Global Fintech Cloud Market Research Report – Segmentation by Service Type (Cloud-Based Banking, Cloud-Based Insurance, Cloud-Based Lending, Cloud-Based Wealth Management, Cloud-Based Payment); By Deployment (Public, Private, Hybrid); By Enterprise (Large Enterprise, SMEs); By Application (Back-end Operations, Customer Experiences, Regulatory Compliance, Data Analysis, Risk Management); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16579

Format:

Region: Global

Market Size and Overview:

The Global Fintech Cloud Market was valued at USD 37.7 billion in 2024 and is projected to reach a market size of USD 80.56 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.4%.

The Fintech Cloud Market represents a transformative shift in how financial services are developed, delivered, and consumed, leveraging cloud computing to enhance agility, scalability, and innovation. By integrating cloud infrastructure into core financial operations, fintech companies and traditional institutions alike can reduce IT costs, accelerate product deployment, and improve customer experiences through real-time data processing and automation. This market is driven by increasing digital adoption, the need for regulatory compliance, and rising demand for secure, flexible solutions that support services such as digital payments, online lending, robo-advisory, and blockchain. As financial institutions continue their cloud migration journey, the fintech cloud ecosystem is evolving rapidly to meet the complex needs of a modern, data-driven financial landscape.

Key Market Insights:

The Fintech Cloud Market is witnessing rapid growth due to the rising reliance on digital financial services and the rising need for scalable infrastructure. Over 70% of financial institutions globally have either migrated to the cloud or are in the process, reflecting the growing trust in cloud-based systems for security, efficiency, and compliance. The integration of cloud solutions has enabled fintech firms to enhance user experiences while reducing time-to-market for new products.

Cloud adoption in fintech is particularly strong in areas like digital banking, payment processing, and fraud detection. Approximately 65% of fintech firms now utilize cloud-based AI and machine learning tools to improve customer insights and automate financial decision-making. This trend is creating more personalized and secure services for users, contributing to improved engagement and retention.

Regionally, North America continues to lead in cloud fintech adoption, fueled by a mature financial ecosystem and strong regulatory frameworks. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, with cloud-first fintech startups and increasing mobile payment usage. This global expansion is fueling a dynamic and competitive environment for cloud service providers catering to financial enterprises.

Fintech Cloud Market Drivers:

Surging Demand for Scalable and Flexible Infrastructure Drives Fintech Cloud Adoption

One of the key drivers of the Fintech Cloud Market is the increasing demand for scalable and flexible infrastructure that allows financial institutions to innovate rapidly and operate efficiently. Traditional banking systems are often rigid and costly to upgrade, but cloud solutions provide a dynamic environment where fintech companies can scale their operations up or down based on demand. This scalability supports fast-paced product development cycles and enables firms to respond to evolving customer expectations and market trends more effectively. With cloud-based platforms, financial services can also reduce infrastructure costs and reallocate resources toward innovation and strategic growth.

Growing Emphasis on Data-Driven Decision-Making Boosts Cloud Analytics in Fintech

The rising reliance on data analytics for personalized financial services and real-time decision-making is significantly boosting the adoption of cloud technology in fintech. Cloud platforms offer the computing power and storage needed to analyze vast amounts of customer data quickly and efficiently. This enables companies to gain actionable insights, detect fraud, assess credit risk, and enhance user experiences. As financial services strive to become more data-driven, the ability to integrate cloud-based analytics tools becomes essential, driving the momentum of cloud infrastructure across the fintech landscape.

Digital Transformation and Regulatory Compliance Propel Cloud Integration

The push for digital transformation, alongside the demand to meet evolving regulatory requirements, is prompting many financial institutions to turn to cloud solutions. Cloud computing supports automation, improves transparency, and facilitates real-time monitoring, all of which are crucial for complying with financial regulations. Moreover, cloud service providers are increasingly offering solutions that are tailored for compliance with global standards like GDPR, PCI-DSS, and ISO 27001. As the financial ecosystem becomes more complex and regulated, cloud platforms serve as a secure and efficient foundation for managing compliance while driving digital change.

Increased Collaboration and Ecosystem Expansion Fuel Cloud Adoption in Fintech

The fintech sector thrives on collaboration and integration across platforms, services, and APIs. Cloud computing enables seamless connectivity and integration among various stakeholders, including banks, payment processors, insurers, and tech startups. By leveraging cloud-based APIs and microservices, fintech companies can accelerate innovation, reduce time-to-market, and deliver better customer experiences. Additionally, the cloud facilitates cross-border partnerships and the development of ecosystem-driven business models. This openness and interoperability are becoming essential in today’s competitive financial landscape, thereby reinforcing the pivotal role of cloud in shaping the future of fintech.

Fintech Cloud Market Restraints and Challenges:

Security Concerns and Data Privacy Issues Pose Significant Restraints to Fintech Cloud Adoption

Despite its many advantages, the Fintech Cloud Market faces substantial restraints primarily related to security concerns and data privacy issues. Financial institutions handle highly sensitive customer data, and any breach can result in severe legal, financial, and reputational damage. The migration of core operations to the cloud increases vulnerability to cyber threats, including data breaches, DDoS attacks, and insider risks. The compliance with stringent regulatory frameworks across different regions—such as GDPR in Europe or data localization laws in certain countries—complicates cloud implementation. The lack of complete control over third-party cloud environments, coupled with concerns about data residency, latency, and interoperability, continues to challenge full-scale adoption among more traditional and risk-averse financial entities.

Fintech Cloud Market Opportunities:

The Fintech Cloud Market presents significant opportunities driven by the growing demand for scalable, agile, and cost-effective digital infrastructure among financial institutions. As more fintech startups and traditional banks embrace digital transformation, cloud solutions offer the flexibility to innovate rapidly and launch new services like digital wallets, robo-advisory, and real-time payments. The rise of embedded finance, open banking, and API-driven ecosystems further amplifies the demand for cloud-based platforms that support seamless integration and collaboration. Additionally, advances in AI and machine learning integrated with cloud systems are enabling personalized financial experiences, smarter fraud detection, and predictive analytics—creating fertile ground for growth and disruption in the sector.

Fintech Cloud Market Segmentation:

Market Segmentation: By Service Type:

• Cloud-Based Banking

• Cloud-Based Insurance

• Cloud-Based Lending

• Cloud-Based Wealth Management

• Cloud-Based Payments

Cloud-Based Payments has emerged as the dominant segment in the fintech cloud market due to the rapid adoption of digital payment platforms, mobile wallets, and contactless payment solutions across both developed and developing economies. As consumers increasingly prefer cashless transactions for their speed and convenience, financial institutions are investing heavily in cloud-based infrastructures to scale their payment operations, ensure real-time processing, and improve cybersecurity. The rise of e-commerce, along with regulatory support for digital transactions in many regions, has further cemented the leadership of this segment, making it an essential pillar in modern financial ecosystems.

Cloud-Based Banking is projected to be the fastest-growing segment, fueled by increasing demand for digital-first banking experiences and the shift from legacy systems to cloud-native architectures. Traditional banks are now adopting cloud to modernize their core banking systems, enabling faster product development, efficient operations, and improved customer engagement. At the same time, digital-only neobanks and challenger banks are gaining traction, relying entirely on cloud infrastructures to provide seamless and flexible banking services.

Market Segmentation: By Deployment:

• Private

• Public

• Hybrid

Private Cloud deployment is widely adopted by financial institutions prioritizing data security, regulatory compliance, and operational control. This model allows for customized infrastructure, ensuring sensitive financial data is managed in a dedicated environment. Large banks and established financial organizations often prefer private clouds to maintain internal oversight, reduce third-party risks, and meet industry-specific regulations. Its ability to offer a controlled environment makes it the dominant deployment type, especially in heavily regulated sectors like banking and insurance.

Hybrid Cloud is experiencing the fastest growth rate due to its flexibility in balancing security and scalability. Organizations are leveraging hybrid models to keep sensitive operations on private infrastructure while using public cloud for non-critical workloads, innovation projects, or customer-facing applications. This approach enables cost optimization, agility, and seamless data integration, making it particularly attractive to mid-sized and large fintech firms aiming for digital transformation without compromising compliance.

Market Segmentation: By Enterprise:

• Large Enterprise

• Small and Medium Enterprise (SMEs)

Large Enterprises dominate the fintech cloud market, fueled by their extensive financial operations, complex compliance requirements, and need for robust, scalable cloud solutions. These organizations invest heavily in cloud infrastructure to enhance operational efficiency, ensure data security, and support large-scale digital transformation initiatives. Their significant budgets and strategic focus on innovation make them the primary consumers of advanced fintech cloud services, enabling them to stay competitive in a rapidly evolving financial landscape.

Small and Medium Enterprises (SMEs) represent the fastest-growing segment in the fintech cloud market due to growing digital adoption and the need for cost-effective, flexible cloud solutions. SMEs leverage cloud-based fintech platforms to streamline their financial processes, improve customer experiences, and scale operations without heavy upfront investments. The accessibility and scalability of cloud technology empower these smaller organizations to compete with larger players by adopting innovative financial services quickly and efficiently.

Market Segmentation: By Application:

• Back-end Operations

• Customer Experiences

• Regulatory Compliance

• Data Analysis

• Risk Management

Back-end Operations hold a dominant position in the fintech cloud market, as financial institutions rely heavily on cloud infrastructure to manage transaction processing, payment systems, and core banking functions. This application area demands high reliability, security, and scalability, making it critical for maintaining seamless daily financial operations. Cloud solutions in this segment optimize efficiency and reduce operational costs, allowing enterprises to focus on innovation and customer-centric services.

Customer Experiences represent the fastest-growing application within the fintech cloud sector. Financial organizations increasingly utilize cloud technologies to deliver personalized, real-time services such as mobile banking, chatbots, and AI-driven customer support. Enhancing user engagement and satisfaction through seamless, cloud-powered digital interfaces is a strategic priority, fueling rapid adoption of these solutions across fintech platforms.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

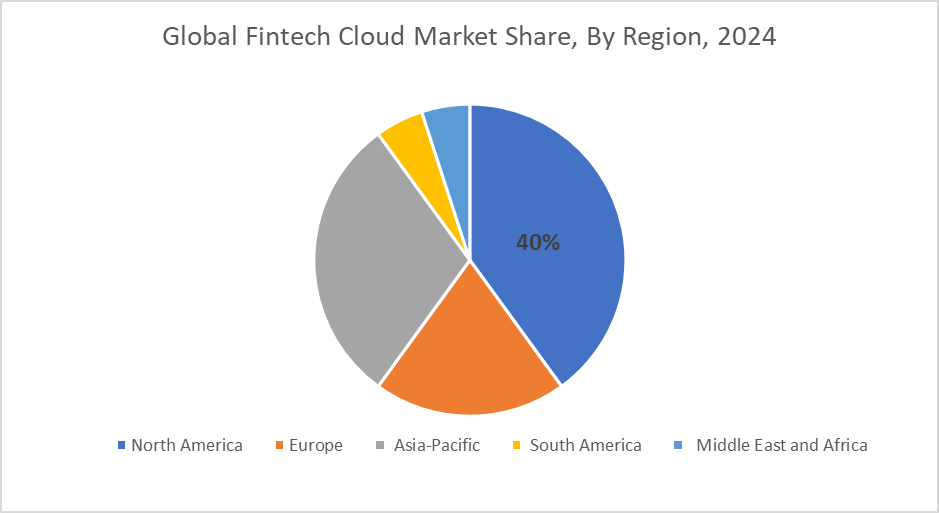

North America holds the dominant position in the Fintech Cloud Market, contributing around 40% of the global revenue. This leadership is driven by the region’s advanced technological infrastructure, early adoption of cloud solutions, and a strong presence of major fintech companies investing heavily in cloud-based innovation. The mature regulatory environment and high digital financial literacy further strengthen North America’s grip on the market, making it the most influential region for fintech cloud services worldwide.

Asia-Pacific is the fastest-growing region, contributing approximately 30% to the global market and showing rapid expansion due to increasing digital transformation, rising smartphone penetration, and supportive government initiatives promoting fintech adoption. Emerging economies such as China, India, and Southeast Asian countries are investing heavily in cloud infrastructure to improve financial inclusion and modernize banking services. This dynamic growth positions Asia-Pacific as the primary region to watch for future advancements and market expansion in fintech cloud technologies.

COVID-19 Impact Analysis on the Global Fintech Cloud Market:

The COVID-19 pandemic significantly disrupted the global Fintech Cloud market, causing a sharp decline in international patient travel because of travel restrictions, safety concerns, and overwhelmed healthcare systems. Many elective procedures were postponed, and hospitals prioritized COVID-19 care, leading to reduced demand. However, the market is gradually recovering as vaccination rates increase and healthcare facilities implement strict safety protocols, with growing interest in telemedicine and regional medical travel reshaping future trends.

Latest Trends/ Developments:

The Fintech Cloud market is witnessing a shift toward advanced digital integration, with the adoption of teleconsultations, online appointment systems, and AI-based patient management tools. These technologies are making it easier for international patients to connect with healthcare providers, evaluate treatment options remotely, and plan their travel more efficiently. Additionally, hospitals in popular destinations are upgrading infrastructure to cater to a growing demand for cosmetic surgeries, fertility treatments, and wellness therapies, combining healthcare with luxury and recovery experiences.

Another major trend is the rising emphasis on personalized and patient-centric care. Medical tourists are now seeking treatments that align with their lifestyle and preferences, such as holistic wellness, integrative medicine, and post-treatment rehabilitation packages. Countries known for affordability and quality—such as those in Southeast Asia and Eastern Europe—are focusing on creating specialized healthcare hubs that cater to niche markets like dental tourism, orthopedic procedures, and cardiology. Sustainability and ethical practices in treatment and hospitality are also gaining attention, influencing destination choices.

Key Players:

• RACKSPACE TECHNOLOGY

• VMware, Inc.

• Amazon.com, Inc.

• Google LLC

• International Business Machines Corporation

• SAP SE

• Microsoft

• Cisco Systems, Inc.

• Salesforce, Inc.

• Oracle

Chapter 1. Global Fintech Cloud Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Fintech Cloud Market – Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Fintech Cloud Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Fintech Cloud Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Fintech Cloud Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Fintech Cloud Market – By Service Type

6.1. Cloud-Based Banking

6.2. Cloud-Based Insurances

6.3. Cloud-Based Lending

6.4. Cloud-Based Wealth Management

6.5. Cloud-Based Payments

6.6. Y-O-Y Growth trend Analysis By Service Type

6.7. Absolute $ Opportunity Analysis By Service Type, 2025-2030

Chapter 7. Global Fintech Cloud Market – By Deployment

7.1. Public

7.2. Private

7.3. Hybrid

7.4. Y-O-Y Growth trend Analysis By Deployment

7.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 8. Global Fintech Cloud Market – By Enterprise

8.1. Large Enterprise

8.2. Small and Medium Enterprise (SMEs)

8.3. Y-O-Y Growth trend Analysis By Enterprise

8.4. Absolute $ Opportunity Analysis By Enterprise, 2025-2030

Chapter 9. Global Fintech Cloud Market – By Application

9.1. Back-end Operations

9.2. Customer Experience

9.3. Regulatory Compliance

9.4. Data Analysis

9.5. Risk Management

9.6. Y-O-Y Growth trend Analysis By Application

9.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 10. Global Fintech Cloud Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Service Type

10.1.3. By Deployment

10.1.4. By Enterprise

10.1.5. By Application

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Service Type

10.2.3. By Deployment

10.2.4. By Enterprise

10.2.5. By Application

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Service Type

10.3.3. By Deployment

10.3.4. By Enterprise

10.3.5. By Application

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Service Type

10.4.3. By Deployment

10.4.4. By Enterprise

10.4.5. By Application

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Service Type

10.5.3. By Deployment

10.5.4. By Enterprise

10.5.5. By Application

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Fintech Cloud Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1 RACKSPACE TECHNOLOGY

11.2 VMware, Inc.

11.3 Amazon.com, Inc.

11.4 Google LLC

11.5 International Business Machines Corporation

11.6 SAP SE

11.7 Microsoft

11.8 Cisco Systems, Inc.

11.9 Salesforce, Inc.

11.10 Oracle

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Fintech Cloud Market was valued at USD 37.7 billion in 2024 and is projected to reach a market size of USD 80.56 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.4%.

Rising demand for digital financial services is driving fintech cloud adoption.

Based on Deployment, the Global Fintech Cloud Market is segmented into Public, Private and Hybrid.

North America is the most dominant region for the Global Fintech Cloud Market.

RACKSPACE TECHNOLOGY, VMware, Inc., Amazon.com, Inc., Google LLC are the leading players in the Global Fintech Cloud Market.