Global Electrical Digital Twin Market Research Report – Segmentation By Product Type (Digital Power Plant Twin, Digital Grid Twin, Digital Substation Twin, Distribution Network Twin, Others), By Deployment Mode (On-premises, Cloud), By End-Use Industry (Utility Service Providers, Grid Infrastructure Operators, Renewable Energy, Manufacturing, Transportation & Logistics, Others), By Distribution Channel (Direct OEM Sales, System Integrators, Online Platforms), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16568

Format:

Region: Global

Market Size and Overview:

The Global Electrical Digital Twin Market was valued at USD 1.35 billion in 2024 and is projected to reach a market size of USD 2.40 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 12.16%.

Real-time IoT sensor data, machine learning analytics, and physics-based simulations are used by electrical digital twins, virtual replicas of power systems, substations, grids, and generation assets, to maximize performance, predict failures, and speed decision-making. Adoption is driven by utilities' push for grid modernization, renewable integration difficulties, and severe reliability and sustainability demands. These solutions assist virtual commissioning of complicated electrical infrastructure over many end‑use industries, lower downtime, and improve asset management efficiency.

Key Market Insights:

Using digital twins to simulate distribution networks, reduce outage durations, and carry out predictive maintenance on transformers and switchgear, utility firms make up more than 40% of present revenues.

Reflecting the pressing need to upgrade deteriorating substation assets and adhere to changing grid codes, digital twins of substations accounted for the greatest product category with 31% market share.

Electrical Digital Twin Market Drivers:

The recent modernization of the grid and reliability mandates are driving the growth of this market.

Utilities in North America and Europe are actively upgrading old infrastructure with digital‑twin solutions to fulfill strict N‑1 contingency requirements and improve overall grid resilience. A Lawrence Berkeley Lab report projects that power outages cost the U. S. economy USD 150 billion a year, hence emphasizing the economic need for proactive asset management. By enabling virtual commissioning of substations and transmission improvements, digital twins let operators simulate N‑1 failure circumstances in real time and maximize protection schemes before actual deployment. By integrating SCADA, GIS, and asset‑management databases, these platforms minimize unexpected outages and prolong equipment lifespans via condition‑based maintenance. Post‑implementation metrics from first adopters show a 15–20% decrease in outage durations and 10% longer transformer service life. Digital-twin-driven grid modernization becomes essential for utilities looking for both compliance and cost reduction as regulatory agencies raise penalties for reliability failures.

The integration complexity regarding renewables is driving the need for this market.

The quick inflow of fluctuating solar and wind power is pushing grid operators to minimize inertia while still balancing supply and demand. High-fidelity, real-time simulations from the electrical digital twin project renewable output fluctuation and assess storage dispatch plans under various weather conditions. Digital twins help utilities maximize storage charging schedules and inverter settings, for instance, by simulating a sudden drop in wind speed for a 2024 pilot in the U.K., therefore allowing operators to pre‑position battery supplies and avoid curtailment events during high hours. By modeling distributed energy resources (DER) and assessing grid‑stability metrics, such as voltage deviations and frequency excursions. In experimental deployments, this lowers the demand for expensive spinning reserves and so lowers renewable curtailment, hence raising general renewable utilization rates up to 12%.

The environmental pressure faced by businesses is helping to increase the adoption of this market.

Heavy digital-twin platform investments are driven by ambitious carbon-reduction targets and changing dependability standards. Under the EU's Green Deal, the bloc aims for a 55% cut in net greenhouse‑gas emissions by 2030 versus 1990 levels, a target now projected to be almost met at 54% under present policies. Both the European Green Deal and the U. S. Inflation Reduction Act offer incentives and compliance measures, such as emissions-trading expansions and energy-efficiency initiatives, that urge utilities to accurately benchmark asset performance and report carbon metrics. Their granular emissions models also support scenario planning for decommissioning fossil-fuel plants and integrating renewables in line with regulatory roadmaps. Digital twins enable continuous carbon-footprint tracking for individual transformers, substations, and grid segments, helping operators qualify for tax credits or avoid penalties and facilitating transparent reporting.

The recent advancements in IoT and AI technologies are driving the growth of this market.

Modern twins ingest real‑time feeds from thousands of smart sensors, covering temperature, vibration, and voltage, while AI‑based anomaly‑detection models achieve up to 90% failure‑prediction accuracy, lowering maintenance expenses by 20–30%. Edge analytics gateways preprocess sensor streams locally, ensuring continuity amid intermittent connectivity and minimizing data transmission loads on utility networks. The fusion of pervasive IoT sensor networks with AI‑driven analytics is elevating digital‑twin accuracy and actionable insight. AI-enhanced twins automatically identify variations, such as transformer oil‑temperature spikes or breaker chatter, which enables operators to plan targeted inspections before small problems grow. These features not only increase uptime but also enable condition-based maintenance plans that extend asset lifetimes by 10–15%, therefore providing great operating cost reductions.

Electrical Digital Twin Market Restraints and Challenges:

The existence of high implementation costs is a major drawback for this market as it reduces its adoption rate.

From sensor networks and edge gateways through cloud‑compute infrastructure to custom analytics, deploying an end‑to‑end electrical digital twin typically costs over USD 1 million for a complete substation or distribution network model. This number covers expert services for design, installation, calibration, and preliminary modeling as well as hardware and software licensing. Often, without the capital budgets to take such great initial costs, smaller utilities and rural grid operators are forced to postpone digital‑twin initiatives or limit pilots. Many fundamental assets still need on-premise components, specialized gateways, and secure local compute nodes, driving capex even as DTaaS subscription models develop. The outcome is a bifurcated market: big, well‑funded utilities drive full‑scale deployments, while smaller players wait for prices to fall or scope down to minimum viable twins.

The problem regarding the integration and standardization of the data is a huge market challenge.

One great obstacle is the merging of heterogeneous datasets, SCADA event logs, GIS network maps, asset management records, and third-party weather data into a single digital-twin environment. Though standards like the Common Information Model (CIM IEC 61970/61968) provide a framework, actual grid data often varies from these models, therefore calling for expensive data-cleaning and mapping efforts. Achieving syntactic, structural, and semantic interoperability across systems often demands extensive ETL (extract‑transform‑load) pipelines and bespoke middleware. As twin accuracy depends on high‑quality, well‑governed data, this ETL effort can postpone ROI realization by 6–12 months. Twins cannot provide accurate simulations or predictive insights without perfect data integration, therefore undercutting stakeholder confidence in the technology.

The concerns about the security and privacy of the data and the rising cases of their breach are a great market challenge.

Connecting mission-critical electrical infrastructure to digital twins broadens the attack surface for cyber-threat actors. 72% of utilities see OT-IT convergence as among the top security risks. Digital twins call for bi‑directional data flows between field devices and cloud platforms, therefore necessitating strong encryption (TLS 1.3 or beyond), tight network segmentation, and continuous security‑monitoring tools. Compliance with regulations (NERC CIP in North America, NIS‑2 in the EU) further complicates matters as each asset and its digital equivalent must adhere to rigorous configuration and audit standards. Often requiring committed security staff or third-party managed-security-service contracts, these cybersecurity safeguards increase both project schedules and operating expenses.

The existence of a skill gap in the digital twin engineering sector hampers operational efficiency.

Developing electrical digital twins calls for a rare combination of talents: electrical power systems engineering to simulate electrical behavior, data science knowledge to create predictive algorithms, and software-development experience to realize scalable, resilient architectures. Still, industry studies show a severe lack in such multidisciplinary expertise; 65% of digital twin projects name skill gaps as a major delaying element. Most utilities depend on outside system integrators and consultants since universities and training programs are only now starting to provide specialized curricula in digital‑twin technology. While in-house teams have to go through expensive, time-consuming certifications to handle twins after go-live, this reliance adds 3–6 months to project timelines and drives overall implementation expenses.

Electrical Digital Twin Market Opportunities:

The emergence of edge-to-cloud hybrid twins presents a great growth opportunity for the market.

ABB's real-time artificial intelligence edge twin for power plants demonstrates this; locally performing closed-loop control operations (e.g., protective relay actuation) to avoid risks within milliseconds; meanwhile, model updates back to the cloud enable ongoing learning. Through on‑site anomaly detection and control optimizations, Schneider Electric and IBM's wind‑farm pilots implanted edge servers at turbine sites, cut downtime by 30% and raised energy output by 20%. By processing high‑frequency sensor streams at the edge—aggregating and filtering data, these hybrids reduce cloud egress expenses and protect delicate operational information. This continuum approach broadens digital‑twin applicability across both latency‑sensitive protection tasks and strategic asset‑management use cases, driving wider utility adoption.

The growing use of digital twin as a service (DaaS) is transforming this market at a faster pace.

Through pay-per-use SaaS solutions, subscription-based DTaaS models allow utilities and renewable developers, especially smaller ones without large CAPEX budgets, to have access to ready-made digital-twin capabilities. Instead of buying software licenses and creating back-end infrastructure, consumers choose from pre-configured templates (substation, distribution feeder, PV farm) and pay monthly fees dependent on data volume or analytic module use. Typically including IoT-sensor onboarding, cloud hosting, and continuous software updates, DTaaS offerings reduce implementation times from 12 months to under three. This democratizes access: small municipal utilities and community solar co‑ops can run real‑time simulations, perform "what‑if" DER integration investigations, and receive alerts on asset health without in-house digital‑twin knowledge. Compared to conventional on‑premise implementations, early DTaaS adopters have 40% faster time‑to‑value and 25% reduced overall cost of ownership.

The opportunity to integrate with the digital grid platform is helping the market to develop further.

Coalescing into whole "digital‑grid" suites that link network‑operations dashboards with virtual‑twin analysis are strategic alliances between digital‑twin providers and SCADA/DMS companies. Hitachi Energy's IdentiQ hybrid-cloud twin, for instance, combines flawlessly with its grid-automation control system to let operators see real-time twin models next to live SCADA feeds and GIS overlays. This tight coupling eliminates siloed workflows: grid planners can iterate on substation‑upgrade designs in the twin environment and push validated configurations directly to DMS for automated commissioning. Bentley Systems' combination of its OpenUtilities Digital Twin with live network‑model data likewise lets dispatchers simulate failure scenarios, check protection‑relay settings, and maximize load transfers inside one interface. These end-to-end systems shorten the feedback loop between virtual simulations and actual control-room activities, simplify procedures, and lower human-error risks.

The growing need for predictive maintenance and lifecycle management is said to be a great opportunity for this market.

Moving beyond failure prediction, next-gen electrical digital twins ingest real-time sensor data, maintenance logs, and environmental conditions to compute remaining useful life (RUL) with 85–90% accuracy; utilities using such twins report 15% lower maintenance spend and 10% fewer unplanned outages; they also optimize asset-replacement timing, evaluate refurb ROI, and simulate end-of-life scenarios to reduce overall cost of ownership. To recommend the most cost-effective approach under various budget restrictions, digital twins can simulate several maintenance schedules, testing single‑equipment swaps versus fleet‑wide overhauls. Twins also assist "digital decommission" by demonstrating the effect of asset retirements on network reliability and capacity, hence helping phased retirements to fit with renewable integration strategies. These lifecycle-oriented abilities turn digital twins into strategic decision-support tools for regulatory reporting and capital expenditure planning.

Electrical Digital Twin Market Segmentation:

Market Segmentation: By Product Type

• Digital Power Plant Twin

• Digital Grid Twin

• Digital Substation Twin

• Distribution Network Twin

• Others

The Digital Power Plant Twin is said to dominate this market. The biggest portion came from digital twins of gas- and steam-power plants since operators use them to maximize turbine performance, minimize fuel use, and schedule maintenance for high-MTBF assets. The Digital Grid Twin segment is the fastest-growing segment of the market. Driven by utilities' need for network-wide optimization and renewable-integration scenarios, system-level grid twins, modeling whole transmission and distribution networks, are growing most rapidly.

When it comes to the Twin Digital Substation segment, through virtual commissioning, substation twins (~31% share) modernize aging switchgear and guarantee N‑1 reliability compliance. The Distribution Network Twin segment is gaining momentum with the implementation of smart meters; distribution twins allow DSOs to imagine load flows and prepare feeder updates. The Others segment includes microgrid, EV‑charging‑network, and transformer‑fleet twins in early trial phases.

Market Segmentation: By Deployment Mode

• On-premises

• Cloud

The On-premises segment dominates the market, and the Cloud-based segment is said to be the fastest-growing one. On-premise twins held roughly 60% of the market, favored by major utilities demanding data sovereignty, low-latency control loops, and integration with current SCADA/DMS infrastructure. Offering elastic compute for extensive simulations, centralized data lakes, and flawless cross-site cooperation free of large upfront capex, cloud-based solutions are growing at roughly 16. 2% CAGR.

Market Segmentation: By End-Use Industry

• Utility Service Providers

• Grid Infrastructure Operators

• Renewable Energy

• Manufacturing

• Transportation & Logistics

• Others

The Utility Service Providers segment is the dominant segment here. Over 40% of revenues come from utilities, which use digital twins for predictive outage management, real-time network monitoring, and regulatory compliance. The Grid Infrastructure Operators segment is said to be the fastest-growing segment. Fastest adopters, distribution system operators (DSOs), use twins to control DERs, coordinate grid enhancements, and meet unbundling regulations.

When it comes to the Renewable Energy segment, operators of wind farms and solar plants employ twins for yield prediction, performance benchmarking, and predictive maintenance of inverters and trackers. In the manufacturing sector, the heavy-industry manufacturers are said to use twins to simulate process lines for the optimization of energy-intensive equipment. Under the Transportation & Twin segment, twins help load management and uptime assurance in railroad electrification projects as well as in EV charging networks. The Others segment includes data center power distribution twins and the microgrid controller simulation.

Market Segmentation: By Distribution Channel

Direct OEM Sales

• System Integrators

• Online Platforms

The Direct OEM Sales segment is said to be the dominant one in this market. Leading digital twin companies get big-scale utilities contracts by means of in-house engineering teams and system-integrator partnerships. The System Integrators segment is the fastest-growing. Delivering end-to-end solutions, SIs are the quickest growing channel combining twins with turnkey automation, IoT, and artificial intelligence. Under the Online Platforms segment, through internet portals, emerging DTaaS markets let smaller operators subscribe to pre-configured twin templates and analysis modules.

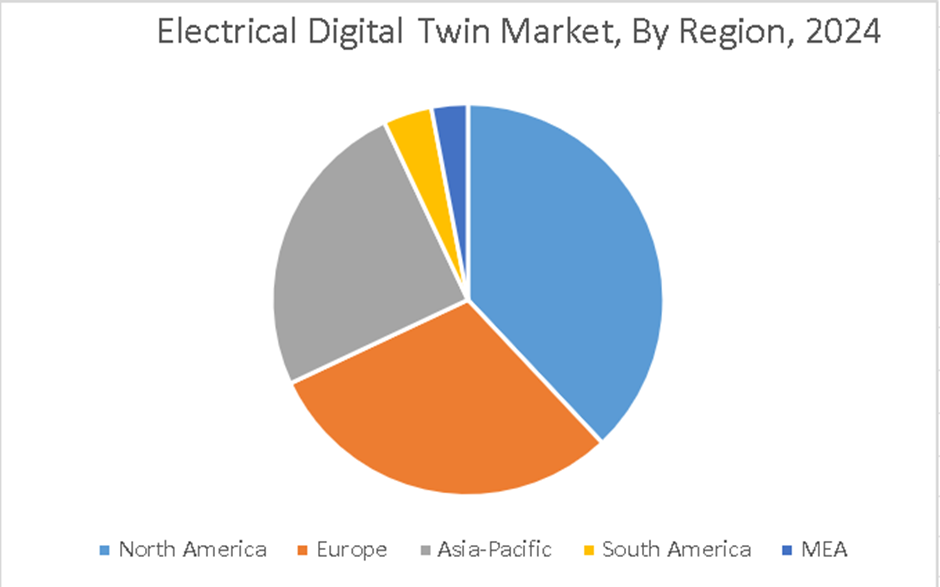

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is said to lead this market. Driven by the fast uptake of cutting-edge technologies in sectors like manufacturing, energy, and utilities, North America is the premier market for electrical digital twins. This expansion is helped by the presence of leading technology companies and a great emphasis on digital transformation projects. The Asia-Pacific region is the fastest-growing region of the market. Particularly in nations like China, Japan, and India, the Asia-Pacific area is expanding quickly. Growing smart cities, industrial automation, and the need for better energy management are fueling demand for electrical digital twins.

Europe is defined by rising investments in Industry 4.0 programs and smart grid technology help Europe to expand noticeably. Leading in adopting digital twin technology to improve operational efficiency and predictive maintenance are nations like Germany, the United Kingdom, and France. The South American market is growing as digital transformation and the advantages of electrical digital twins are becoming more well-known. Brazil, Argentina, and other countries are starting to investigate these techniques to improve their energy and industrial systems. Although the MEA region's market is modest, rising interest in digital twin technology is being shown by governments and companies looking to increase sustainability and efficiency. Adoption is being fueled by investments in smart infrastructure and energy management systems.

COVID-19 Impact Analysis on the Global Electrical Digital Twin Market:

Due to travel restrictions and supply chain bottlenecks, the epidemic interrupted field‑instrumentation activities and postponed sensor‑installation schedules by 3 to 6 months. Utility capital cycles were shortened in 2020, so postponing non‑critical digital twin rollouts. But accelerated remote-operations requirements, targeted at lowering onsite staffing, motivated investments in digital-twin systems for predictive maintenance and virtual asset monitoring. Government incentive programs set aside funds for digital-grid resilience by late 2021, therefore sparking a 20% increase in electrical digital-twin implementations. The crisis highlighted the importance of virtual replicas in guaranteeing operational agility, safety, and company continuity, thus supporting long‑term market expansion.

Latest Trends/ Developments:

Edge servers deployed in substations and wind farms to execute low‑latency twin simulations locally lower cloud dependencies.

Integration of deep‑learning models for anomaly detection, achieving up to 92% accuracy, in streaming sensor data across grid assets.

DTC, or industry partnerships, is fueling standardization projects (IEC 63278–1) to guarantee interoperability and data-model uniformity across providers.

Tests of 5G networks allow millisecond‑level telemetry updates for real-time twin synchronizing in distant renewable locations.

Key Players:

• General Electric (US)

• Siemens (Germany)

• ABB (Switzerland)

• Emerson (US)

• AVEVA Group (UK)

• Schneider Electric (France)

• Microsoft (US)

• Wipro (India)

• SAS Institute (US)

• SAP (Germany)

Chapter 1. Global Electrical Digital Twin Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Electrical Digital Twin Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Electrical Digital Twin Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Electrical Digital Twin Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Electrical Digital Twin Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Electrical Digital Twin Market- By Product Type

6.1. Introduction/Key Findings

6.2. Digital Power Plant Twin

6.3. Digital Grid Twin

6.4. Digital Substation Twin

6.5. Distribution Network Twin

6.6. Others

6.7. Y-O-Y Growth trend Analysis By Product Type

6.8. Absolute $ Opportunity Analysis By Product Type, 2025-2030

Chapter 7. Global Electrical Digital Twin Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. On-Premises

7.3. Cloud

7.4. Y-O-Y Growth trend Analysis By Deployment Mode

7.5. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Electrical Digital Twin Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. Utility Service Providers

8.3. Grid Infrastructure Operators

8.4. Renewable Energy

8.5. Manufacturing

8.6. Transportation & Logistics

8.7. Others

8.8. Y-O-Y Growth trend Analysis By End-Use Industry

8.9. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Electrical Digital Twin Market– By Distribution Channel

9.1. Introduction/Key Findings

9.2. Direct OEM Sales

9.3. System Integrators

9.4. Online Platforms

9.5. Y-O-Y Growth trend Analysis By Distribution Channel

9.6. Absolute $ Opportunity Analysis By Distribution Channel, 2025-2030

Chapter 10. Global Electrical Digital Twin Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product Type

10.1.3. By Deployment Mode

10.1.4. By End-Use Industry

10.1.5. By Distribution Channel

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product Type

10.2.3. By Deployment Mode

10.2.4. By End-Use Industry

10.2.5. By Distribution Channel

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product Type

10.3.3. By Deployment Mode

10.3.4. By End-Use Industry

10.3.5. By Distribution Channel

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Product Type

10.4.3. By Deployment Mode

10.4.4. By End-Use Industry

10.4.5. By Distribution Channel

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Product Type

10.5.3. By Deployment Mode

10.5.4. By End-Use Industry

10.5.5. By Distribution Channel

10.5.6. By Region

Chapter 11. Global Electrical Digital Twin Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. General Electric (US)

11.2. Siemens (Germany)

11.3. ABB (Switzerland)

11.4. Emerson (US)

11.5. AVEVA Group (UK)

11.6. Schneider Electric (France)

11.7. Microsoft (US)

11.8. Wipro (India)

11.9. SAS Institute (US)

11.10. SAP (Germany)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Electrical Digital Twin Market was valued at USD 1.35 billion in 2024 and is projected to reach a market size of USD 2.40 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 12.16%.

The Utility Service Provider segment is said to dominate this market with a market share of about 40%. This is due to streamlining of outage management and optimization of grid reliability.

High sensor‑deployment expenses, complexity of data integration, cybersecurity hazards, and shortage of cross‑domain digital‑twin specialists are some of the major challenges that this market faces.

The pandemic has impacted this market on a large scale. A rise in remote-operation investments, which sped long-term demand for digital-twin solutions, countered early project delays.

Driven by fast renewable integration, grid extensions in China and India, and smart-grid investments across Southeast Asia, Asia Pacific leads with an estimated CAGR of about 17% until 2030.