Global Electric Vehicle Insulation Market Research Report – Segmentation by Product Type (Insulation tapes, Molded insulation housings, Impregnated winding insulations, Potting and casting compounds, Thermal interface materials), Application(Electric traction motors, Battery packs, Power electronics / inverters, Charging equipment, Wiring harnesses), Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-4390

Format:

Region: Global

Market Size and Overview:

The Global Electric Vehicle Insulation Market was valued at USD 1.2 billion in 2024 and will grow at a CAGR of 12% from 2025 to 2030. The market is expected to reach USD 2.11 billion by 2030.

The Electric Vehicle Insulation Market focuses on materials and systems used to electrically isolate, thermally manage, and protect wiring, motors, batteries, and power electronics from heat and electrical faults. This market is experiencing robust growth due to rising EV adoption worldwide, increasing focus on vehicle safety, performance efficiency, and compliance with evolving regulatory standards.

Key market insights:

Global EV sales reached nearly 10 million units in 2024, driving a proportional increase in demand for advanced insulation materials.

Thermally conductive yet electrically insulating materials like mica and silicone composites are being adopted at a rate of 15% year-over-year.

Increased battery pack voltages (800V architecture) require insulation systems with higher dielectric strength, raising R&D budgets by 20%.

Regulations such as UNECE R100 and ISO 6469 are pushing OEMs to use flame-retardant, low-smoke insulation compounds, boosting compliance-driven market value by an estimated USD 0.3 billion.

Lightweight insulation materials like aerogels and thin-film polyimides are gaining traction, potentially reducing vehicle mass by up to 3%, improving EV range by 2–4%.

China accounted for over 45% of global EV insulation demand in 2024, followed by Europe at 25% and North America at 20%.

Repairable and recyclable insulation solutions are entering the aftermarket sector, driven by circular economy trends, expected to grow at a CAGR of 14%.

Strategic partnerships between insulation material suppliers and EV OEMs are supporting custom-tailored material development, increasing contract volumes by 18%.

Global Electric Vehicle Insulation Market Drivers

Thermal management demands in high voltage EV systems is driving the market growth

Advancements in EV powertrain designs have increased battery voltages and motor operating temperatures, necessitating improved thermal management. Insulation must now efficiently dissipate heat while maintaining dielectric strength to prevent arcing and degradation. The shift to 800 V architectures, adopted by leading EV makers such as Porsche and Hyundai, raises operating temperatures and thermal stresses. Conventional insulation materials cannot cope with these new thermal profiles; hence, manufacturers are investing heavily in thermally conductive dielectric composites. These composites often incorporate mica, boron nitride, and silicone fillers that maintain electrical isolation while conducting heat away from hotspots. Enhanced thermal performance extends battery lifespan, reduces cooling system load, and increases overall vehicle efficiency. As global EV production scales, the volume of advanced insulation materials required is expected to increase dramatically. The demand for materials that balance thermal conductivity, electrical insulation, flame retardancy, and manufacturability is driving innovation and investment across the supply chain, propelling market growth.

Regulatory safety frameworks and fire safety requirements is driving the market growth

Global safety regulations increasingly focus on EV fire safety and electric shock protection. Standards such as United Nations Regulation No. 100 (UNECE R100) and ISO 6469 require component-level certification for flame resistance, low smoke emission, and dielectric performance under thermal overload scenarios. These stringent guidelines compel original equipment manufacturers (OEMs) to adopt advanced insulation systems, even at higher cost, to ensure compliance and pass regulatory tests. Failure to meet these standards can result in costly recalls and brand reputation damage. Consequently, suppliers are developing halogen-free, green compound materials, and implementing rigorous testing protocols to demonstrate compliance. The ongoing shift toward more stringent regional regulations—such as China’s GB 38483–2020—creates a continual need for new insulating material grades. These dynamics generate steady procurement pipelines and higher-margin innovation opportunities, reinforcing the insulation market’s growth trajectory.

Rising circular economy pressure in supply chains is driving the market growth

With sustainability high on corporate agendas, both OEMs and regulators are prioritizing end of life material recyclability. Insulation systems are traditionally composed of multiple layered polymers, adhesives, and fillers, making recycling challenging. New eco design initiatives aim to simplify insulation architectures by standardizing material chemistries or enabling modular replacement. This drives innovation in recyclable polyimides, thermoplastic elastomers, and bio-based masterbatches that can be separated and reprocessed. Suppliers are forming joint ventures with recyclers to develop take back and reuse pathways for high value insulation waste. Cost benefit analyses reveal that recyclable systems can reduce total lifecycle cost by 10 % and carbon footprint by up to 15 %. These environmental and economic incentives are motivating procurement teams to adopt circular insulation products in fleet and commercial vehicle segments, further expanding the market.

Global Electric Vehicle Insulation Market Challenges and Restraints

Balancing dielectric strength and environmental resilience is restricting the market growth

Insulation materials in EVs must resist electrical breakdown while withstanding harsh mechanical, thermal, and chemical environments. Achieving high dielectric strength often involves dense fillers such as alumina or silica, which increase stiffness and reduce flexibility. This creates a tradeoff: materials that insulate well may crack under vibration or temperature cycling, compromising reliability. Stringent humidity and immersion tests (e.g., IP67-rated systems) further complicate formulation. Suppliers frequently face formulation lead times of 12–18 months to fine-tune material compositions. Any deviation may void component certifications or invalidate crash safety compliance. OEMs require assurances through accelerated lifecycle testing, increasing development costs. As the industry pushes lower costs and faster time-to-market, the lengthy material qualification process acts as a bottleneck, slowing adoption of advanced insulation systems and challenging smaller players who lack extensive testing infrastructure.

Supply chain dependency and raw materials volatility is restricting the market growth

Electric vehicle insulation relies on specialty polymers, fillers, and chemical additives sourced from limited suppliers, often headquartered in Japan, Europe, or China. The mica, silicone, and polyimide supply is especially fragmented. Any disruption—including trade policy shifts, natural disasters, or raw-material price spikes—can lead to significant lead-time increases and price volatility. For instance, a 2023 surge in silicone precursor costs increased insulation material pricing by 8–12%, squeezing margins for component manufacturers. OEMs, meanwhile, are under pressure to reduce EV costs to meet competitive vehicle pricing targets. This volatility forces them to overstock, increasing inventory carry costs, or periodically redesign insulation systems around available inputs, slowing development. Establishing regional supply chains with inventory buffers and dual sourcing is a costly process and takes years to implement. Until then, insulation system suppliers remain vulnerable to market shocks.

High barrier to entry in insulation product innovation is restricting the market growth

Developing next-gen insulation materials demands deep expertise in polymer chemistry, electrics, and thermal dynamics, backed by lab and field validation. The R&D investment to design custom insulation tapes, molded housings, or impregnated winding systems runs into millions. OEMs increasingly set high technical benchmarks via joint programs and impose long qualification cycles with certified testing partners, raising entry barriers for newcomers. Furthermore, incumbent suppliers hold key patents on processing methods and formulations, creating legal hurdles. New entrants with disruptive but untested technologies struggle to gain OEM trust. Without codevelopment partnerships or proof-of-concept pilots, they often cannot access EV platforms. As a result, insulation material innovation is led by a handful of multinational chemical companies and tier 1 automotive suppliers, limiting competition and potentially slowing the pace of diversity in material types.

Market Opportunities

The Electric Vehicle Insulation Market presents several high-potential avenues, driven by escalating EV penetration, technological innovation, and evolving value chains. Aerogel-based insulation systems have emerged as a top opportunity. These nanostructured materials offer extremely low thermal conductivity combined with high dielectric strength, allowing design engineers to reduce insulation thickness by 30–50%. Thinner insulation saves vehicle weight—improving range—and opens packaging flexibility. A recent collaboration between an aerogel specialist and a Chinese EV OEM reported range improvements of up to 5% in test vehicles. Advanced manufacturing techniques, such as 3D printing of insulation molds, also enable part consolidation—reducing assembly complexity and labor costs while enabling customization for different motor and battery designs. This trend supports the move toward platform standardization across vehicle families. Another significant opportunity lies in digital material modeling and simulation tools for electric insulation, employing finite element analysis alongside artificial intelligence. These tools can predict thermal and electrical behavior under various operating conditions, accelerating qualification cycles and reducing bench-testing requirements by 40%. They also permit rapid iteration of material blends customized for specific climates, from arctic to desert environments. Insulation suppliers integrating these digital tools are differentiating themselves by offering turnkey solutions rather than component-only sales, increasing customer stickiness and enabling premium pricing. The aftermarket segment, historically underdeveloped, is gaining importance as EVs age. Insulation failures due to electrical wear, moisture ingress, or collision damage are rising. This has created demand for repair kits and retrofit insulation systems, especially in commercial fleets (e buses, delivery vehicles) where downtime is costly. Suppliers can tap into this with branded repair offerings, backed by training programs for repair technicians. From an environmental standpoint, insulated material recovery programs tied to battery recycling are also emerging. By reusing insulation-grade polymers or converting them into lower-value products, OEMs and recyclers create new value chains, reducing disposal costs and contributing to circular-economy targets. As global EV fleets grow, these service and sustainability-led opportunities are expected to contribute significant long-term revenue streams while reinforcing brand value with eco-conscious end-users.

Market segmentation

By Products

• Insulation tapes

• Molded insulation housings

• Impregnated winding insulations

• Potting and casting compounds

• Thermal interface materials

Insulation tapes represent the most dominant product segment, accounting for approximately 40 % of the market by revenue in 2024. Their ease of application across motors, harnesses, and battery modules, alongside availability in various dielectric strengths and thermal ratings, makes them preferred by OEMs. They also facilitate rapid prototyping and flexible winding insulation, speeding assembly line integration. Tape substrates like polyester, polyimide (Kapton), and mica further offer specialty flame-retardant and high-temperature grades. The combination of cost-effectiveness, broad compatibility, and ease of supply chain sourcing solidifies insulation tapes’ dominance. Advanced tape formulations, such as pressure-sensitive polyimide tapes with nano fillers, are enabling performance improvements, reaffirming this segment’s lead position.

By Application

• Electric traction motors

• Battery packs

• Power electronics / inverters

• Charging equipment

• Wiring harnesses

Electric traction motors remain the most dominant application, capturing around 35 % of insulation market share in 2024. Motor insulation systems must withstand high voltage levels, frequent thermal cycling, and mechanical vibration, making them the largest single consumer of specialized insulation materials. As EV OEMs push for higher power densities and compact motor designs, demand for thin yet high-performance insulating solutions increases. Motor insulation is also the most standardized part of vehicle electronics, benefiting from established production volumes and rigorous qualification cycles. Additionally, a significant share of motors is supplied by Tier-1 partners, enabling scale efficiencies and long-term contracts. These dynamics position motor insulation as the largest application category in the EV insulation landscape.

Regional Segmentation

• North America

• Asia Pacific

• Europe

• South America

• Middle East & Africa

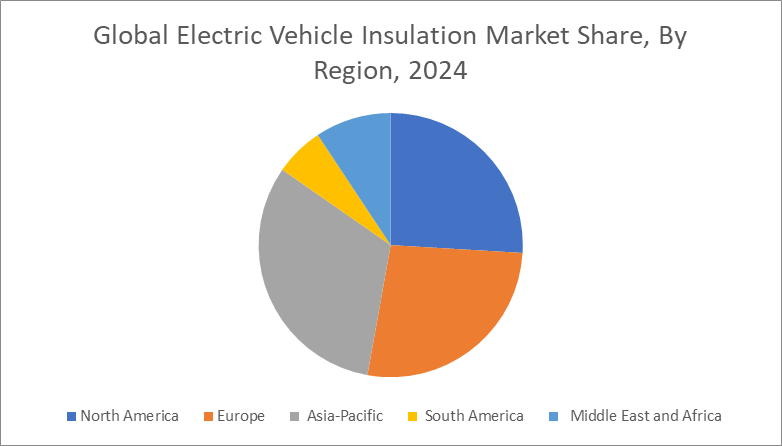

The dominant region is Asia Pacific, particularly China. In 2024, the Asia Pacific region accounted for over 50 % of global demand for EV insulation materials, driven by the region’s massive EV production volumes and supportive industrial infrastructure. China alone manufactured more than 7 million EVs in 2024, creating a huge, localized ecosystem of insulation-tape, resin, and polymer suppliers. Regional material engineers collaborate with OEMs on custom dielectric compounds adapted for local cell chemistries and thermal profiles. Additionally, government policies — such as subsidies for domestic component sourcing and R&D incentives — strengthen local supply chains. Adoption of advanced insulation systems in Chinese OEMs is among the highest globally, with manufacturers investing in next gen materials ahead of Western counterparts. South Korea and Japan also contribute strong technical innovation and material exports. The combination of production scale, regulatory alignment, and localized manufacturing positions Asia Pacific as the clear market leader in EV insulation.

COVID 19 Impact Analysis on the Electric Vehicle Insulation Market

The COVID-19 pandemic disrupted supply chains and manufacturing capacity across the EV insulation market, particularly in the early 2020 equal to 2020. Lockdowns in China and Southeast Asia led to temporary factory closures, delaying shipments of key raw materials such as mica, silicone, and specialty polymers. This resulted in a 15% extension in lead times for insulation tape grades and potting compounds. With reduced supply, OEMs were forced to adjust production schedules and shift sourcing to secondary suppliers, often at higher cost. However, stimulus packages and renewed investment in electric mobility helped a gradual rebound in late 2021, with insulation demand recovering to 2020 pre pandemic levels by mid 2022. The crisis highlighted vulnerabilities due to single region sourcing; many companies began building dual source strategies and regional warehousing to mitigate future disruptions. Accelerated digitization in supply chain management, with real time inventory monitoring and AI forecasting, became widespread among tier 1 insulation suppliers. Lockdowns also delayed new EV model launches, reducing short term insulation demand; yet, pent up vehicle demand post COVID resulted in 2023–2024 insulation consumption growth rates exceeding pre pandemic averages. In summary, while the pandemic disrupted production and highlighted supply risks, it also drove investment in resilience, digital capabilities, and local sourcing—setting the foundation for stronger long term growth in the EV insulation market.

Latest trends/Developments

Recent developments in the EV insulation market illustrate a shift toward multifunctional materials, digital integration, and sustainability. Companies are launching hybrid insulation systems combining thermal management with sensors—integrating fiber-optic temperature or moisture sensors into insulation tapes or molded housings. This real-time monitoring addresses safety and performance optimization needs. Additionally, manufacturers are introducing bio-based polyimide precursors and halogen-free synergies in potting compounds, reducing environmental impact and labeling them eco-friendly to appeal to green-conscious OEMs. Advancements in vacuum-pressure impregnation (VPI) for motor coils allow precise resin control, reducing porosity and improving dielectric breakdown resistance by up to 25%. Digital twins are also being used for new material qualification, shortening development cycles from 18 to 12 months. On the supply chain side, tier-1 suppliers are collaborating on blockchain traceability for insulation materials to ensure compliance and provenance. Finally, additive manufacturing is gaining traction: insulation houses and motor endcaps are being 3D printed using dielectric polymer blends, enabling rapid customization for new EV platforms. These trends—sensor integration, green materials, digital models, and additive manufacturing—collectively point toward smarter, lighter, and more sustainable insulation solutions shaping the future EV market.

Key Players:

• Saint Gobain

• 3M

• Kaneka Corporation

• Henkel AG & Co. KGaA

• Parker Hannifin Corporation

• DuPont de Nemours, Inc.

• Asahi Kasei Corporation

• Taiyo Kogyo Corporation

• Henchman & Co.

• ParkerBaldwin International

Chapter 1. Global Electric Vehicle Insulation Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Electric Vehicle Insulation Market – Executive Summary

2.1. Market Size & Forecast – (2025–2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Electric Vehicle Insulation Market – Competitive Landscape

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Strategic Alliances, M&A, Joint Ventures

3.4. Vendor Mapping & Ecosystem Overview

Chapter 4. Global Electric Vehicle Insulation Market Entry Scenario

4.1. Regulatory Landscape

4.2. Key Start-up Case Studies

4.3. Customer Adoption & Analysis

4.4. PESTLE Analysis

4.5. Porter’s Five Forces Analysis

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Power of Buyers

4.5.3. Threat of New Entrants

4.5.4. Threat of Substitutes

4.5.5. Industry Rivalry

Chapter 5. Global Electric Vehicle Insulation Market – Key Market Dynamics

5.1. Market Drivers

5.2. Market Restraints

5.3. Market Opportunities

5.4. Emerging Technologies & Innovations

Chapter 6. Global Electric Vehicle Insulation Market – By Products

6.1. Insulation Tapes

6.2. Molded Insulation Housings

6.3. Impregnated Winding Insulations

6.4. Potting and Casting Compounds

6.5. Thermal Interface Materials

6.6. Y-o-Y Growth Analysis by Products

6.7. Absolute $ Opportunity by Products (2025–2030)

Chapter 7. Global Electric Vehicle Insulation Market – By Application

7.1. Electric Traction Motors

7.2. Battery Packs

7.3. Power Electronics / Inverters

7.4. Charging Equipment

7.5. Wiring Harnesses

7.6. Y-o-Y Growth Analysis by Application

7.7. Absolute $ Opportunity by Application (2025–2030)

Chapter 8. Global Electric Vehicle Insulation Market – Regional Analysis

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Products

8.1.3. By Application

8.1.4. Country-level Attractiveness

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Products

8.2.3. By Application

8.2.4. Country-level Attractiveness

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia Pacific

8.3.2. By Products

8.3.3. By Application

8.3.4. Country-level Attractiveness

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Products

8.4.3. By Application

8.4.4. Country-level Attractiveness

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. UAE

8.5.1.2. Saudi Arabia

8.5.1.3. South Africa

8.5.1.4. Nigeria

8.5.1.5. Egypt

8.5.1.6. Kenya

8.5.1.7. Rest of MEA

8.5.2. By Products

8.5.3. By Application

8.5.4. Country-level Attractiveness

Chapter 9. Global Electric Vehicle Insulation Market – Company Profiles

(Overview, Product Portfolio, Financials, Strategies & SWOT)

9.1. Saint Gobain

9.2. 3M

9.3. Kaneka Corporation

9.4. Henkel AG & Co. KGaA

9.5. Parker Hannifin Corporation

9.6. DuPont de Nemours, Inc.

9.7. Asahi Kasei Corporation

9.8. Taiyo Kogyo Corporation

9.9. Henchman & Co.

9.10. ParkerBaldwin International

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Electric Vehicle Insulation Market was valued at USD 1.2 billion in 2024 and will grow at a CAGR of 12% from 2025 to 2030. The market is expected to reach USD 2.11 billion by 2030.

Key drivers include thermal management needs, safety regulation compliance, and circular economy pressures.

Segments include insulation tapes, molded housings, winding insulations, potting compounds, and thermal interface materials; applications cover motors, batteries, electronics, charging equipment, wiring harnesses.

Asia Pacific, particularly China, leads the market with over 50% share due to high EV production and local supply chains.

Leading players include Saint Gobain, 3M, Kaneka Corporation, Henkel, Parker Hannifin, DuPont, Asahi Kasei, and Taiyo Kogyo.