Global Home Energy Management System Market Research Report – Segmentation By Product Type (Smart Thermostats, Energy Monitors, Lighting Controls, Smart Plugs), By Communication Technology (Wi-Fi, Zigbee, Z-Wave, Others), By End-User (Single-Family Homes, Multi-Family Homes, Apartments, Villas), By Distribution Channel (Direct Sales, Distributors, Online Retail), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16592

Format:

Region: Global

Market Size and Overview:

The Global Home Energy Management System Market was valued at USD 3.80 billion in 2024 and is projected to reach a market size of USD 8.28 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.86%.

High smart-speaker penetration (present in over 45% of U. S. households) has lowered the barrier to entry as voice-enabled HEMS capabilities seamlessly merge into current ecosystems. Particularly Wi‑Fi, which has a 45% device share, wireless connection standards help plug‑and‑play installations without much wiring. Continuous innovation in AI-driven optimization and edge processing promises to further enhance data privacy and system performance, thereby paving the way for ongoing market growth into 2030.

Key Market Insights:

High smart-thermostat adoption and usefulness rebate schemes in the United States and Canada drove 38% of worldwide HEMS income.

Favored for their easy incorporation with current home networks and broad consumer familiarity, Wi‑Fi–enabled HEMS devices possessed 45% of the connectivity sector.

With over 35% of sales, smart thermostats are the biggest product category since they offer instant comfort and cost-saving advantages that justify the initial smart-home costs.

Home Energy Management System Market Drivers:

The huge rise in residential energy costs is driving the growing need for this market.

Rising from USD 0.18/kWh in Q1 to USD 0.195/kWh in Q4, an 8.5% rise over two years as wholesale and retail markets tightened, the world-average household electricity price climbed. Along with rising demand, global electricity usage increased 4. 3% in 2024 per IEA—homeowners must deal with growing utility costs, sometimes reaching more than USD 2,500 annually. HEMS deployments have sped up as a result, allowing load shifting to off-peak rates and automated demand response, which studies indicate could reduce household expenditures by 15–20%. To flatten peaks and prevent expensive times, these systems combine smart thermostats, real-time pricing signals, and appliance scheduling. HEMS offers a great ROI, usually recouped within 2–3 years, driving double-digit market expansion worldwide as energy prices stay high in light of climate-driven volatility.

The latest government incentives and rebates are said to drive the growth of this market.

Administered by states and tribes via the DOE's Home Energy Rebates Program, the Inflation Reduction Act authorized USD 8.8 billion for Home Energy Rebates programs, covering up to 30% of retrofit costs for insulation, electrification, and efficiency enhancements. Similarly, the EU's Renovation Wave plan allocates recovery money and cohesion grants to support clever home installations, including HEMS hardware and expert costs, therefore lowering net expenses by 20 to 30%. These incentives have halved payback periods, therefore inspiring widespread adoption among homeowners who would otherwise see HEMS as prohibitively expensive. Low-income families are given priority among rebates, hence improving financial inclusion. The result is a chain of HEMS initiatives going outside early adopters into mainstream markets, supporting strong growth forecasts for 2030.

The growing proliferation of smart hubs is considered to be a major market driver.

45% of U.S. houses currently include voice-controlled smart-speaker platforms like Amazon Alexa and Google Assistant, which incorporate energy-management "skills" that enable homeowners to use simple voice commands to change thermostats, lights, and appliance schedules. Because many gadgets need only a software update to fit into already established smart‑speaker environments, this ubiquity has dropped the barrier to entry for HEMS. Often utilizing these voice hubs, utility pilots boost user participation and happiness by providing real-time consumption warnings and demand-response notices. The familiarity and ease of voice control have turned HEMS from small installs into mass-market products, therefore speeding up worldwide deployment rates and creating the groundwork for more profound AI-driven automation.

The recent integration of renewable and EV charging is helping this market to gain an advantage.

As household EV ownership grows at 30% CAGR and rooftop solar capacity exceeds 1 TWh worldwide, homeowners increasingly use HEMS to coordinate bidirectional power flows between PV arrays, battery storage, and chargers. Intelligent scheduling algorithms synchronize EV charging with peak solar generation, therefore maximizing self‑consumption and obviating pricey grid imports throughout times of peak demand. Additionally, HEMS supports vehicle‑to‑home (V2H) and vehicle‑to‑grid (V2G) scenarios, in which EV batteries serve as dispatchable storage to smooth household loads and provide grid services. Through bill savings, tariff arbitrage, and incentive payments, HEMS delivers €340–€1,000 of annual value, thus considerably improving ROI and accelerating adoption across both established and developing countries by optimizing these clean‑energy assets.

Home Energy Management System Market Restraints and Challenges:

The existence of a high initial investment needed for this market is a major challenge, as it hampers its adoption rate.

The upfront cost, which can exceed USD 1,200 for a basic package of gadgets, expert installation, and a year of cloud subscription charges, is a major obstacle to HEMS adoption. This sticker shock is especially severe in developing countries where average household incomes are lower, leading many cost‑sensitive customers to postpone purchases or choose single‑device rather than full‑home solutions. Buyers, even in developed countries, view payback periods of 2–3 years as too extended in light of their investment horizons. Though these sometimes lack the thorough analysis and remote-management capabilities of fully integrated HEMS, manufacturers have developed lower-priced DIY kits. Consequently, tech enthusiasts and affluent homeowners still exhibit the highest market penetration; other residential groups are awaiting lower hardware prices and more easily available financing options.

The market faces a challenge through the complexity in the process of integration, which slows down market operations.

Often discovering compatibility issues, obsolete wiring, non‑standard HVAC gear, and patented control systems, that call for bespoke gateway solutions and expert-grade middleware, retrofitting HEMS into legacy homes calls for a 4 to 6 week average installation time, wherein installers must examine current electrical and communications infrastructure, source specialized interface modules, and thoroughly test end-to-end performance. From signal interference in Wi‑Fi mesh networks to mismatched voltage ranges in older heating systems, each site's particular arrangement can cause unforeseen integration difficulties. These difficulties raise labor expenses, typically USD 100–150 per hour, and can reduce client satisfaction as installers run into unexpected problems. Though simplified, plug-and-play designs are still a target; genuine "install anywhere" HEMS systems are years away; therefore, maintaining professional services as a vital and expensive element of the value chain.

The rising concerns regarding the privacy of the data are a great challenge that hampers its growth potential.

Regular monitoring of appliance-level use and occupancy patterns among homeowners raises legitimate privacy concerns. According to a qualitative analysis, "privacy-conscious citizens" worry that exposed granular HEMS data, perhaps exposing daily routines or absence periods, could be misused, so some people refuse to systems. A quick review shows that with many users hesitant to share data in the absence of clear, mutually beneficial protections, worries about loss of autonomy and data control present major obstacles to participation in smart‑local energy systems. Compounding this, fewer than 15% of smart-thermostat consumers investigate supplier privacy policies, therefore highlighting a trust gap that HEMS companies must overcome. Many possible users will still be skeptical of HEMS systems until producers include “privacy‑by‑design,” provide clear data-handling policies, and provide user-friendly consent controls.

The technology standards of the market are fragmented, which poses difficulties for the market.

Multiple wireless protocols, ZigBee, Z‑Wave, Thread, Wi‑Fi, and proprietary vendor APIs split the HEMS environment, therefore creating an uneven user experience and limited device interoperability. Every protocol has different frequency ranges, network topologies, and security systems, which forces HEMS gateways to install complicated translation layers that increase costs and delay. Matter's rise as a unifying smart home standard is encouraging, but adoption is erratic and will take years to spread throughout traditional systems. Consumers, therefore, have to negotiate compatibility charts and often buy several hubs or branded ecosystems, thereby diminishing the value proposition of HEMS. Broad industry agreement on open standards and strong certification programs will be required for true plug‑and‑play interoperability to guarantee smooth cross‑vendor device integration.

Home Energy Management System Market Opportunities:

The growing use of AI-driven energy optimization techniques is considered a major market growth opportunity.

According to a recent analysis in Buildings, by deliberately turning off unnecessary sensors and concentrating on high‑impact data inputs, a gradient‑boosting regressor model could cut HVAC energy consumption by up to 13%, therefore lowering system expenses by 13% while still maintaining accuracy. Treating load scheduling as a Markov Decision Process, elsewhere, reinforcement-learning-based systems learned best appliance-use policies over time and achieved 20% monthly bill reductions vs conventional ILP approaches. Driving an extra 10 to 12 percent savings over traditional rule-based systems and speeding HEMS ROI, these AI-driven optimizations constantly refine control strategies in reaction to real-time data.

The high demand for subscription-based services helps in growing the demand for this market.

The move toward subscription-based HEMS solutions is opening up regular revenue streams and greater lifetime value per user. According to industry research, combining hardware with cloud analytics, proactive maintenance, and automated utility‑bill reconciliations can increase average revenue per user by 25–30% over purely hardware‑centric models. Platforms like Schneider Electric's EcoStruxure provide tiered SaaS packages, ranging from basic monitoring to premium AI‑optimization modules, with monthly payments beginning at USD 10–20. These services typically feature automated fault detection alerts, consumption benchmarking, and customized energy‑saving advice, therefore improving stickiness: churn rates for subscription‑bundled HEMS fall under 5% yearly against 15% for single appliances. The consistent OPEX model reduces the first obstacles for homeowners, enabling them to progressively scale features as needed, therefore giving vendors steady, long-term income.

The latest and fastest expansion seen in the emerging nations has made them a new place for business.

With expected CAGRs above 18% through 2030, emerging markets in India, Southeast Asia, and Latin America are ready for fast HEMS development. In India, residential electricity prices have increased by 12% annually, therefore driving demand for energy management solutions among the growing middle class. Pilot projects in Brazil and Mexico, supported by local utilities, report 20–25% reductions in peak residential demand following HEMS roll‑outs in social-housing projects. Southeast Asia's smart-city initiatives in Kuala Lumpur and Bangkok include HEMS in green building rules, offering tax incentives to homeowners who install approved systems. Mobile‑first HEMS applications simplify user interaction as smartphone adoption approaches 70% in these regions. The combination of rising energy prices, urbanisation, and digitally savvy communities provides ideal ground for affordable, scalable HEMS solutions modified to local needs.

The integration of this market with energy storage unlocks new possibilities for this market.

Combining HEMS with residential battery storage opens up premium-priced advanced use cases, such as backup-power provisioning and automated demand-response engagement. According to research, reinforcement-learning-based HEMS management of PV-battery systems cuts monthly energy expenses by 20% compared to rule-based techniques while allowing for proactive load-shedding during grid failures. HEMS can arrange battery charging during off‑peak hours and discharge during peak, therefore producing arbitrage profits of €200–€400 yearly in areas with time‑of‑use tariffs. With performance-guarantee clauses ensuring consumers of minimum savings, packaged offerings, combining solar panels, batteries, and HEMS under one contract are becoming popular in Australia and California. Appealing to high‑value customers searching for resilience and sustainability, these ready-to-use "solar + storage + HEMS" packages command 20–30% higher average selling prices than individual component sales.

Home Energy Management System Market Segmentation:

Market Segmentation: By Product Type

• Smart Thermostats

• Energy Monitors

• Lighting Controls

• Smart Plugs

Smart thermostats segment is said to lead the market as homeowners give urgent comfort and bill‑saving priority by means of automated HVAC management and learning algorithms, representing 35%. The Energy Monitors segment is the fastest-growing segment of the market. Energy monitors provide detailed, appliance-level insights that promote greater consumer involvement and more savings opportunities, therefore expected to record the highest CAGR (more than 16%) by 2030.

In the Lighting Controls segment, this segment is said to account for 15% of the market share. This is due to occupancy-based controls and LED retrofits that lead to energy savings. The Smart Plug segment makes up around 15% share; plug‑and‑play simplicity lets consumers automate and monitor single appliances without wiring modifications.

Market Segmentation: By Communication Technology

• Wi-Fi

• Zigbee

• Z-Wave

• Others

The Wi-Fi segment is said to dominate the market with a market share of 45%. This is due to existing routers that are used for plug-and-play installations and device compatibility. ZigBee is said to be the fastest-growing segment of the market. With an anticipated ~14% CAGR, ZigBee's low-power mesh network is especially good in multi-sensor HEMS installations, therefore increasing range and battery life.

The Z-Wave segment is said to represent around 20% market share, appreciated for its dependability in certified smart‑home ecosystems and interoperability across them. When it comes to the others segment, share totaling around 20%; emerging standards provide improved security and IPv6 support, yet early adoption phases still prevail.

Market Segmentation: By End-User

• Single-Family Homes

• Multi-Family Homes

• Apartments

• Villas

The Single-Family Homes segment dominates this market, and the Multi-Family and Apartments segment is the fastest-growing segment. The Single-Family Homes segment is driven by detached-home owners' capacity to retrofit entire-home systems and get government rebates, capturing 55% of installs. The Multi-Family Homes and Apartments segment is said to be growing at more than 18% CAGR. These categories use shared-infrastructure models and landlord-driven renovation initiatives to combine expenses and benefits. The Villas segment comprises around 15%; high‑end customers choose luxury‑grade HEMS for integrated comfort, security, and energy management.

Market Segmentation: By Distribution Channel

• Direct Sales

• Distributors

• Online Retail

The Online Retail segment is said to be the dominant segment of the market. 60% of sales are accounted for as e‑commerce sites allow for quick product discovery, competitive pricing, and next‑day delivery. The Direct Sales segment is growing at around 20% CAGR through HVAC contractors and utility schemes that combine HEMS with equipment service contracts for simplified installs. The Distributors segment holds around 20% of the market share, which is due to the supply of smart home integrators and regional installers.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

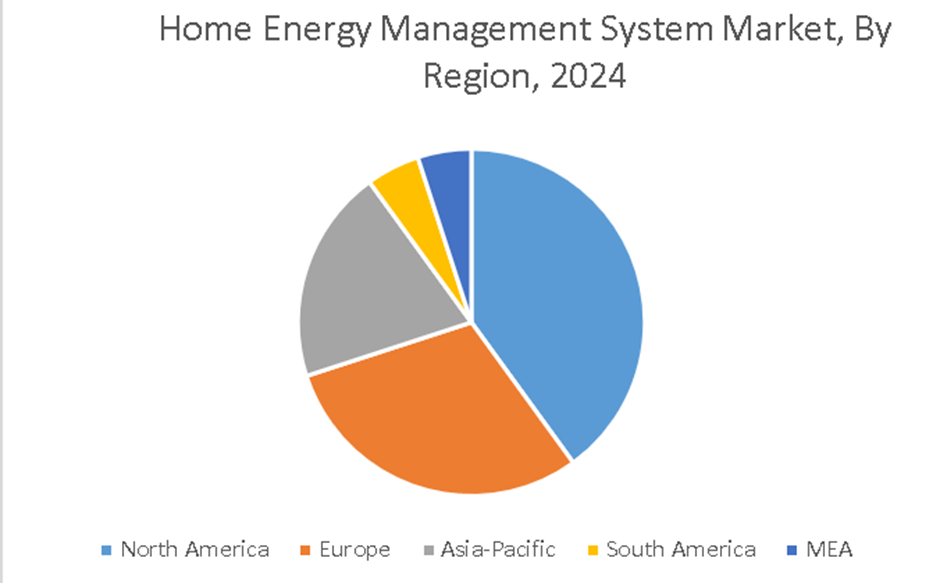

North America is said to lead this market. With 38% of global HEMS revenue in 2024, driven by mature rebate programs, high smart‑speaker penetration, and sophisticated smart‑grid pilot initiatives. The Asia-Pacific region is said to be the fastest-growing segment. Driven by fast urbanization, growing energy prices in China and India, and government smart-city directives, projected to achieve a 17% CAGR.

Europe is said to hold around 25%; adoption is aided by strict construction efficiency codes and residential energy-saving incentives. Both MEA and South America are considered emerging markets. Rising environmental consciousness and better broadband access fuel expansion in developing economies with undeveloped smart home systems.

COVID-19 Impact Analysis on the Global Home Energy Management System Market:

Supply-chain bottlenecks postponed device deliveries by 4–6 weeks, whereas consumers deprioritized house renovations in the middle of financial uncertainty. But steady work-from-home policies and surges in household electricity consumption drew attention back to automated energy systems. Virtual consultations and touchless installations arose, supporting a 30% year-on-year market recovery by mid-2021. Additionally, expanded to aid post-pandemic economic recovery, utility rebate programs more motivate HEMS renovations. Online retail outlets rose, capturing 60% of sales as homeowners embraced remote purchasing. Consumer interest in comfort‑energy trade‑offs and real‑time monitoring confirmed HEMS as a resiliency tool, guaranteeing ongoing market expansion despite first hiccups.

Latest Trends/ Developments:

50% of new HEMS equipment includes Amazon Alexa or Google Assistant, so customers may effortlessly run multi‑device routines while modifying their thermostats and lighting hands‑free.

By locally analyzing consumption patterns, on-device machine-learning inference is increasingly conventional, hence lowering cloud dependence, speeding reaction times, and protecting tenant data.

Using HEMS data on blockchain systems, pilot projects in North America and Europe are enabling peer‑to‑peer solar energy exchanges and dynamic local microgrid settlements.

Increasing average revenue per user by 25–30% and enhancing long‑term customer retention, emerging HEMS products combine hardware with SaaS dashboards and automated fault‑detection signals.

Key Players:

• Honeywell International Inc. (US)

• Nest Labs Inc. (US)

• Vivint, Inc. (US)

• General Electric Company (US)

• Ecobee Inc (Canada)

• Alarm.com (US)

• Comcast Cable (US)

• Panasonic Corporation (Japan)

• Ecofactor Inc. (US)

• Energyhub Inc. (US)

Chapter 1. Global Home Energy Management System Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Home Energy Management System Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Home Energy Management System Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Home Energy Management System Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Home Energy Management System Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Home Energy Management System Market- By Product Type

6.1. Introduction/Key Findings

6.2. Smart Thermostats

6.3. Energy Monitors

6.4. Lighting Controls

6.5. Smart Plugs

6.6. Y-O-Y Growth trend Analysis By Product Type

6.7. Absolute $ Opportunity Analysis By Product Type, 2025-2030

Chapter 7. Global Home Energy Management System Market– By Communication Technology

7.1 Introduction/Key Findings

7.2. Wi-Fi

7.3. Zigbee

7.4. Z-Wave

7.5. Others

7.6. Y-O-Y Growth trend Analysis By Communication Technology

7.7. Absolute $ Opportunity Analysis By Communication Technology, 2025-2030

Chapter 8. Global Home Energy Management System Market– By End-User

8.1. Introduction/Key Findings

8.2. Single-Family Homes

8.3. Multi-Family Homes

8.4. Apartments

8.5. Villas

8.6. Y-O-Y Growth trend Analysis By End-User

8.7. Absolute $ Opportunity Analysis By End-User, 2025-2030

Chapter 9. Global Home Energy Management System Market– By Distribution Channel

9.1. Introduction/Key Findings

9.2. Direct Sales

9.3. Distributors

9.4. Online Retail

9.5. Y-O-Y Growth trend Analysis By Distribution Channel

9.6. Absolute $ Opportunity Analysis By Distribution Channel, 2025-2030

Chapter 10. Global Home Energy Management System Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product Type

10.1.3. By Communication Technology

10.1.4. By End-User

10.1.5. By Distribution Channel

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product Type

10.2.3. By Communication Technology

10.2.4. By End-User

10.2.5. By Distribution Channel

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product Type

10.3.3. By Communication Technology

10.3.4. By End-User

10.3.5. By Distribution Channel

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Product Type

10.4.3. By Communication Technology

10.4.4. By End-User

10.4.5. By Distribution Channel

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Product Type

10.5.3. By Communication Technology

10.5.4. By End-User

10.5.5. By Distribution Channel

10.5.6. By Region

Chapter 11. Global Home Energy Management System Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Honeywell International Inc. (US)

11.2. Nest Labs Inc. (US)

11.3. Vivint, Inc. (US)

11.4. General Electric Company (US)

11.5. Ecobee Inc (Canada)

11.6. Alarm.com (US)

11.7. Comcast Cable (US)

11.8. Panasonic Corporation (Japan)

11.9. Ecofactor Inc. (US)

11.10. Energyhub Inc. (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Home Energy Management System Market was valued at USD 3.80 billion in 2024 and is projected to reach a market size of USD 8.28 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.86%.

Main factors include growing energy prices, government incentives, smart-speaker proliferation, and integration with renewables.

Smart thermostats are visible, simple to operate, and provide actual bill-saving potential, therefore making them the dominant segment of the market.

The pandemic had a great impact on this market. Following an early decline, internet‑friendly sales and increased home occupancy quickened digital channel expansion.

Major obstacles for this market include data-privacy issues, legacy-home retrofitting complexity, high initial costs, and fragmented IoT standards.