilots confirm ROI and simplify scale-up.

The emergence of subscription-based services is a major market growth opportunity.

With gross margins of 25–30%, cloud-hosted BMS platforms and fully managed analytics services now make up about 30% of new contracts; providers lower entry obstacles for small-to-mid-sized landlords by combining sensor-health monitoring, firmware updates, and abnormality alarms into monthly charges, thereby increasing addressable market by 40% in secondary and tertiary cities. Predictive-maintenance subscriptions alone have 80% renewal rates as continual optimization yields 15–20% yearly O&M savings. FinOps dashboards and API-driven integrations into ERP systems further cement recurring revenue streams, with average contract lengths extending to 5–7 years, growing lifetime value (LTV) by 25% compared to one-time sales.

The integration of this market with remote microgrids is a huge market opportunity.

By hosting EV-charging stations and behind-the-meter solar-battery microgrids, commercial and residential structures are developing into grid-interactive prosumers. Intelligent-automation systems now coordinate bidirectional flows, shifting EV charging to off-peak times and deferring HVAC loads during peak rates, unlocking USD 0.50–1.00/ft² per year in demand-response revenues. Hybrid microgrid pilots integrating PV, battery storage, and EV chargers achieved 99.9% uptime and 25% lower utility costs in recent trials, as IoT-based EMS platforms optimize dispatch via AI-driven forecasts. Vehicle-to-Grid (V2G) standards now allow buildings to re-export stored energy during grid stress events, further monetizing on-site assets and reducing carbon footprints. Microgrid-EV integration sets smart building operators apart as governments tighten renewable-portfolio requirements.

The chance of enhancement of AI-driven workplace experience is a major market growth opportunity.

With employee well-being now linked to ESG and real-estate valuations, AI-driven experience enhancements represent a high-margin upsell for automation vendors. Post-pandemic demand for healthier, more personalized workplaces is accelerating the uptake of occupant-centric controls that leverage AI and real-time feedback to tailor HVAC, lighting, and air quality to individual preferences. Systems like BrainBox AI have demonstrated 60% improvement in occupant comfort scores and 15–25% HVAC-energy reductions within three months, with minimal CAPEX. Advanced machine-learning models ingest occupancy schedules, external-weather forecasts, and user-input profiles to adjust temperature setpoints and circadian lighting schedules, boosting productivity metrics by 8–12%. Real-time dashboards allow tenants to review personalized comfort data, enhancing Tenant Satisfaction Scores (TSS) and commanding up to a 15% premium in rental rates.

Intelligent Building Automation Technologies Market Segmentation:

Market Segmentation: By Technology

• Sensor Technology

• Connectivity Technology

• Computing Technology

The Sensor Technology segment is said to dominate the market because exact, ubiquitous sensing is fundamental to all automation. Covers occupancy, air-quality sensors that feed real-time data into automation systems to drive control logic and analytics. With granular monitoring supporting all downstream controls, sensors made up the greatest expenditure at roughly 38% of technology revenues in 2024. The Computing Technology is said to be the fastest-growing segment. Driven by the need for edge AI and digital-twin analytics in current BMS systems, computation technology is among the fastest-growing. Includes edge-computing gateways and cloud-based analytics engines running AI/ML models, predictive-maintenance algorithms, and digital-twin simulations. Demand by operators for low-latency, on-premises processing for mission-critical controls and to lower cloud-bandwidth expenditures makes this area the fastest-growing (approximately 15% CAGR). Driven by retrofits in old buildings requiring non-invasive wireless solutions, connectivity investments make up about 30% of the market.

Market Segmentation: By Application

• HVAC Control

• Lighting Control

• Security & Access Control

• Energy Management

• Others

The HVAC Control segment dominates this market. HVAC Control is dominant because of its vital importance for occupant comfort and great energy usage. Automates heating, ventilation, and air-conditioning based on occupancy and environmental inputs, providing 20–30% energy savings. The Energy Management segment is said to be the fastest-growing segment. Driven by net-zero goals and dynamic utility-program participation, energy management monitors and optimizes whole-building or district-level energy flows, including demand-response and microgrid coordination. This is the fastest-growing application (about 18% CAGR) as sustainability requirements and utility-incentive programs drive complex energy-optimization deployments.

Under the Lighting Control segment, dims or switches lighting according to occupancy and daylight harvesting, therefore cutting lighting energy usage by 25%. Simple retrofitting projects with lighting control make up around 25% of application expenditure. The Access Control and Security segment represents about 20% of the market, integrates video analytics, IoT door locks, and credential management for unified safety and occupant-flow monitoring. The others segment includes font cooling, water management automation, and fire safety locks, which make up around 5% market share.

Market Segmentation: By End-Use Industry

• Commercial Buildings

• Residential Buildings

• Industrial Facilities

• Healthcare

• Education

• Retail

The Commercial Buildings segment is said to dominate the market. Commercial Structures, the biggest single built space category with great energy-management stakes. Large refurbishment projects intended to lower energy costs and tenant-experience improvements drive about 45% of market income from offices, retail malls, hotels, and mixed-use buildings. The Healthcare segment is the fastest-growing segment of the market. Driven by the urgent requirement for exact environmental control and post-pandemic safety standards, healthcare is the fastest-growing sector. With roughly 10% market share, hospitals, labs, and clinics are investing in critical-environment controls and air quality monitoring, the fastest-growing vertical (about 16% CAGR), driven by strict health-safety and regulatory demands.

Under the Industrial Facilities segment, it is used by the factories and warehouses for predictive maintenance and environmental control purposes. For the Residential Facilities, families use them for premium amenities. It covers 15% market share. The Education and Retail segments together are forming about 10% of the market share. These are stores and colleges using automation to lower OPEX and enhance user comfort.

Market Segmentation: By Distribution Channel

• Direct Sales

• Distributors

• Online Retail

The Direct Sales segment dominates this market, and the Online Retail segment is said to be the fastest-growing segment. Direct Sales, driven by complex, large-scale integration projects requiring bespoke engineering. OEMs and system integrators sell turnkey automation solutions and full-service contracts directly to large building portfolios, accounting for ≈55% of channel revenues. The Online Retail segment is fueled by the emergence of plug-and-play IoT devices and tiny property automation needs. Off-the-shelf IoT sensors, do-it-yourself BMS systems, and cloud-managed lighting controllers provide quick deployment for small properties; this channel is the fastest-growing (around 20% CAGR) as ease-of-purchase and self-installation draw in new entrants. Under the Distributors segment, with nearly 30% of the market, Regional value-added Resellers and systems integrators assist small and medium-sized enterprises.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

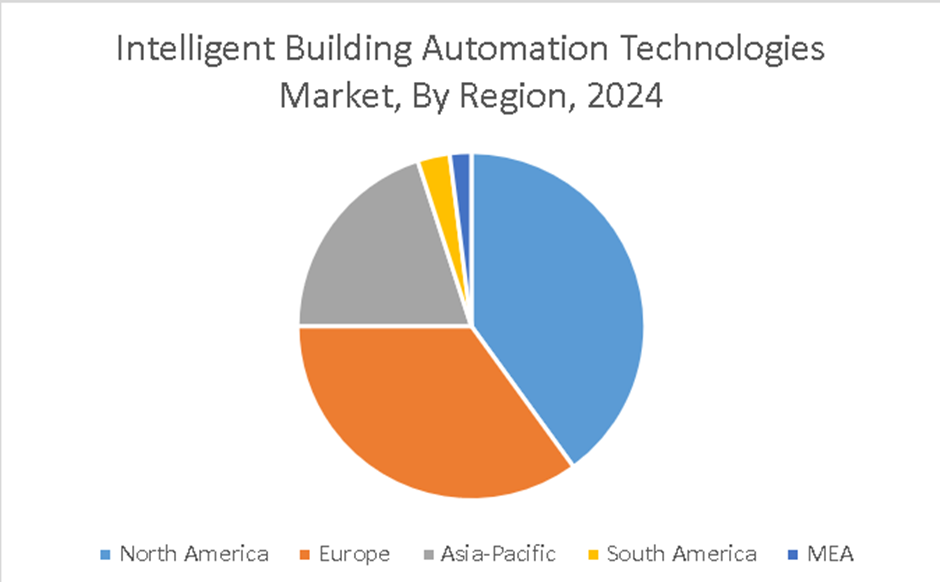

North America leads this market, owing to mature markets and ambitious sustainability goals. It is driven by strong energy codes, retrofit incentives, and high penetration of smart-building technologies. The Asia-Pacific region is the fastest-growing region of the market. Fuelled by urbanization, smart-city projects, and growing facility-management modernization, Asia Pacific is the fastest-growing area at around 14% CAGR. China, India, and Southeast Asia begin large-scale urbanization, smart-city rollouts, and industrial park automation.

Driven by the Europe’s Energy Performance of Buildings Directive and robust green-building certification programs, Europe has around 25 percent of the market. South America has a share of about 7%; pilots in smart campuses and commercial retrofits are getting attention. When it comes to the MEA region, it holds around 3% share, growing as GCC countries and South Africa invest in smart infrastructure for fresh projects.

COVID-19 Impact Analysis on the Global Intelligent Building Automation Technologies Market:

The epidemic underlined the need for remote monitoring and touch-free controls, which in 2020–2021 drove a 20% increase in demand for cloud-based BMS and AI-driven occupancy analytics. Health-safety measures hastened the adoption of contactless access-control and air-quality sensors, features that are now baseline expectations. Project priorities moved to employee-wellness dashboards and mobile-app integration to control building use and cleaning schedules, permanently increasing intelligent automation requirements.

Latest Trends/ Developments:

Real-time 3D building models synced with live sensor data boost scene-planning accuracy and facility-management procedures.

Ultra-reliable, low-latency 5G networks enable sensor deployment in legacy buildings without rewiring, hence speeding up installations by 30%.

Through safe microservices, edge-AI markets let building owners subscribe to vertical-specific analytical applications such as peak-load forecasting and indoor-wayfinding.

Among building-cluster microgrids, immutable ledgers are under trial for audit-proof access events and P2P energy trades.

Key Players:

• Honeywell International Inc

• Schneider Electric SE

• Trane Technologies pic

• Azbil Corporation

• Robert Bosch GmbH

• Cisco Systems, Inc.

• CBRE Group, Inc.

• Spaceti

• Johnson Controls International PLC

• Carrier Global Corporation

Chapter 1. Global Intelligent Building Automation Technologies Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Intelligent Building Automation Technologies Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Intelligent Building Automation Technologies Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Intelligent Building Automation Technologies Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Intelligent Building Automation Technologies Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Intelligent Building Automation Technologies Market- By Technology

6.1. Introduction/Key Findings

6.2. Sensor Technology

6.3. Connectivity Technology

6.4. Computing Technology

6.5. Y-O-Y Growth trend Analysis By Technology

6.6. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 7. Global Intelligent Building Automation Technologies Market– By Application

7.1 Introduction/Key Findings

7.2. HVAC Control

7.3. Lighting Control

7.4. Security & Access Control

7.5. Energy Management

7.6. Others

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Intelligent Building Automation Technologies Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. Commercial Buildings

8.3. Residential Buildings

8.4. Industrial Facilities

8.5. Healthcare

8.6. Education

8.7. Retail

8.8. Y-O-Y Growth trend Analysis By End-Use Industry

8.9. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Intelligent Building Automation Technologies Market– By Distribution Channel

9.1. Introduction/Key Findings

9.2. Direct Sales

9.3. Distributors

9.4. Online Retail

9.5. Y-O-Y Growth trend Analysis By Distribution Channel

9.6. Absolute $ Opportunity Analysis By Distribution Channel , 2025-2030

Chapter 10. Global Intelligent Building Automation Technologies Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Technology

10.1.3. By Application

10.1.4. By End-Use Industry

10.1.5. By Distribution Channel

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Technology

10.2.3. By Application

10.2.4. By End-Use Industry

10.2.5. By Distribution Channel

10.2.6. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Technology

10.3.3. By Application

10.3.4. By End-Use Industry

10.3.5. By Distribution Channel

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Technology

10.4.3. By Application

10.4.4. By End-Use Industry

10.4.5. By Distribution Channel

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Technology

10.5.3. By Application

10.5.4. By End-Use Industry

10.5.5. By Distribution Channel

10.5.6. By Region

Chapter 11. Global Intelligent Building Automation Technologies Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Honeywell International Inc

11.2. Schneider Electric SE

11.3. Trane Technologies pic

11.4. Azbil Corporation

11.5. Robert Bosch GmbH

11.6. Cisco Systems, Inc.

11.7. CBRE Group, Inc.

11.8. Spaceti

11.9. Johnson Controls International PLC

11.10. Carrier Global Corporation

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Intelligent Building Automation Technologies Market was valued at USD 117.37 billion in 2024 and is projected to reach a market size of USD 204.82 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 11.78%.

With almost 45% of revenues, commercial buildings (offices, retail, hospitality) lead because of large portfolios of aging assets looking for centralized BMS improvements and sustainability credentials.

Fuelled by fast urbanization, government smart-city investment, and rising adoption of IoT-driven efficiency solutions in China, India, and Southeast Asia, Asia Pacific is the fastest-growing region at around 14% CAGR (2025–2030).

The move from CapEx to OpEx, by means of cloud-hosted BMS and managed analytics subscriptions, lowers entry barriers, hence expanding adoption among small-to-mid-sized property owners and producing recurring-revenue flows for vendors.

Important trends include edge-AI for on-site analytics, 5G-backed wireless sensor networks, digital-twin integration for real-time simulation, and blockchain-enabled energy trading, all of which open up new revenue streams and distinguish service offers.