Global FinTech Lending Market Research Report – Segmentation By Technology (AI & ML, Big Data Analytics, Blockchain, Mobile Platforms, Cloud), By Lending Type (Consumer Loans, SME Loan, Mortgage Loan, Student Loan, Others), By Deployment Mode (Cloud-based, On-premises), By Organization Size (SMEs, Large Enterprises), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16580

Format:

Region: Global

Market Size and Overview:

The Global FinTech Lending Market was valued at USD 400 billion and is projected to reach a market size of USD 800 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.87%.

Digital transformation in financial services, growing demand for alternative credit options among underbanked individuals and SMEs, and the multiplication of AI- and data-driven underwriting systems that simplify loan origination, payment, and risk management fuel this fast growth. Using real-time data sources like mobile-device signals and alternative payment histories, fintech lenders extend credit more inclusively and across geographies.

Key Market Insights:

Small companies searching for quick, collateral-light finance to manage cash flow have led to SME loans totaling around 42% of all FinTech lending volume in 2024. Driving 30% year-over-year growth in SME loan issuance, FinTech platforms reduce approval times from weeks to hours.

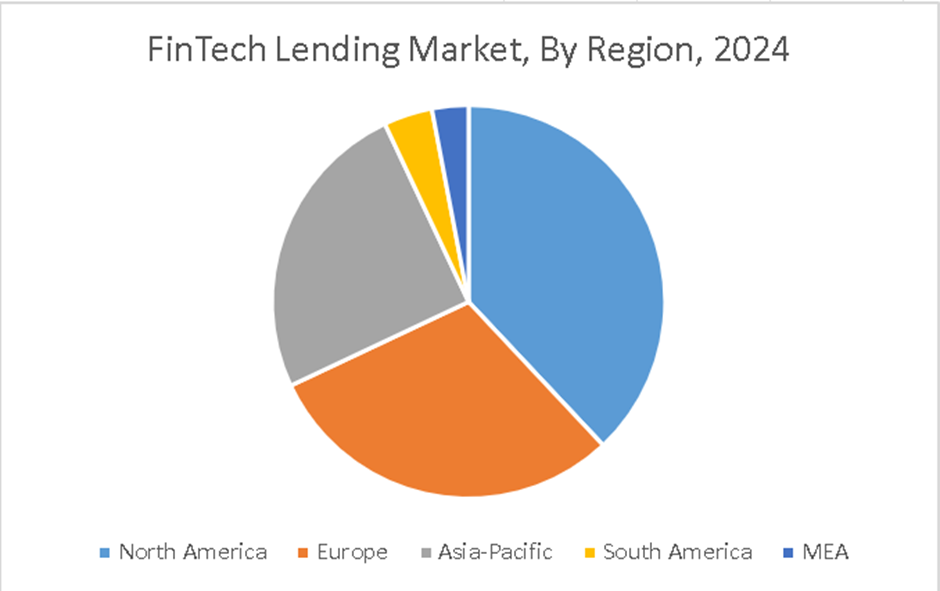

Led worldwide in 2024 with roughly 36% market share, Asia Pacific is projected to grow at 18% CAGR through 2030, driven by e-commerce credit in China and digital micro-lending in India and Southeast Asia.

Lenders automating decision-making and compliance checks, platforms employing AI/ML for credit scoring and fraud detection, lowered non-performing loan ratios by 20% on average, accounting for about 28% of technology spend in 2024.

Capturing about 30% of retail-loan volumes, consumer personal loans made through FinTech increased by 25% in 2024 as digital-first borrowers adopted mobile applications and instant disbursal.

FinTech Lending Market Drivers:

The underbanked population and credit inclusion are major market growth drivers.

Including utility payments, mobile-phone top-ups, and e-commerce purchase histories among other data sources, digital lenders create credit profiles for thin-file consumers, therefore unlocking an estimated USD 500 billion in unutilized loan volume by 2030. Mobile-money systems in Africa have allowed immediate microloans to rural customers, therefore helping half of the 700 million worldwide mobile-money users obtain access to credit for the first time. Likewise, alternative-data scoring in India extends working-capital lines to small merchants, hence, 15% decreasing NPL rates contrast with conventional underwriters. FinTech lending is turning out to be a strong driver for financial inclusion and economic resilience as authorities and NGOs push digital financial literacy and supportive systems.

The market offers speed and convenience, which is a great market growth driver.

Unlike 2–4 weeks for traditional banks, digital-first lending services compress the end-to-end loan process, from application to disbursal, under 24 hours. Identity validation is expedited by automated KYC/AML checks using document-verification APIs and biometric e-signatures; real-time fraud analytics engines block dubious transactions immediately. Driven by simple mobile applications and clear charge arrangements, borrower-experience indicators demonstrate satisfaction scores for FinTech lenders 20% higher. Micro-loan applications grew 300% in use throughout peak agricultural season as farmers quickly obtained cash using cell phones. This speedy service not only helps to improve portfolio performance by lowering application abandonment and allowing dynamic risk-based pricing, but also strengthens customer loyalty.

The use of Open AI and Regulatory Sandbox is driving the rapid growth of this market.

Regulatory sandboxes have been created in jurisdictions such as the U.K., Singapore, and the UAE, whereby FinTech startups may pilot creative lending products under limited control, hence reducing time-to-market by 30%. Simultaneously, open-banking rules (PSD2 in the EU; U.K. Open Banking) compel banks to reveal customer-consented data through standardized APIs, therefore allowing FinTech lenders to access transaction histories and carry out instant affordability evaluations, free from manual bank statements. By means of live-sandbox pilots in Abu Dhabi and Hong Kong, insights that inform scalable frameworks are produced to guarantee that compliance, consumer protection, and innovation progress in tandem with this API-driven data access, reducing underwriting costs by 25%, whilst increasing credit-decision accuracy.

The existence of cost-effective infrastructure is beneficial for the market, promoting its growth.

By using pay-as-you-go compute and storage, cloud-based lending platforms eliminate costly hardware refresh cycles and provide 30% lower infrastructure costs than on-premises solutions. Lenders match IT expenditure with loan-volume variations by auto-scaling resources during marketing campaigns and credit-peak seasons, such as holiday spending, thereby preserving capital for customer acquisition and underwriting. Further lowering idle-resource costs, serverless architectures and managed database services aid compliance with data-residency regulations. Smaller FinTechs competing with established banks on feature parity and pricing help to stimulate a tide of new entrants that lowers loan-processing costs for SMEs and consumers both.

FinTech Lending Market Restraints and Challenges:

The high risk of credit default and fraud poses a huge challenge for the market.

The quick scaling of digital lending platforms frequently overtakes the maturity of credit-risk models, which results in high default rates, especially in unsecured SME sectors where global average defaults hover around 6%. FinTechs targeting developing markets might rely heavily on alternative data underwriting, but sudden economic shocks, like rising inflation or industry declines, can make predictive models less accurate. To lessen losses, lenders need to keep strengthened capital buffers, frequently 15 to 20% higher than regulatory minima, and use dynamic provisioning that modifies reserves near real time based on portfolio performance cues. Among advanced risk methods are portfolio division according to risk tier, machine-learning-driven stress testing, and automated collection procedures meant to maximize contact approaches by borrower segment. But these complex structures raise operational difficulty and demand continuous model governance, validation, and regulatory consent, thereby straining compliance and data-science resources in quick-growth FinTech businesses.

The risk related to the privacy and security of data is a great market challenge faced by this market.

Because they handle very sensitive biometric, financial, and personal information, FinTech lenders are clearly in the crosshairs of regulatory examination and cyberattacks. Noncompliance under GDPR and CCPA may draw penalties up to 4 % of worldwide turnover or USD 7.5 million, respectively; APAC countries are enacting similar tough data-sovereignty regulations requiring local storage and processing. FinTechs typically dedicate 10–15 percent of their IT budgets to managed security service providers and cybersecurity tools. Building a zero-trust architecture, where every request is authenticated and authorized, further strengthens defenses but increases latency and tooling overhead. Maintaining thorough data-provenance logs and consent-management systems to examine data use adds to integration and operational costs as consumers demand transparency; hence, businesses should also do this.

The uncertainty that exists in the rules and regulations hampers market growth and development.

FinTech lenders traverse a maze of changing rules from usury laws and interest-rate caps to consumer-protection systems and AML/KYC requirements, which vary greatly by country and region. India's digital-lending rules, for example, call for clear disclosure of loan expenses and set maximum processing fees; Brazil's Central Bank limits charge structures for microloans. This patchwork forces FinTechs to create modular compliance engines able to enforce area-specific regulations, therefore raising development and operational expenditures by up to 15% of all budgets. Additionally, harming product economics and profitability are regulatory moratoria or abrupt policy changes, including temporary rate-cap suspensions. Active interaction with regulators using sandboxes and industry groups helps to produce sensible standards, but it calls for committed legal and government-affairs teams, thus further limiting corporate resources in a quickly expanding market.

The market faces great competition from banks all over the world, affecting its growth potential.

Using low funding costs, deep customer relationships, and wide branch networks, traditional banks are increasing their digital-lending capabilities to regain market share from nimble FinTech companies. Leading international banks are registering 25–30 % yearly growth in digital-loan volumes, utilizing their current deposits to provide competitive unsecured loans and simplified onboarding via their mobile applications. Banks can also cross-sell lending solutions inside bundled checking or credit-card suites, therefore putting pricing pressure on independent FinTechs. FinTech lenders must stand out via specialized markets (e.g., industry-specific SME loans), better user experiences, or quicker approvals to be competitive. To access institutional distribution while maintaining technology leadership, they could also seek strategic alliances, white-label agreements, or bank incubator initiatives. Still, bank rivalry has shrunk FinTech profits, therefore pushing cost reduction and creativity to keep pace with growth paths in a declining market.

FinTech Lending Market Opportunities:

The use of embedded lending in E-commerce is seen as a major market growth opportunity.

Embedding credit at the point of sale transforms the checkout experience and lifts key performance metrics for online merchants. Capturing a significant portion of the USD 200 billion in additional loans projected for e-commerce platforms, McKinsey projects that embedded lending will grow from around 5% of retail and SMB lending today to 25% by 2030. Retailers partnering with FinTech lenders integrate seamless "Buy Now, Pay Later" (BNPL) and digital installment choices via APIs, so reducing cart abandonment and increasing average order values by 15% while growing conversion rates by 10–20%. These embedded solutions leverage real-time risk assessments and alternative-data credit scoring, allowing near-instant credit decisions without sending customers to external sites. The line between business and finance blurs as marketplaces from Amazon to Shopify open their ecosystems to outside lenders, hence presenting fresh revenue-share and loyalty possibilities for both businesses and lending partners.

The rise of SME Ecosystem Finance is presenting a good market development opportunity.

Rising numbers of small and mid-sized companies look to integrated financial-management packages that include borrowing with core business apps, including accounting, invoicing, and payroll, into a single platform. Driven by digital platforms such as QuickBooks Capital and Xero's partner lending network, the SME ecosystem-finance market is forecast to reach USD 150 billion in annual originations by 2030. These solutions lower time to funding to under 24 hours, increase cash-flow clarity, and automate repayment through invoice matching by integrating working-capital loans right inside billing processes. Working with payment providers and ERP vendors, FinTechs show credit offers contextually, for instance, pre-approved lines are shown when merchants produce huge invoices, hence increasing take-up rates by 30 % above standalone loan requests. By spreading into several contact points within a small to medium-sized firm's lifecycle, this integrated approach improves customer relationships, reduces customer acquisition expenses, and lowers lender concentration risk.

The use of sustainable lending products is helping this market to grow at a faster rate.

Emerging as a fast-expanding area within FinTech lending, green and sustainability-connected products satisfy corporate and consumer needs for ESG-aligned finance. Driven in part by green bonds and sustainability-linked loans, the sustainable finance market will grow from USD 5.87 trillion in 2024 to over USD 23.99 trillion by 2032 at a 21.45 % CAGR. FinTech lenders like Firstmac have pioneered discounted "green loans" for electric-vehicle purchases and energy-efficient home improvements, offering rate reductions of 0.5–1.0 percent for verifiable emissions-saving projects. Corporations now use ESG-linked credit lines, where interest rates vary according to sustainability indicators, opening capital, and meeting stakeholder expectations. FinTech platforms are including automated data-collection for carbon footprints and project results as legislators and investors ask for strict impact reporting, therefore streamlining compliance and allowing for quick scaling of green-finance portfolios at a premium of 10–15 bps over vanilla loans.

The emergence of cross-border and remittance loans is seen as a massive market growth opportunity.

According to migration-finance studies, startups like Tala and Branch are tapping a USD 24.5 billion digital-remittance market set to increase at 16.7% CAGR by 2030 by providing microloans in regions like Asia, Africa, and Latin America, where remittance-linked loans assist in leveling consumption across payday cycles. These platforms combine FX-hedged wallets and immediate disbursal, allowing borrowers to access USD 50 billion in new credit volumes by 2030. Lenders can evaluate creditworthiness based on stable cash flows and provide cheap loans (sub-3 percent) by connecting credit offers to incoming remittances. Alliances with mobile-money providers and decentralized finance networks will next lower transfer costs and processing times, hence promoting more financial inclusion and producing integrated remittance-plus-credit ecosystems throughout developing nations.

FinTech Lending Market Segmentation:

Market Segmentation: By Technology

• AI & ML

• Big Data Analytics

• Blockchain

• Mobile Platforms

• Cloud

The Mobile Platforms segment dominates this market. Mobile Platforms as smartphone penetration and app-based lending direct loan origination channels. Mobile-first lending applications push consumer and micro-loan adoption, holding around 32% of technology spend owing to the ubiquity of smartphones and fast disbursal needs. The Blockchain segment is said to be the fastest-growing segment. Driven by DeFi inventions and tokenized lending models, Blockchain is the fastest-growing. Enables decentralized ledgers for smart-contract distributions, peer-to-peer lending, and collateral tracking. Though still undeveloped at roughly 8% share, blockchain is the fastest-growing technology sector (approximately 30% CAGR) as DeFi models take off.

AI & ML segment powers automated credit scoring, fraud detection, and dynamic pricing models. AI/ML platforms accounted for roughly 28% of fintech-lending tech expenditure in 2024, as lenders use predictive analytics to lower defaults and maximize portfolios. The Big Data segment informs underwriting and risk management by aggregation of alternative data (e.g., utility payments, social signals). Representing around 22% of technological spending, big data solutions allowed real-time monitoring and portfolio insights. Favored for cost-effective elasticity, cloud installations accounted for almost 10% of tech spending and support scalable, on-demand infrastructure for loan origination and servicing.

Market Segmentation: By Lending Type

• Consumer Loans

• SME Loan

• Mortgage Loan

• Student Loan

• Others

The SME Loan leads this market. With around 42% market share, small-business funding leads as an alternative underwriter that provides fast, collateral-light credit lines for underserved SMEs. The Student Loan segment is the fastest-growing segment. Student Loans as a fintech approach to increasing tuition expenses and innovative repayment plans. Growth in student lending is driven by ed-tech alliances and income-share arrangements; now about 5% of volume, but growing at roughly 24% CAGR.

Consumer Loans include loans related to auto and personal loans, it have a 30% market share, which is due to instant approval and zero paperwork. The Mortgage segment accounts for around 12% market share. It is modernizing the home-loan application and appraisal process by using e-signatures. The Others segment comprises the remaining around 11%, other sectors include invoice financing, equipment leasing, and micro-loans.

Market Segmentation: By Deployment Mode

• Cloud-based

• On-premises

The Cloud-based segment is both the dominant and the fastest-growing segment. For its flexibility, cheaper initial expenditures, and quicker time-to-market, the cloud-based is said to be the dominant one. For loan-origination systems, the main model at roughly 75% share provides pay-as-you-go scalability and quick feature launches. Driven by constant movement to SaaS and PaaS lending systems, cloud-based continues to overtake on-premises segment. The On-premises segment, accounting for around 25%, is favored by major financial institutions needing total control over compliance and data.

Market Segmentation: By Organization Size

• SMEs

• Large Enterprises

The SMEs segment dominates this market. SMEs, reflecting the large, underappreciated small-business sector, dominate. Accessible, off-the-shelf lending solutions and digital onboarding account for the fastest-growing sector, at around 20% CAGR. Utilizing ready-made digital platforms to handle borrowing without significant IT staff or collateral, fintech-lending consumers comprise around 55%. The Large Enterprise segment is said to be the fastest-growing segment, this is because of the deployment of high-volume lending solutions with the existing banking infrastructure.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America leads this market. Driven by a robust presence of fintech lending platforms, great consumer acceptability of digital lending solutions, and major venture capital investments in creative lending technologies. The Asia-Pacific region is said to be the fastest-growing region, driven by the rise of mobile banking, rising internet penetration, and a rising number of businesses in nations such as China and India that are adopting fintech lending solutions.

The European market consists of regulatory systems that encourage fintech innovation to support growth, therefore increasing demand for alternative lending options and emphasizing the improvement of customer experiences via technology. South America and the MEA regions are the emerging markets. Driven by a need for financial inclusion and access to credit for underprivileged groups, digital lending solutions will propel emerging markets with possible growth as they become more widely adopted. MEA has a small market size, but growing interest in fintech lending solutions as companies and customers search for quick access to financing and better banking services.

COVID-19 Impact Analysis on the Global FinTech Lending Market:

As SMEs and consumers battled cash flow problems and social distancing requirements, FinTech lending accelerated during the pandemic. Digital loan origination surged 45% in 2020, driven by instant-approval products and government-backed aid programs dispensed through FinTech platforms. Remote KYC and e-signature features allowed continuous credit access, thereby confirming digital lending as a vital channel that has retained 25% more involvement post-pandemic.

Latest Trends/ Developments:

BNPL had a worldwide transaction value of USD 170 billion in 2024, with collaborations spanning retail, travel, and healthcare.

Modular API stacks for credit-as-a-service from LendTech startups allow a 60% faster go-live.

Lenders include sustainability KPIs into loan pricing to reward borrowers reaching carbon reduction targets.

AI voice assistants make loan applications and account management easier, therefore increasing access for underbanked communities.

Key Players:

• Braviant Holdings

• RateSetter

• Kabbage Funding

• Avant LLC

• Tavant

• Fundbox

• OnDeck

• Social Finance Inc.

• Funding Circle

• LendingClub Bank

Chapter 1. Global FinTech Lending Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global FinTech Lending Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global FinTech Lending Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global FinTech Lending Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global FinTech Lending Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global FinTech Lending Market- By Technology

6.1. Introduction/Key Findings

6.2. Blockchain

6.3. Artificial Intelligence & Machine Learning

6.4. Big Data Analytics

6.5. Mobile Platforms

6.6. Cloud

6.7. Y-O-Y Growth trend Analysis By Technology

6.8. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 7. Global FinTech Lending Market– By Lending Type

7.1 Introduction/Key Findings

7.2. Consumer Loans

7.3. SME Loan

7.4. Mortgage Loan

7.5. Student Loan

7.6. Others

7.7. Y-O-Y Growth trend Analysis By Lending Type

7.8. Absolute $ Opportunity Analysis By Lending Type, 2025-2030

Chapter 8. Global FinTech Lending Market– By Deployment Mode

8.1. Introduction/Key Findings

8.2. Cloud-based

8.3. On-premises

8.4. Y-O-Y Growth trend Analysis By Deployment Mode

8.5. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 9. Global FinTech Lending Market– By Organization Size

9.1. Introduction/Key Findings

9.2. SMEs

9.3. Large Enterprises

9.4. Y-O-Y Growth trend Analysis By Organization Size

9.5. Absolute $ Opportunity Analysis By Organization Size, 2025-2030

Chapter 10. Global FinTech Lending Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Technology

10.1.3. By Lending Type

10.1.4. By Deployment Mode

10.1.5. By Organization Size

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Technology

10.2.3. By Lending Type

10.2.4. By Deployment Mode

10.2.5. By Organization Size

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Technology

10.3.3. By Lending Type

10.3.4. By Deployment Mode

10.3.5. By Organization Size

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Technology

10.4.3. By Lending Type

10.4.4. By Deployment Mode

10.4.5. By Organization Size

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Technology

10.5.3. By Lending Type

10.5.4. By Deployment Mode

10.5.5. By Organization Size

10.5.6. By Region

Chapter 11. Global FinTech Lending Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Braviant Holdings

11.2. RateSetter

11.3. Kabbage Funding

11.4. Avant LLC

11.5. Tavant

11.6. Fundbox

11.7. OnDeck

11.8. Social Finance Inc.

11.9. Funding Circle

11.10. LendingClub Bank

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The factors that are driving the growth of this market are rapid adoption of digitalization, demand for underbanked credit, and AI-driven underwriting.

Small businesses wanting rapid, collateral-light finance drive SME loans, which account for almost 42% of volume.

Given the extensive smartphone penetration, mobile lending solutions drive usage and account for 30% of technology expenditure.

For relief funding, the epidemic caused a 45% increase in digital loan originations, hence confirming distant, quick-approval channels.

Driven by mobile micro-lending and digital remittances, the Asia-Pacific region is the fastest-growing area at around 20% CAGR.