Global EV charging station Market Research Report – Segmentation by Charging Type (AC Charging, DC Fast Charging, Wireless Charging); by Application (Residential, Commercial, Highway/Transit, Fleet Charging); by End User (Private Consumers, Public Sector, Commercial Businesses, Utilities and Energy Providers); Region – Forecast (2025 – 2030)

Published: 2024 - March

Report Code: IM-16245

Format:

Region: Global

Market Size and Overview:

The EV charging station Market was valued at USD 30.23 billion and is projected to reach a market size of USD 148.78 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 37.53%.

The EV charging station market is a key pillar of the rapidly evolving electric mobility ecosystem. As electric vehicles become more common on roads worldwide, the demand for accessible and reliable charging infrastructure continues to rise. Charging stations serve as the backbone that supports this transition from fossil fuels to cleaner energy sources. The market includes various types of chargers, from slower home-based setups to ultra-fast commercial DC stations found along highways and in city centers.

This ecosystem is shaped by a mix of stakeholders, including governments, automotive companies, utility providers, and technology startups. There's a growing interest in smart charging solutions, grid integration, and renewable energy tie-ins. Urban planning, energy management, and even consumer habits are being reshaped around the availability of EV charging infrastructure. At the same time, developing countries are catching up by exploring scalable, cost-effective solutions for both urban and rural needs. All of this makes the EV charging station market not just a technological movement, but a cultural and infrastructural shift.

Key Market Insights:

In 2023, global public charging points crossed 3 million units, with China accounting for over 60% of that number. The year saw a notable push from governments and private players to scale infrastructure in urban centers and highways. This expansion was especially significant in Europe, where new policy mandates pushed for installation of high-power chargers every 60 km on major roads.

By 2024, several automakers and charging providers rolled out ultra-fast DC chargers (above 250 kW) in key markets, notably the U.S., Germany, and South Korea. These chargers can top up compatible EVs in under 20 minutes, aligning with consumer expectations for faster turnaround. The trend was supported by next-gen EV models designed to handle high voltage charging without battery degradation.

As of mid-2024, about 65–70% of EV users still primarily charge at home or at work, but reliance on public infrastructure increased compared to 2023. This shift was driven by more long-distance EV travel and better availability of fast public chargers. Urban EV owners without private parking remain a core user group for public charging.

In 2023 and 2024, Europe made strong progress toward a connected, interoperable EV charging ecosystem. Operators like Ionity and Allego expanded networks across 20+ countries, supporting plug-and-charge protocols and unified billing systems. EU regulations pushed for transparency in pricing and mandatory card payment compatibility, making charging more seamless.

By 2024, many new installations, particularly in the U.S. and Europe, featured smart charging capabilities, allowing for load balancing and integration with renewable energy. Utilities began rolling out vehicle-to-grid (V2G) pilot projects, testing how EVs could help stabilize local grids. Smart features also became common in home chargers, offering time-of-use scheduling to reduce electricity costs.

EV charging station Market Drivers:

Government Incentives and Regulations

Governments worldwide are actively supporting EV infrastructure through financial incentives, grants, and mandates. In regions like the EU, U.S., and China, policies require new buildings and parking areas to include EV charging provisions. Additionally, fuel economy standards and emission targets are pushing automakers and cities to invest in charging infrastructure. This policy-driven momentum plays a foundational role in shaping the market.

Rising EV Adoption and Model Availability

The surge in electric vehicle adoption is directly increasing the need for widespread and reliable charging networks. Consumers now have access to a growing range of EV models across various price points, from compact cars to luxury SUVs. As the number of EVs on the road rises, demand for both home and public charging options is accelerating. This trend is particularly visible in urban areas and along intercity travel routes.

Technological Advancements in Charging Solutions

Charging technology has evolved significantly in recent years, with faster, smarter, and more energy-efficient systems becoming the norm. Ultra-fast DC chargers can now deliver hundreds of kilometers of range in under 30 minutes, improving user experience. Smart charging features such as app-based control, energy optimization, and integration with solar or battery storage are becoming common. These innovations are making EV ownership more practical and attractive.

EV charging station Market Restraints and Challenges:

High Initial Infrastructure and Installation Costs

Setting up EV charging stations, especially fast-charging or commercial-grade units, involves significant capital investment. Costs include not only the hardware but also land acquisition, grid upgrades, and ongoing maintenance. For many regions and businesses, these expenses are a barrier to large-scale deployment. This challenge is more acute in developing countries where public funding and private incentives are limited.

Grid Capacity and Load Management Issues

As EV adoption increases, the added demand on local electricity grids can become a major concern. In areas with outdated or limited infrastructure, widespread charging can lead to voltage drops or supply instability. Utilities need to invest in grid modernization and load-balancing systems to handle the added stress. Without proper planning, mass adoption could strain power systems, especially during peak hours.

Lack of Standardization and Interoperability

The absence of universal charging standards across countries and manufacturers leads to fragmented user experiences. EV owners often face compatibility issues with connectors, payment platforms, and network access. This discourages long-distance travel and creates hesitation among new EV buyers. Interoperability challenges also make it harder for operators to scale networks efficiently across regions.

EV charging station Market Opportunities:

The EV charging station market holds significant untapped opportunities as the global shift toward electric mobility accelerates. One major area is the integration of renewable energy sources like solar and wind with charging infrastructure, creating greener and more self-sufficient systems. Smart charging technologies and vehicle-to-grid (V2G) solutions also open new revenue streams by allowing EVs to interact with the power grid. There's growing space for subscription-based models and charging-as-a-service, especially for fleet operators and urban dwellers.

As urban centers expand their low-emission zones, the need for dense city-wide charging networks becomes a clear opportunity for infrastructure providers. Rural and semi-urban areas, which currently lack adequate infrastructure, present a fresh market for expansion. There’s also potential in cross-industry partnerships, where energy providers, automakers, and tech firms collaborate to deliver seamless charging experiences. As battery technology improves and charging becomes faster, more users will rely on public networks, increasing footfall and usage rates. Lastly, developing markets like India, Southeast Asia, and parts of Africa offer long-term growth potential due to rising EV penetration and favorable policy shifts.

EV charging station Market Segmentation:

Market Segmentation: by Charging Type

• AC Charging

• DC Fast Charging

• Wireless Charging

AC charging, particularly Level 1 and Level 2 chargers, remains the most widely used globally due to its affordability and ease of installation. These chargers are most commonly found in homes, offices, and low-traffic public areas. While slower than DC fast chargers, they are well-suited for overnight and long-duration charging. Their large share is driven by residential users and the fact that most EVs come with AC charging compatibility. This segment shares 60% of the market.

DC fast chargers are critical for commercial stations, highway corridors, and fleet operations, offering rapid charging capabilities (often 80% charge in under 30 minutes). Their adoption is increasing as EV drivers demand faster and more convenient charging experiences. These chargers are more expensive to install and operate, often requiring grid upgrades and cooling systems. As battery tech evolves, their usage is expected to keep rising in high-traffic areas. The market share of this segment is 35%.

Wireless charging is still in its early stages, with limited adoption across pilot projects and high-end residential setups. This technology uses inductive transfer, allowing drivers to charge EVs simply by parking over a charging pad. While convenient and aesthetically appealing, high costs and low efficiency currently limit widespread deployment. It holds future promise in urban areas and autonomous vehicle infrastructure. This segment shares 5% of the market.

Market Segmentation: by Application

• Residential

• Commercial

• Highway/Transit

• Fleet Charging

Most EV owners charge their vehicles at home, making residential setups the largest application segment. These installations are typically AC chargers connected to household electrical systems. Ease of use, lower cost, and overnight charging convenience drive this segment's dominance. Government incentives and building codes are also encouraging home charger adoption. This segment has 60% market share.

Commercial applications include charging stations at malls, offices, restaurants, and parking garages. These locations typically use a mix of AC and DC chargers to serve employees, customers, or the public. This segment is growing fast as businesses see value in offering EV charging as a service or incentive. Charging access also helps increase customer dwell time and brand sustainability image. This segment shares 20% of the market.

Highway and transit-oriented charging serves long-distance travelers and heavy-use EVs such as buses or taxis. These stations rely on high-power DC fast chargers and are often located at rest stops, fuel stations, or transportation hubs. The infrastructure here is vital to reduce range anxiety and encourage EV use for intercity travel. Many governments are mandating the development of such corridors. This segment has 10% market share.

Fleet charging caters to commercial EV fleets—such as logistics vans, ride-hailing cars, and delivery vehicles. These operations require centralized, high-capacity chargers and often use load management systems to reduce energy costs. The demand for fleet-specific charging solutions is rising as last-mile delivery and logistics increasingly shift to electric. Scalability and operational cost control are key drivers here. This segment also shares 10% of the market.

Market Segmentation: by End User

• Private Consumers

• Public Sector

• Commercial Businesses

• Utilities and Energy Providers

Individual EV owners represent the largest end-user segment, primarily charging at home or in residential communities. Their needs are typically met with Level 1 or Level 2 AC chargers that provide overnight convenience. Ease of access, affordability, and control over energy consumption make private ownership the most prominent. Many users also install smart chargers for scheduling and energy optimization. This segment has 60% of the market share.

Governments and municipalities play a key role in deploying EV infrastructure in public spaces like parks, streets, and transit stations. These entities often fund large-scale projects through public-private partnerships or subsidies. Their role is vital in underserved or high-density areas where private solutions may be unfeasible. Public sector efforts are also aligned with climate targets and urban planning. This segment has 10% market share.

This group includes businesses offering EV charging to employees, customers, or tenants as part of their service portfolio. Charging stations are installed at commercial premises such as malls, tech campuses, and hotels. Businesses see this as a way to attract customers, improve ESG scores, and increase dwell time. Some also monetize charging through apps or loyalty programs. This segment has 20% of the market share.

Electric utilities and energy firms are increasingly entering the EV charging space, integrating stations with grid services and renewable energy. They offer smart charging, dynamic pricing, and load balancing solutions to optimize electricity usage. This segment is vital for ensuring that EV adoption does not destabilize local energy systems. Utilities also have an advantage in scaling infrastructure quickly using existing assets. This segment also has 10% of the market share.

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

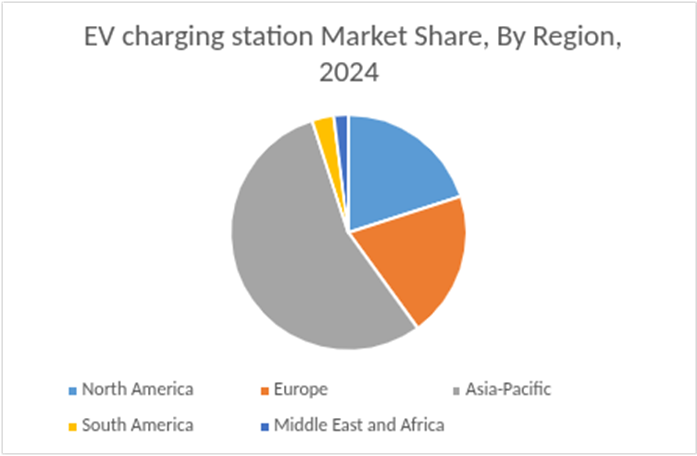

North America, led by the United States and Canada, has seen a strong push toward expanding fast-charging networks, especially along interstate highways and urban hubs. Government initiatives like the U.S. NEVI program and growing consumer EV adoption have helped accelerate infrastructure development. Tech companies and automakers are also partnering to expand coverage and improve user experience. North America holds approximately 20% of the global EV charging station market.

Asia-Pacific is the undisputed leader in the global EV charging market, largely driven by China’s aggressive infrastructure rollout and policy backing. Japan and South Korea are also investing in dense urban networks and next-gen technologies like wireless charging. The region benefits from high EV sales, urbanization, and manufacturing dominance in EV components. Asia-Pacific accounts for about 55% of the global market share.

Europe has established a highly regulated and interoperable EV charging ecosystem, with countries like Germany, the Netherlands, and Norway leading adoption. Strict emissions laws, cross-border networks, and incentives for renewable energy integration are shaping the market. Public and private partnerships have built an extensive fast-charging corridor across the continent. Europe holds around 20% of the global market share.

South America's EV infrastructure is still in its early stages, with countries like Brazil, Chile, and Colombia gradually building up public and private charging networks. Economic constraints and limited EV availability have slowed widespread adoption, but there is rising interest from urban centers. Most chargers are concentrated in capital cities or wealthier regions. South America contributes about 3% to the global EV charging station market.

The MEA region is emerging slowly, with the UAE, Saudi Arabia, and South Africa taking early steps in EV infrastructure development. Projects are often government-led or tied to smart city plans and sustainability goals. Harsh climates and energy grid limitations pose challenges in some areas, but luxury EV demand is creating niche markets. Middle East and Africa together account for roughly 2% of the global market.

COVID-19 Impact Analysis on the Global EV charging station Market:

The COVID-19 pandemic had a mixed but ultimately transformative impact on the EV charging station market. In the early months of 2020, lockdowns and supply chain disruptions caused significant delays in charging infrastructure projects worldwide. Manufacturing of hardware components slowed down due to labor shortages and restricted movement of goods. Many governments also redirected public spending to health and emergency services, putting infrastructure plans temporarily on hold.

However, the pandemic also led to a noticeable shift in environmental priorities and green recovery plans. Several countries introduced EV-focused stimulus packages to revive their economies, which included incentives for both vehicle purchases and charging infrastructure. Consumer interest in private mobility increased during the pandemic, reducing reliance on shared or public transportation, and indirectly boosting EV sales. This trend created more demand for home and workplace chargers.

Moreover, the disruption highlighted the importance of building resilient and decentralized infrastructure, prompting cities and energy providers to re-evaluate their strategies. As a result, post-COVID recovery saw a stronger and more targeted push toward EV charging networks, especially those integrated with renewable energy and smart grids. In many ways, the pandemic acted as a catalyst for long-term investment in sustainable mobility.

Latest Trends/Developments:

The EV charging station market is experiencing a wave of innovation and structural evolution as of 2023–2024. A major trend is the rollout of the universal Plug & Charge protocol, which will allow seamless, app-free charging by simply connecting the vehicle to the station. Ultra-fast charging infrastructure is expanding, especially in the EU and China, with 350 kW+ stations becoming more common for quicker turnaround. Simultaneously, smart charging and grid integration are gaining ground through advanced load balancing, AI-driven energy management, and real-time communication protocols like OCPP 2.1.

Another exciting development is the growth of Vehicle-to-Grid (V2G) technology, enabling EVs to supply power back to the grid during peak demand. Wireless charging, both static and dynamic (while driving), is undergoing testing in cities and highways, showing promise for urban mobility. Business models are also shifting—Charging-as-a-Service (CaaS) now allows companies and fleet owners to deploy infrastructure without upfront capital costs. Renewable energy-powered charging stations, especially those combining solar panels and battery storage, are being deployed to reduce grid dependency and emissions. At the same time, connector standardization efforts (like Tesla's NACS gaining traction in North America) are helping make the ecosystem more user-friendly and interoperable. Finally, large-scale public-private partnerships are driving national rollouts, such as fast-charging corridors in India and federally funded networks in the U.S., setting the stage for mass adoption.

Key Players:

• ChargePoint, Inc,

• Tesla, Inc.

• ABB

• BP Chargemaster

• ClipperCreek, Inc.

• Bikeep

• Robert Bosch GmbH

• Get Charged, Inc.

• Flower Turbines

• Ather Energy

Chapter 1. Global EV charging station Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global EV charging station Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn/$Tn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global EV charging station Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global EV charging station Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global EV charging station Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global EV charging station Market – By Charging Type

6.1. Introduction/Key Findings

6.2. AC Charging

6.3. DC Fast Charging

6.4. Wireless Charging

6.5. Y-O-Y Growth trend Analysis By Charging Type

6.6. Absolute $ Opportunity Analysis By Charging Type, 2025-2030

Chapter 7. Global EV charging station Market – By Application

7.1. Introduction/Key Findings

7.2. Residential

7.3. Commercial

7.4. Highway/Transit

7.5. Fleet Charging

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global EV charging station Market – By End User

8.1. Introduction/Key Findings

8.2. Private Consumer

8.3. Public Sector

8.4. Commercial Businesses

8.5. Utilities and Energy Providers

8.6. Y-O-Y Growth trend Analysis By End User

8.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global EV charging station Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Charging Type

9.1.3. By Application

9.1.4. By End User

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Charging Type

9.2.3. By Application

9.2.4. By End User

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Charging Type

9.3.3. By Application

9.3.4. By End User

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Charging Type

9.4.3. By Application

9.4.4. By End User

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Charging Type

9.5.3. By Application

9.5.4. By End User

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global EV charging station Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. ChargePoint, Inc,

10.2. Tesla, Inc.

10.3. ABB

10.4. BP Chargemaster

10.5. ClipperCreek, Inc.

10.6. Bikeep

10.7. Robert Bosch GmbH

10.8. Get Charged, Inc.

10.9. Flower Turbines

10.10. Ather Energy

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The EV charging station Market was valued at USD 30.23 billion and is projected to reach a market size of USD 148.78 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 37.53%.

Government Incentives and Regulations, Rising EV Adoption and Model Availability, Technological Advancements in Charging Solutions are some of the key market drivers in the EV charging station Market.

Residential, Commercial, Highway/Transit, Fleet Charging are the segments by Application in the EV charging station Market.

Asia-Pacific is the most dominant region for the Global EV charging station Market.

ChargePoint, Inc, Tesla, Inc., ABB, BP Chargemaster, ClipperCreek, Inc., Bikeep, Robert Bosch GmbH, Get Charged, Inc., Flower Turbines, Ather Energy etc.