Global Generative AI In Fintech Market Research Report – Segmentation By Component (Software, Services), By Deployment (On-premises, Cloud), By Application (Fraud Detection & Risk Management, Customer Services & Personalization, Algorithmic Trading & Portfolio Optimization, Credit Scoring & Underwriting, Others), By End-Users (Banks, Insurance Companies, Payment Providers, Trading Firms, RegTech Firms, Others), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16585

Format:

Region: Global

Market Size and Overview:

The Global Generative AI In Fintech Market was valued at USD 2.17 billion and is projected to reach a market size of USD 18.9 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 54.17%.

Able to produce authentic text, code, and synthetic data, generative AI allows financial organizations to automate credit decision-making, produce compliance reports, customize client interactions, and simulate sophisticated risk scenarios. The demand for extremely individualized services, the push for operational efficiency, and strict regulatory compliance are among the main drivers. Leading banks, insurance firms, and financial technology companies are working with AI providers to incorporate generative features into fundamental operations, hence altering the financial services scene.

Key Market Insights:

As institutions invest in licensing sophisticated generative engines and bespoke model training environments, the software sector, made up of AI models, development platforms, and integration toolkits, generated 61% of 2024 revenue.

By using scalable GPU instances and managed artificial intelligence services, cloud-based generative-AI deployments captured about 68% of the market, therefore allowing for quick experimentation and worldwide distribution without much on-premises investment.

As organizations try to anticipate complex threats and abide by Basel and FRTB criteria, the Fraud and Risk category drove to ~27% of market revenues in 2024, thanks in part to generative artificial intelligence for synthetic-data generation, anomaly detection, and automated scenario modeling.

Banks, including those in retail and business, accounted for roughly 35% of the generative-AI fintech market in 2024, deploying AI agents for personalized wealth-management advice, compliance-report creation, and loan underwriting.

Generative AI In Fintech Market Drivers:

The biggest advantage for this market is the cost reduction and operational efficiency that drives its growth.

Financial institutions usually assign 50–60% of their revenues to operating expenses, staffing, document processing, and regulatory reporting, which provides significant motivation for the automation of repetitive tasks. Through generative artificial intelligence-powered Intelligent Document Processing (IDP) solutions like those utilized by Canoe Intelligence, millions of KYC and loan documents are processed with 99.9% accuracy, lowering overhead expenses by up to 60% and decreasing manual review times by 70%. Beyond IDP, banks use AI-driven code refactoring tools to automatically update and optimize legacy application code, therefore cutting development cycles by 30%. Generative models combine account-opening paperwork and create credit memorandum narratives, functions formerly requiring specialized analysts, reducing the workload by 40–50% and allowing teams to concentrate on high-value advisory roles in corporate banking. Consequently, organizations claim 20 to 25% faster time-to-market for new loan products and compliance procedures.

The strict regulatory compliance and auditability are major market growth drivers.

Strict financial regulations, GDPR, CCPA, Basel III, and FRTB call for open, auditable procedures and quick reporting. Generative AI systems now include compliance-check modules that automatically prepare policy-aligned risk reports, simulate stress-test scenarios utilizing adversarial GAN frameworks, and, in real time, flag regulatory deviations. At major European banks, implementations show a 30% drop in compliance-preparation effort with AI-generated draft submissions encompassing detailed Basel and IFRS 9 disclosures previously consuming hundreds of analyst hours. Every model inference and data transformation is recorded in automated audit trails, therefore guaranteeing complete traceability for regulators. By integrating generative artificial intelligence into RegTech systems, companies may dynamically adjust to changing regulations, like EU AI Act proposals, hence lowering the risk of non-compliance fines, which could reach 4% of global turnover under GDPR.

The rising demand for hyper-personalized customer experience is a major market growth driver.

Modern customers anticipate financial services customized to their individual profiles and life events. Generative-AI–driven virtual assistants, implemented by top fintechs, combine LLMs with customer-data lakes to produce tailored investment recommendations, loan offers, and savings plans in natural language, raising Net Promoter Scores (NPS) 15–20%. In retail banking, AI-generated conversational interfaces handle complex inquiries, such as retirement planning scenarios, without human intervention, achieving first-contact resolution rates of 85%. Wealth-management platforms employ generative models to simulate portfolio adjustment narratives, allowing financial advisors to provide bespoke insights at scale. Institutions using these tailored generative-AI solutions thus register 25% more cross-sell rates and 30% more digital interactions per customer.

The recent innovations in portfolio management and trading are considered to be great market drivers.

Algorithmic trading desks are employing generative models to expand their strategic repertoire beyond past back-testing. Incorporating rare stress events, businesses employ GANs to create synthetic market situations and so improve risk-adjusted returns by 12 to 18% versus conventional Monte-Carlo simulations. Generative AI also automates the creation of trading algorithms: traders input high-level strategy themes (“momentum + mean reversion”) and receive code prototypes, therefore shortening development cycles by 50%. Portfolio managers use text-to-quant models to convert research reports and news articles into actionable trade signals, boosting alpha capture by 8–10%. These AI-driven innovations not only raise performance but also enable quick iteration on novel tactics, therefore offering a competitive advantage in unstable markets.

Generative AI In Fintech Market Restraints and Challenges:

The existence of model bias and issues regarding data quality are major drawbacks for this market.

Generative artificial intelligence's outputs are only as trustworthy as the data on which they are trained; so, high-quality, representative datasets are vital, yet in financial services data often resides in silos across loan-origination systems, trading logs, and customer–relationship databases. Biased or incomplete training data can embed unfair scoring, such as disadvantaging minority applicants in credit decisions, or produce synthetic scenarios that fail to capture real‐world risk correlations, leading to regulatory non‐compliance and flawed risk assessments. Ensuring data lineage and provenance across these diverse sources requires robust data‐governance frameworks and metadata catalogs, yet many institutions still lack automated tools for traceability. Continuous validation, comparing model outputs against live production data, is critical to detect drift and bias over time, but it is resource‐intensive, demanding dedicated data-engineering and compliance teams. Without these safeguards, banks risk deploying generative models that propagate systemic biases, destroy stakeholder trust, and trigger regulatory scrutiny under frameworks like the EU AI Act and U.S. fair lending laws.

The issue related to trusting the system and its explainability is a major challenge for this market.

Large language and diffusion models function as "black boxes," producing output via complicated, dispersed neural network layers that resist simple explanation. This transparency clashes with financial-regulation requirements, such as the ECB's expectations for model governance and the “right to explanation” under GDPR, mandating institutions to show how decisions driven by artificial intelligence are created. Banks are funding explainable artificial intelligence (XAI) toolkits to help bridge this gap; these systems use methods like SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations), which follow contributions of input features to model results. Embedding these governance levels raises operating and development costs noticeably, therefore delaying project timelines by 20–30% and needing specialized personnel to analyze and offer justifications to risk committees and auditors. Particularly when automated credit decisions or portfolio‐recommendation engines produce unexpected results, financial institutions without strong XAI systems expose themselves to regulatory sanctions, reputational damage, and customer distrust.

The integration of this technology with the existing system is difficult, which slows down its operations.

Many banks and insurers still depend on core banking systems and policies created decades ago—monolithic, batch-oriented, and incompatible with real-time, API-driven generative-AI microservices. Bridging these legacy systems requires great middleware layers, unique connectors, and data-orchestration pipelines, usually increasing integration costs by 20–30% and extending implementation timescales by months. Data-model mismatches, erratic customer identifiers, and strict ETL procedures all add to the difficulties smooth data flow faces, therefore causing synchronization delays and perhaps inconsistencies. Institutions are implementing API-led architectures and data fabric platforms that abstract underlying systems and offer centralized, real-time data access to lessen these obstacles. Creating and running these contemporary integration layers, however, requires cross-disciplinary knowledge in cloud-native data architectures as well as legacy technologies, resources that continue to be in short supply and demand premium prices.

The huge skill gap and shortage of a talented workforce slow down the working of market.

The rise in generative-AI projects has increased competition for data scientists with deep technical expertise in transformers and domain knowledge in financial services. Business Insider's "AI Talent Wars" suggests that only 1,000 or so scientists globally have the sophisticated expertise to create and refine massive language models; top candidates command offers in the seven- to nine-figure range and base pay of more than USD 200,000. This dearth of talent results in extended recruiting cycles, 4 to 6 months on average, and high contractor fees, which add 30–40% to the budget of a project. Many businesses cooperate with AI service providers or use off-the-shelf managed AI platforms to close the gap; however, these methods can restrict customization and produce vendor dependencies. Banks run the danger of slowing down generative-AI projects and giving fintech competitors with more nimble resourcing models a competitive edge in the absence of sustainable talent development plans, like in-house artificial intelligence academies and university collaborations.

Generative AI In Fintech Market Opportunities:

The use of embedded Generative AI in the core banking platform increases their efficiency.

NatWest's partnership with OpenAI, for instance, improved its Cora chatbot and staff assistant AskArchie, thereby increasing consumer happiness by 150% and lowering advisor burden by automating account security checks and fraud-flagging processes. Similarly, companies like Temenos and Finacle, global core-banking suppliers, are including AI agents for customer-centric virtual assistants, real-time risk-monitoring dashboards, and automatic compliance-report generation. These SaaS add-ons enable new revenue streams through subscription or transaction-based fees and speed banks' time-to-market for digital services by as much as 40%, all the while maintaining tight integration with current account-management and payment-processing systems.

The recent use of synthetic-date-as-a-service is opening up new opportunities for this market.

Financial organizations more and more using synthetic data systems to produce realistic, GDPR-compliant datasets for artificial intelligence model training and software testing as privacy rules get stricter. Driven by demand for secure data sharing and strong stress-testing environments, the worldwide synthetic-data-generation market is predicted to expand from USD 292.0 million in 2024 to USD 1,788.1 million by 2030, a 35.3% CAGR, on the back of demand for secure data sharing and strong stress-testing environments. Leading providers (e.g., MOSTLY AI, Hazy Limited) offer high-fidelity transaction logs, customer-profile repositories, and micro-segmentation tools that preserve statistical properties without exposing personal information. Banks deploy these platforms to augment credit-scoring datasets, simulate rare fraud scenarios, and validate AI risk models, cutting the time for safe data access from months to hours while maintaining full audit trails.

The SMEs and Challenger-Bank Solutions are rapidly adopting Generative AI, which is helping this market to expand.

Unencumbered by inherited infrastructure, digital-only challenger banks and fintech startups are quickly adopting generative AI to provide full end-to-end services for underserved SMEs. UK challenger Allica Bank incorporates AI-driven credit-scoring systems into its SME loan platform, lowering application-to-decision times to less than 24 hours and supposedly enabling 55% year-over-year AUM expansion. Digital lenders like Kissht in India use AI agents to execute real-time cash-flow analysis and automated documentation, therefore granting quick credit approvals for micro-enterprises with little documentation. These AI-enabled workflows let challengers provide distinct, rapid-response banking experiences, thus gaining market share from incumbents and addressing gaps in conventional SME lending.

The emergence of RegTech and Audit-Automation Platforms is seen as a major market opportunity.

Automating the drafting of audit summaries, regulatory filings, and stress-test reports, generative artificial intelligence is changing regulatory compliance. Valued at USD 1.89 billion in 2024, the artificial intelligence in the RegTech market is expected to hit USD 9.11 billion by 2029, a 37.0% CAGR, as financial institutions attempt to streamline compliance and shorten manual review cycles. Platforms such as ComplyAdvantage and Ayasdi use LLMs to create policy-aligned reports, map regulatory changes to internal controls, and simulate "what-if" scenarios for Basel FRTB and Dodd-Frank stress tests. These AI-driven RegTech solutions help companies avoid fines, possibly up to 4% of worldwide turnover, and free compliance teams to focus on strategic risk management by reducing compliance preparation time by 30% and improving documentation accuracy.

Generative AI In Fintech Market Segmentation:

Market Segmentation: By Component

• Software

• Services

The Software segment is said to dominate this market. Financial institutions mostly invest in generative‐AI engines, model‐training frameworks, and integration toolkits, licensing these core software components to infuse AI across their businesses. These have around a 61% market share in 2024. The Services segment is the fastest-growing segment, Services (nearly 38% CAGR, 2025–2030). Demand for professional and managed services is rising as businesses need customized model fine-tuning, MLOps consulting, and managed-AI operations and lack in-house AI expertise.

Market Segmentation: By Deployment

• On-premises

• Cloud

The Cloud segment is the dominant segment of the market. Through deployment, cloud deployments, which use hyperscale GPU clusters and managed artificial intelligence services, enable quick prototyping, cost-effective scaling, and worldwide launch without significant financial commitment. Cloud holds around 68% market share. The On-premises segment is the fastest-growing segment. Highly regulated banks and insurers with strict data sovereignty and audit requirements are increasingly deploying generative-AI microservices behind their firewalls.

Market Segmentation: By Application

• Fraud Detection & Risk Management

• Customer Services & Personalization

• Algorithmic Trading & Portfolio Optimization

• Credit Scoring & Underwriting

• Others

The Fraud Detection & Risk Management segment dominates this market. Generative models create real transaction data for anomaly detection and scenario modeling, thereby allowing businesses to get ahead of complex financial crime. Share of around 27%. The Customer Services & Personalization segment is the fastest-growing segment. Customer Service and Personalization (around 36% CAGR) – AI-powered chatbots, virtual assistants, and dynamic offer generators are quickly embraced to provide hyper-personalized experiences, hence enhancing customer retention and satisfaction.

AI-driven strategy simulations and synthetic market situations enhance risk-adjusted returns by 12–18% in the Algorithmic Trading and Portfolio Optimizing segment. Under the Credit Scoring & Underwriting segment, generative artificial intelligence produces synthetic credit profiles and improves decision openness, therefore lowering default rates by up to 20%. The Others segment of the market includes back-office automation and artificial intelligence-driven drafting of compliance reports.

Market Segmentation: By End-Users

• Banks

• Insurance Companies

• Payment Providers

• Trading Firms

• RegTech Firms

• Others

The Banks segment is said to dominate this market. Banks (~35% share) use generative artificial intelligence for loan underwriting, compliance-report auto-generation, and virtual wealth advisors across both retail and corporate banking departments. The RegTech Firms segment is the fastest-growing one, as these companies use generative artificial intelligence to automate audit narratives, risk assessments, and regulatory submissions, therefore driving remarkable expansion as regulatory complexity increases.

The insurance companies include AI-created risk models and the drafting of claims paperwork. For the Payment Providers segment, it has around a 12% market share. This segment includes anti-fraud synthetic data and conversational bots. When it comes to the Trading Firms segment, Trading Companies, with about 14% market share, include strategy back-testing and scenario generation. Other people (around 21%) comprise corporate-treasury systems, mortgage fintech, and wealth management.

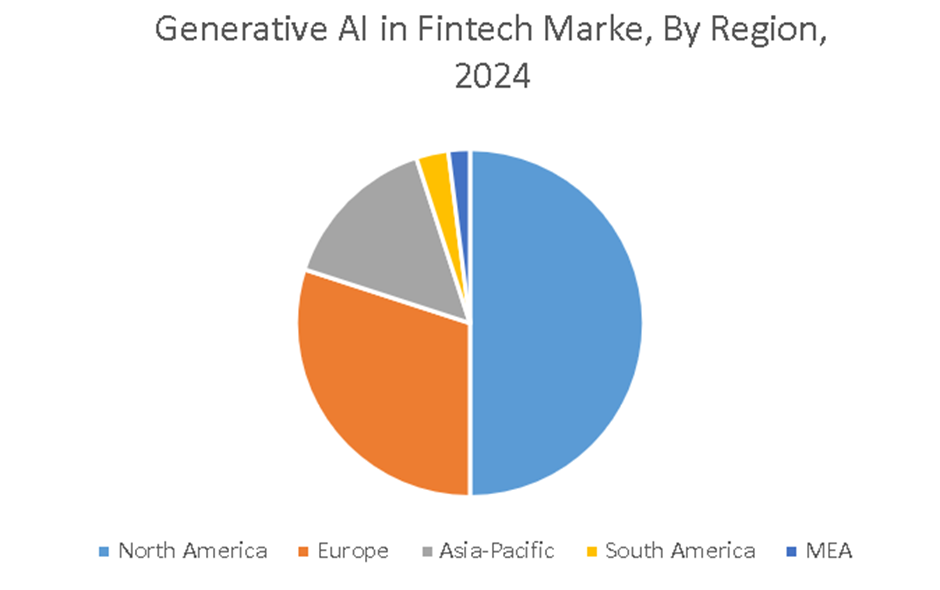

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America leads this market, and the Asia-Pacific region is the fastest-growing region. North America, home to prominent fintech centers and leading research in artificial intelligence, benefits from extensive hyperscaler assistance and substantial corporate spending on deep enterprise AI. Asia Pacific's fast digital‐banking adoption, India's fintech penetration, and China's digital‐finance requirements are driving the fastest regional growth.

Europe is defined by robust digital banking infrastructure and strong artificial intelligence governance. Both South America and the MEA regions are considered emerging markets due to Fintech innovation in Mexico and Brazil, Digital transformation in the oil and gas sector, and smart-city funding initiatives.

COVID-19 Impact Analysis on the Global Generative AI In Fintech Market:

The epidemic highlighted the necessity of financially remote-capable services and automation. Banks accelerated AI pilots by 50% in 2020–2021, concentrating on automated document processing and virtual assistants to handle branch closures and staffing restrictions. Specifically, generative artificial intelligence saw pilot projects in loan origination and customer-service bots increase by 65% as institutions sought to maintain service levels without physical branches. Though initially focused on emergency response, 80% of these pilots have moved to production, anchoring generative-AI investments as a strategic pillar for operational resilience and digital-first consumer engagement.

Latest Trends/ Developments:

Fusion of text, voice, and image creation for more meaningful customer interactions and safe identification confirmation.

Improving anti-money-laundering networks by means of privacy-preserving, cross-institutional model training without crude data exchange.

Regulators (such as the UK's FCA) are starting generative-AI labs to co-innovate compliant applications with fintechs.

Providers of financial cloud services are giving selected curated generative AI model catalogs to help quickly integrate with current financial technology systems.

Key Players:

• Open AI

• Microsoft Corporation

• Google LLC

• Genie AI Ltd.

• IBM Corporation

• MOSTLY AI Inc.

• Veesual AI

• Adobe Inc.

• Synthesis AI

• Salesforce

Chapter 1. Global Generative AI In Fintech Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Generative AI In Fintech Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Generative AI In Fintech Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Generative AI In Fintech Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Generative AI In Fintech Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Generative AI In Fintech Market- By Component

6.1. Introduction/Key Findings

6.2. Software

6.3. Services

6.4. Y-O-Y Growth trend Analysis By Component

6.5. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Generative AI In Fintech Market– By Deployment

7.1 Introduction/Key Findings

7.2. On-premises

7.3. Cloud

7.4. Y-O-Y Growth trend Analysis By Deployment

7.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 8. Global Generative AI In Fintech Market– By Application

8.1. Introduction/Key Findings

8.2. Fraud Detection & Risk Management

8.3. Customer Services & Personalization

8.4. Algorithmic Trading & Portfolio Optimization

8.5. Credit Scoring & Underwriting

8.6. Others

8.7. Y-O-Y Growth trend Analysis By Application

8.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 9. Global Generative AI In Fintech Market– By End-Users

9.1. Introduction/Key Findings

9.2. Banks

9.3. Insurance Companies

9.4. Payment Providers

9.5. Trading Firms

9.6. RegTech Firms

9.7. Others

9.8. Y-O-Y Growth trend Analysis By End-Users

9.9. Absolute $ Opportunity Analysis By End-Users, 2025-2030

Chapter 10. Global Generative AI In Fintech Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Deployment

10.1.4. By Application

10.1.5. By End-Users

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Deployment

10.2.4. By Application

10.2.5. By End-Users

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Deployment

10.3.4. By Application

10.3.5. By End-Users

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Deployment

10.4.4. By Application

10.4.5. By End-Users

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Deployment

10.5.4. By Application

10.5.5. By End-Users

10.5.6. By Region

Chapter 11. Global Generative AI In Fintech Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Open AI

11.2. Microsoft Corporation

11.3. Google LLC

11.4. Genie AI Ltd.

11.5. IBM Corporation

11.6. MOSTLY AI Inc.

11.7. Veesual AI

11.8. Adobe Inc.

11.9. Synthesis AI

11.10. Salesforce

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Generative AI In Fintech Market was valued at USD 2.17 billion and is projected to reach a market size of USD 18.9 billion by the end of 2030 with a CAGR of 54.17%.

The Fraud Detection & Risk Management segment is said to be the dominant one for this market due to regulatory pressure and a rise in financial crimes.

With 80% shifting to production post-pandemic, branch closures and personnel restrictions fueled a 65% increase in generative-AI pilots for document Automation and virtual assistants.

Buoyed by China's digital-finance mandates and India's fintech innovation centers, the Asia-Pacific is the fastest-growing region.

Explainability of artificial intelligence models, data privacy/regulatory compliance, integration with legacy banking systems, and the paucity of trained AI personnel.