Energy Storage for Unmanned Aerial Vehicles Market Research Report – Segmentation by Type (Lithium-Ion Batteries, Solid-State Batteries, Hydrogen Fuel Cells, Hybrid Power Systems, Supercapacitors); By Distribution Channel (Original Equipment Manufacturers (OEMs), Aftermarket Sales, Direct Sales, Specialized Integrators, Online Retailers); By Application (Military & Defense, Commercial Logistics & Delivery, Agriculture & Forestry, Infrastructure Inspection & Monitoring, Entertainment & Media); By UAV Type (Rotary-Wing UAVs, Fixed-Wing UAVs, Hybrid VTOL UAVs, Nano/Micro UAVs, Large Cargo UAVs); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16570

Format:

Region: Global

Market Size and Overview:

The Energy Storage for Unmanned Aerial Vehicles (UAVs) Market was valued at USD 4.85 Billion in 2024 and is projected to reach a market size of USD 14.57 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.6%.

The Energy Storage for Unmanned Aerial Vehicles (UAVs) Market is undergoing a profound transformation, driven by the insatiable demand for extended flight durations, enhanced payload capacities, and rapid operational turnaround times across a myriad of applications. This dynamic sector is at the nexus of advanced battery technology, fuel cell innovation, and sophisticated power management systems, all tailored to meet the unique and stringent requirements of autonomous flight. Historically, UAV performance has been significantly constrained by the limitations of conventional energy storage solutions, primarily impacting flight range, endurance, and the weight of onboard equipment. However, the burgeoning advancements in materials science, electrochemical engineering, and power electronics are rapidly dismantling these barriers, ushering in an era where UAVs can perform more complex, longer-duration missions with greater efficiency.

Furthermore, the shift towards sustainable aviation also places a premium on cleaner energy storage options, further stimulating innovation in areas like hydrogen and advanced battery recycling.

Key Market Insights:

Lithium-ion batteries constituted approximately 85% of all energy storage solutions deployed in UAVs during 2024, reflecting their established market dominance.

The average energy density of commercial UAV batteries reached 250 Wh/kg in 2024, a notable improvement over previous years. Investment in solid-state battery R&D for aviation applications surpassed $350 million in 2024, indicating strong future potential.

Hydrogen fuel cell systems for long-endurance drones saw a 40% increase in prototype deployments in 2024 compared to the previous year. The average charging time for standard commercial drone batteries decreased by 15% in 2024 due to advancements in fast-charging technologies.

Approximately 60% of new large cargo drones introduced in 2024 incorporated some form of hybrid power system. The market for lightweight, high-power supercapacitors for UAVs grew by 25% in 2024, primarily for burst power applications.

Over 75% of military UAVs adopted specialized energy storage solutions designed for extreme temperature operations in 2024. The average flight time for small commercial inspection drones increased by 18% in 2024 due to battery improvements.

The cost per Wh for UAV energy storage solutions declined by an average of 8% in 2024. The adoption rate of smart battery management systems (BMS) in new UAV designs reached 92% in 2024.

Market Drivers:

Digital Transformation Acceleration

The rapid acceleration of digital transformation across various industries is a primary driver for the energy storage market in UAVs. As businesses increasingly adopt drones for automation, data collection, and operational efficiency, the demand for reliable and high-performance energy solutions becomes paramount. From precision agriculture to infrastructure inspection and logistics, drones are becoming indispensable tools. This widespread integration necessitates energy storage systems that can support longer flight times, heavier payloads, and faster turnaround, directly fueling innovation and investment in advanced battery and fuel cell technologies to meet the evolving operational requirements of a digitally transformed economy.

Advancements in Autonomous Flight Technology

The continuous evolution of autonomous flight capabilities, including advanced navigation, AI-driven decision-making, and sophisticated sensor integration, directly propels the demand for superior energy storage. As UAVs become more intelligent and capable of complex, unsupervised missions, the need for robust and enduring power sources intensifies. These advancements enable drones to perform tasks that were previously unfeasible, such as long-range surveillance or multi-point deliveries, which inherently require energy systems that offer extended endurance, higher power output, and enhanced reliability, thereby stimulating significant growth and innovation in the energy storage sector for UAVs.

Market Restraints and Challenges:

The market faces significant restraints, primarily the inherent limitations of current battery energy density, which directly impacts UAV flight endurance and payload capacity. High initial costs of advanced energy storage solutions, particularly solid-state batteries and hydrogen fuel cells, pose a barrier to widespread adoption. Furthermore, the complexities associated with thermal management, especially in high-power discharge scenarios, and the safety concerns related to battery flammability, present persistent technical challenges that hinder market expansion and require continuous innovation to overcome.

Market Opportunities:

The burgeoning demand for long-endurance and heavy-lift UAVs in sectors like logistics and defense offers substantial opportunities for advanced energy storage solutions like hydrogen fuel cells and high-density solid-state batteries. The development of integrated charging infrastructure, including rapid charging stations and battery swapping systems, presents a lucrative market segment. Moreover, the increasing focus on sustainable aviation and green energy solutions will drive innovation in environmentally friendly power sources, opening new avenues for market growth and technological differentiation in the UAV energy storage landscape.

Market Segmentation:

Segmentation by Type:

• Lithium-Ion Batteries

• Solid-State Batteries

• Hydrogen Fuel Cells

• Hybrid Power Systems

• Supercapacitors

Solid-state batteries are emerging as the fastest-growing segment, driven by their promise of significantly higher energy density, enhanced safety (reduced risk of thermal runaway), and longer cycle life compared to traditional lithium-ion counterparts. As manufacturing processes mature and costs decrease, their adoption in high-performance and safety-critical UAV applications is rapidly accelerating, positioning them as a key future technology for extended flight capabilities.

Lithium-ion batteries currently dominate the market due to their established technology, high power-to-weight ratio, relative affordability, and widespread manufacturing infrastructure. They are the go-to choice for the vast majority of consumer, commercial, and many industrial UAVs, offering a balance of performance and cost-effectiveness that has made them indispensable for various drone applications, from recreational flying to professional aerial photography.

Segmentation by Distribution Channel:

• Original Equipment Manufacturers (OEMs)

• Aftermarket Sales

• Direct Sales

• Specialized Integrators

• Online Retailers

Specialized integrators represent the fastest-growing distribution channel, as they cater to complex, custom UAV solutions requiring tailored energy storage systems. These integrators work closely with end-users to design and implement bespoke power solutions for niche applications, such as heavy-lift industrial drones or specialized military platforms, driving demand for highly customized and high-performance energy storage units.

Original Equipment Manufacturers (OEMs) continue to dominate the market, as the majority of energy storage units are integrated directly into new UAVs during the manufacturing process. Drone manufacturers procure batteries and other power systems in large volumes from specialized suppliers, making OEM sales the primary channel for market penetration and volume-based revenue for energy storage providers.

Segmentation by Application:

• Military & Defense

• Commercial Logistics & Delivery

• Agriculture & Forestry

• Infrastructure Inspection & Monitoring

• Entertainment & Media

Commercial logistics and delivery applications are the fastest-growing segment, propelled by the increasing adoption of drones for last-mile delivery, warehouse management, and inter-facility transport. The demand for longer range, higher payload capacity, and rapid turnaround times in this sector is driving significant investment in advanced energy storage solutions, making it a key growth area for the market.

Military & defense applications remain the most dominant segment, commanding the largest share due to the critical need for high-performance, reliable, and secure energy storage for surveillance, reconnaissance, combat, and logistical support UAVs. Defense budgets often prioritize cutting-edge technology, leading to significant investment in advanced battery and fuel cell systems that offer superior endurance and operational capabilities in demanding environments.

Segmentation by UAV Type:

• Rotary-Wing UAVs

• Fixed-Wing UAVs

• Hybrid VTOL UAVs

• Nano/Micro UAVs

• Large Cargo UAVs

Large cargo UAVs represent the fastest-growing segment, driven by the burgeoning interest in drone-based logistics and heavy-lift operations for industrial and military purposes. These platforms require substantial energy storage capacity for long-range flights and heavy payloads, stimulating rapid innovation and adoption of high-density batteries and hydrogen fuel cells tailored for large-scale aerial transport.

Rotary-wing UAVs, particularly multirotors, continue to be the most dominant type in terms of energy storage demand. Their widespread use in commercial applications like aerial photography, inspection, and short-range delivery, coupled with their ease of operation and versatility, means a vast number of these drones are in circulation, driving consistent demand for their specific energy storage requirements.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

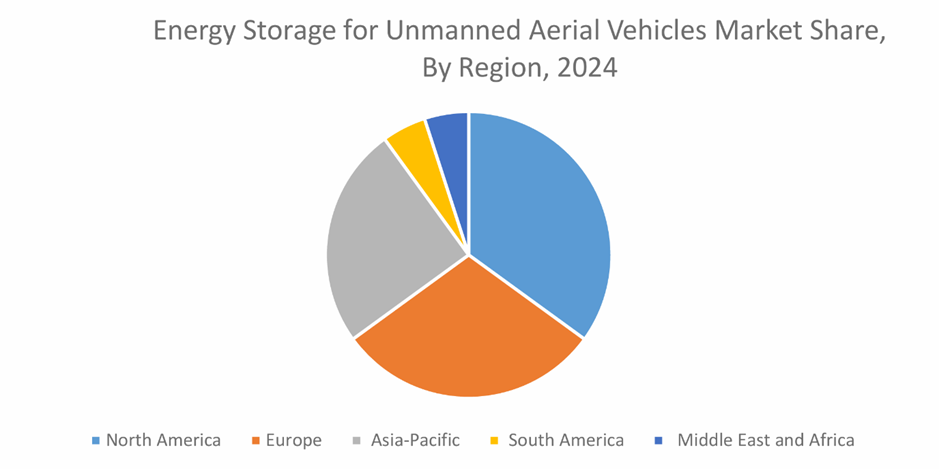

North America holds approximately 38% of the market share, followed by Europe with 25%, Asia-Pacific with 22%, and the rest of the world contributing 15%. North America maintains its dominance due to robust defense spending, a thriving commercial drone industry, and significant R&D investments in advanced energy technologies. Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, increasing drone adoption in logistics and agriculture, and supportive government initiatives promoting UAV technology.

COVID-19 Impact Analysis:

The COVID-19 pandemic significantly impacted the energy storage for UAVs market by both disrupting supply chains and accelerating demand. Initial lockdowns caused production delays and component shortages, particularly for batteries. However, the pandemic simultaneously highlighted the utility of drones for contactless delivery, surveillance, and medical supply transport, leading to increased investment and accelerated adoption in various sectors, ultimately stimulating long-term growth for energy storage solutions as drone operations expanded globally.

Latest Trends and Developments:

The energy storage for UAVs market is witnessing several transformative trends. There's a strong push towards solid-state battery commercialization, promising higher energy density and improved safety. Hydrogen fuel cell miniaturization is advancing rapidly for long-endurance applications. Integrated power management systems with AI are optimizing energy usage and extending flight times. Furthermore, advancements in rapid charging technologies and the development of modular, swappable battery packs are enhancing operational efficiency and reducing downtime for commercial drone fleets.

Key Players in the Market:

• Amprius Technologies, Inc.

• H3 Dynamics

• Intelligent Energy Ltd.

• Plug Power Inc.

• Skydio, Inc.

• DJI

• Parrot Drones SAS

• AeroVironment, Inc.

• QuantumScape Corporation

• Solid Power, Inc.

Chapter 1. Global Energy Storage for Unmanned Aerial Vehicles Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Energy Storage for Unmanned Aerial Vehicles Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Energy Storage for Unmanned Aerial Vehicles Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Energy Storage for Unmanned Aerial Vehicles Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Energy Storage for Unmanned Aerial Vehicles Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Energy Storage for Unmanned Aerial Vehicles Market – By Type

6.1. Introduction/Key Findings

6.2. Lithium-Ion Batteries

6.3. Solid-State Batteries

6.4. Hydrogen Fuel Cells

6.5. Hybrid Power Systems

6.6. Supercapacitors

6.7. Y-O-Y Growth trend Analysis By Type

6.8. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global Energy Storage for Unmanned Aerial Vehicles Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Original Equipment Manufacturers (OEMs)

7.3. Aftermarket Sales

7.4. Direct Sales

7.5. Specialized Integrators

7.6. Online Retailers

7.7. Y-O-Y Growth trend Analysis By Distribution Channel

7.8. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global Energy Storage for Unmanned Aerial Vehicles Market – By Application

8.1. Introduction/Key Findings

8.2. Military & Defense

8.3. Commercial Logistics & Delivery

8.4. Agriculture & Forestry

8.5. Infrastructure Inspection & Monitoring

8.6. Entertainment & Media

8.7. Y-O-Y Growth trend Analysis By Application

8.8. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 9. Global Energy Storage for Unmanned Aerial Vehicles Market – By UAV Type

9.1. Introduction/Key Findings

9.2. Rotary-Wing UAVs

9.3. Fixed-Wing UAVs

9.4. Hybrid VTOL UAVs

9.5. Nano/Micro UAVs

9.6. Large Cargo UAVs

9.7. Y-O-Y Growth trend Analysis By UAV Type

9.8. Absolute $ Opportunity Analysis By UAV Type, 2024-2030

Chapter 10. Global Energy Storage for Unmanned Aerial Vehicles Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Energy Storage Type

10.1.3. By Distribution Channel

10.1.4. By Application

10.1.5. By UAV Type

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Energy Storage Type

10.2.3. By Distribution Channel

10.2.4. By Application

10.2.5. By UAV Type

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Energy Storage Type

10.3.3. By Distribution Channel

10.3.4. By Application

10.3.5. By UAV Type

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Energy Storage Type

10.4.3. By Distribution Channel

10.4.4. By Application

10.4.5. By UAV Type

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Energy Storage Type

10.5.3. By Distribution Channel

10.5.4. By Application

10.5.5. By UAV Type

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Energy Storage for Unmanned Aerial Vehicles Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Amprius Technologies, Inc.

11.2. H3 Dynamics

11.3. Intelligent Energy Ltd.

11.4. Plug Power Inc.

11.5. Skydio, Inc.

11.6. DJI

11.7. Parrot Drones SAS

11.8. AeroVironment, Inc.

11.9. QuantumScape Corporation

11.10. Solid Power, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The market is primarily driven by the increasing demand for extended flight durations and enhanced payload capacities in UAVs across diverse applications, coupled with rapid advancements in autonomous flight technology that necessitate more robust and efficient power solutions.

Key concerns include the inherent limitations of current battery energy density, the high initial costs of advanced energy storage solutions, and persistent challenges related to thermal management and safety risks associated with battery flammability.

Key players include Amprius Technologies, Inc., H3 Dynamics, Intelligent Energy Ltd., Plug Power Inc., Skydio, Inc., DJI, Parrot Drones SAS, AeroVironment, Inc., QuantumScape Corporation, Solid Power, Inc., Ballard Power Systems, Inc., FuelCell Energy, Inc., Sion Power Corporation, StoreDot Ltd., and OXIS Energy Ltd.

North America currently holds the largest market share, estimated at approximately 38%, driven by significant defense spending and a mature commercial drone ecosystem.

Asia-Pacific is experiencing the highest growth rate, fueled by rapid digitalization, increasing drone adoption in commercial sectors, and supportive government policies promoting UAV technology development and deployment.