Electric Vehicle Infrastructure Market Research Report -- Segmentation by Charging Type (AC Charging, DC Fast Charging); By Connector Type (CHAdeMO, CCS, Tesla Supercharger, Type 2, Others); By Installation Type (Public, Private); By Application (Commercial, Residential); By Vehicle Type (Battery Electric Vehicle, Plug-in Hybrid Electric Vehicle); Region - Forecast (2025 - 2030)

Published: 2025 - June

Report Code: IM-16567

Format:

Region: Global

Market Size and Overview:

The Electric Vehicle Infrastructure Market was valued at USD 31.87 billion in 2024 and is projected to reach a market size of USD 104.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 26.8%.

Electric Vehicle Infrastructure represents the backbone of the electric mobility ecosystem, encompassing charging stations, battery swapping facilities, and supporting electrical grid infrastructure necessary to power electric vehicles. This rapidly evolving sector has emerged as a critical enabler of transportation electrification in the 21st century, with governments, utilities, and private companies investing heavily in building comprehensive charging networks. As the automotive industry undergoes its most significant transformation since the introduction of the assembly line, the development of robust EV infrastructure has become essential for supporting the mass adoption of electric vehicles and achieving global climate objectives.

Key Market Insights:

According to the International Energy Agency's Global EV Outlook 2022, there were approximately 1.8 million public charging points worldwide, representing a 37% increase from the previous year. However, research indicates that achieving widespread EV adoption requires a ratio of one public charging point per 10-15 electric vehicles, suggesting the need for approximately 15 million public charging points by 2030 to support projected EV sales volumes.

A comprehensive survey conducted by McKinsey & Company involving 3,000 EV owners across 15 countries revealed that 67% of respondents identified charging infrastructure availability as the primary factor influencing their vehicle purchase decision. Additionally, 78% of potential EV buyers stated they would be more likely to purchase an electric vehicle if charging time could be reduced to under 15 minutes, driving significant investment in ultra-fast charging technologies.

Market analysis from BloombergNEF indicates that global investment in EV charging infrastructure reached USD 14.2 billion in 2022, with China accounting for 52% of total investments, followed by Europe at 31% and North America at 12%. The study projects that cumulative infrastructure investment will need to reach USD 620 billion by 2040 to support the anticipated growth in electric vehicle adoption across all market segments.

Electric Vehicle Infrastructure Market Drivers:

Government initiatives, regulatory mandates, and substantial public investment programs are fundamentally transforming the electric vehicle infrastructure landscape and accelerating market growth across all geographic regions.

Governments worldwide have implemented comprehensive policy frameworks that combine regulatory mandates, financial incentives, and direct infrastructure investments to accelerate EV adoption and charging network development. The European Union's Green Deal includes EUR 1 trillion in climate investments, with significant portions allocated to transportation electrification and charging infrastructure development. Similarly, the United States Infrastructure Investment and Jobs Act allocated USD 7.5 billion specifically for EV charging infrastructure, aiming to establish a national network of 500,000 charging stations by 2030. China's 14th Five-Year Plan includes targets for 20 million charging points by 2025, supported by substantial government subsidies and streamlined permitting processes. These policy initiatives extend beyond financial support to include regulatory requirements such as California's Advanced Clean Cars II rule, which mandates 100% zero-emission vehicle sales by 2035, and the European Union's proposed ban on internal combustion engine sales by 2035. Additionally, many jurisdictions have implemented building codes requiring EV charging readiness in new construction, with states like California requiring 20% of parking spaces in new apartment buildings to be EV-ready.

The dramatic expansion of electric vehicle production capacity and the introduction of affordable EV models across multiple market segments are creating unprecedented demand for supporting charging infrastructure.

Global automakers have committed over USD 330 billion to electric vehicle development and manufacturing capacity expansion through 2030, with production capacity expected to exceed 30 million units annually by the end of the decade. This massive scaling of EV production is being accompanied by significant improvements in battery technology, with average battery costs declining by 85% over the past decade and continuing to fall at approximately 8% annually. The introduction of mass-market EVs priced below USD 30,000, combined with improving range capabilities now exceeding 300 miles for many models, is expanding the addressable market beyond early adopters to mainstream consumers. Major automotive manufacturers including General Motors, Ford, Volkswagen, and Stellantis have announced plans to transition to predominantly electric lineups within the next 15 years, creating predictable demand for charging infrastructure investments. The emergence of electric commercial vehicles, including delivery vans, trucks, and buses, is creating additional infrastructure requirements, particularly for depot charging and highway corridor fast-charging networks capable of supporting heavy-duty applications.

Electric Vehicle Infrastructure Market Restraints and Challenges:

Despite strong growth prospects, the electric vehicle infrastructure market faces significant challenges that could impact deployment timelines and adoption rates. Grid capacity constraints represent a critical bottleneck, with many electrical distribution systems requiring substantial upgrades to support high-power charging installations, particularly in dense urban areas and along highway corridors. Permitting and regulatory approval processes remain complex and time-consuming, with average installation timelines ranging from 12-24 months for public charging stations due to utility interconnection requirements and local zoning approvals. High upfront capital costs for infrastructure deployment, particularly for DC fast charging stations that can cost USD 150,000-500,000 per installation, create financial barriers for many potential operators. Technical standardization challenges persist across different charging protocols and connector types, creating consumer confusion and limiting interoperability between networks.

Electric Vehicle Infrastructure Market Opportunities:

The electric vehicle infrastructure market presents substantial opportunities across multiple dimensions as the transition to electric mobility accelerates globally. Workplace charging represents a significant growth opportunity, with only 8% of U.S. employers currently offering charging facilities despite 67% of employees expressing interest in this benefit. Multi-unit dwelling charging solutions address the critical need for residential charging access among the 40% of Americans who live in apartments or condominiums without dedicated parking. Highway corridor charging networks present opportunities for high-utilization installations that can achieve faster payback periods and support long-distance travel adoption. Vehicle-to-grid technology integration offers additional revenue opportunities by enabling charging stations to provide grid services such as load balancing and energy storage. The electrification of commercial fleets, including last-mile delivery, ride-sharing, and public transit, creates predictable demand patterns that support infrastructure investment decisions. Rural and underserved community charging networks represent both a social equity opportunity and a market expansion possibility, particularly with government funding support.

Electric Vehicle Infrastructure Market Segmentation:

Market Segmentation: By Charging Type

• AC Charging

• DC Fast Charging

In 2024, AC charging dominated the global electric vehicle infrastructure market with approximately 78.4% revenue share, primarily due to its lower installation costs and widespread applicability for residential and workplace charging applications. AC charging stations, typically ranging from 3.7kW to 22kW power levels, are cost-effective solutions for overnight charging and locations where vehicles remain parked for extended periods. The prevalence of AC charging reflects the current charging behavior patterns where most EV owners conduct primary charging at home or work locations.

DC fast charging represents the fastest-growing segment with a projected CAGR of 31.7% during the forecast period. This accelerated growth is driven by the need for rapid charging capabilities that can provide 80% battery capacity in 15-30 minutes, essential for highway travel and commercial applications. DC fast charging stations, ranging from 50kW to 350kW power levels, command higher installation costs but generate greater revenue per session, making them attractive for commercial operators in high-traffic locations.

Market Segmentation: By Connector Type

• CHAdeMO

• CCS (Combined Charging System)

• Tesla Supercharger

• Type 2

• Others

The CCS (Combined Charging System) connector emerged as the dominant standard in 2024, accounting for 43.2% of the market share globally. CCS has gained widespread adoption due to its support by major European and American automakers and its ability to handle both AC and DC charging through a single connector interface. The European Union's mandate requiring CCS compatibility for all public charging stations has further accelerated its adoption across European markets.

Tesla Supercharger connectors represent a significant market segment with 28.7% share, supported by Tesla's extensive proprietary charging network and high customer satisfaction ratings. However, Tesla's recent decision to open its Supercharger network to other manufacturers and adopt CCS standards in new installations is expected to reshape connector market dynamics. The CHAdeMO standard, primarily used by Japanese manufacturers, maintains a strong presence in Asian markets but faces declining adoption in Western markets as automakers transition to CCS compatibility.

Market Segmentation: By Installation Type

• Public

• Private

Public charging installations accounted for 61.8% of the market share in 2024, driven by the need for accessible charging networks that support vehicle adoption among consumers without private parking access. Public charging includes both publicly accessible commercial stations and government-operated facilities, with locations ranging from retail centers and parking garages to highway rest stops and urban street charging.

Private charging installations are projected to grow at the fastest rate during the forecast period, with a CAGR of 29.3%. This growth is driven by increasing workplace charging installations, fleet depot charging requirements, and residential charging among single-family homeowners. Private installations typically offer lower charging costs and guaranteed availability, making them attractive for regular users with predictable charging patterns.

Market Segmentation: By Application

• Commercial

• Residential

The commercial segment dominated the market with 67.4% share in 2024, encompassing public charging networks, workplace charging, and fleet charging applications. Commercial installations typically feature higher power levels, multiple charging ports, and sophisticated payment and network management systems. This segment benefits from higher utilization rates and revenue generation potential compared to residential applications.

The residential segment is anticipated to experience significant growth as EV adoption expands beyond early adopters to mainstream consumers. Home charging represents the most convenient and cost-effective charging solution for daily commuting needs, with residential installations typically ranging from 3.7kW to 11kW power levels. Government incentives and utility rebate programs are making residential charging installations more accessible and affordable for homeowners.

Market Segmentation: By Vehicle Type

• Battery Electric Vehicle (BEV)

• Plug-in Hybrid Electric Vehicle (PHEV)

Battery Electric Vehicles drove 74.6% of infrastructure demand, reflecting the higher charging frequency requirements of vehicles that rely entirely on electric power. BEVs typically require more frequent charging sessions and benefit from both AC and DC charging capabilities, driving demand for diverse charging infrastructure types across different use cases and locations.

Plug-in Hybrid Electric Vehicles represent a significant but smaller portion of infrastructure demand, accounting for 25.4% of market share. PHEVs typically require less frequent charging due to their internal combustion engine backup, but their adoption has contributed to overall charging network utilization and helped justify infrastructure investments during the early stages of market development.

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

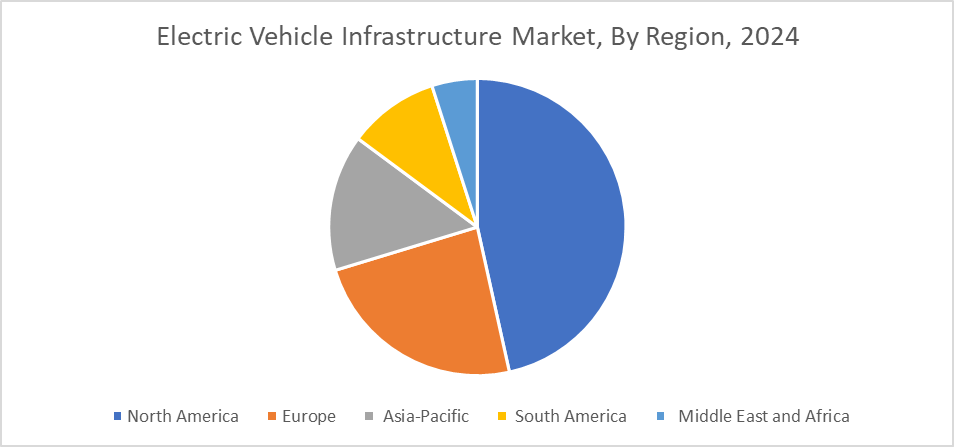

Asia-Pacific and America led the global electric vehicle infrastructure market with 48.7% revenue share, driven primarily by China's massive investment in charging infrastructure and supportive government policies. China alone accounts for approximately 85% of global public charging points, with over 1.5 million public charging stations installed. The region's dominance is further supported by strong EV manufacturing capabilities and comprehensive government support for electrification initiatives.

Europe is projected to witness the highest growth rate during the forecast period, with a CAGR of 32.1%. The European Union's Green Deal and Fit for 55 package include ambitious targets for charging infrastructure deployment, with plans for at least one charging point every 60 kilometers along major highways by 2025. Countries like Norway, Netherlands, and Germany are leading deployment efforts with comprehensive national charging networks and supportive regulatory frameworks.

COVID-19 Impact Analysis on the Global Electric Vehicle Infrastructure Market:

The COVID-19 pandemic initially disrupted electric vehicle infrastructure deployment due to supply chain constraints, permitting delays, and reduced mobility patterns that decreased charging station utilization. Many planned installations were postponed as operators focused on preserving cash flow during the uncertain economic environment. However, the pandemic ultimately accelerated long-term infrastructure development as governments incorporated EV charging investments into economic recovery packages and stimulus programs.

Latest Trends/ Developments:

Ultra-fast charging technology advancement is revolutionizing the infrastructure landscape, with manufacturers developing 350kW+ charging systems capable of adding 200 miles of range in under 10 minutes. Companies like Ionity, Electrify America, and Tesla are deploying these next-generation systems along major highway corridors, addressing range anxiety concerns and enabling long-distance EV travel comparable to conventional vehicles.

Vehicle-to-grid integration and bidirectional charging capabilities are emerging as significant value propositions for infrastructure operators and utility companies. Ford's F-150 Lightning and other vehicles now offer vehicle-to-home capabilities, while pilot programs in California and Europe are demonstrating the potential for EVs to provide grid services including peak load management and renewable energy storage integration.

Key Players:

• BTC Power

• Tesla Inc

• ABB Ltd

• Delta Electronics

• Bp Puls

• Tritium DCFC Ltd

• Siemens

• Schneider Electric

• Eaton Corp

• Webasto Group

Chapter 1. Electric Vehicle Infrastructure Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Electric Vehicle Infrastructure Market – Executive Summary

2.1. Market Installation Type & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Electric Vehicle Infrastructure Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Electric Vehicle Infrastructure Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Electric Vehicle Infrastructure Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Electric Vehicle Infrastructure Market – By Charging Type

6.1. Introduction/Key Findings

6.2. AC Charging

6.3. DC Fast Charging

6.4. Y-O-Y Growth trend Analysis By Charging Type

6.5. Absolute $ Opportunity Analysis By Charging Type, 2025-2030

Chapter 7. Electric Vehicle Infrastructure Market – By Connector Type

7.1. Introduction/Key Findings

7.2. CHAdeMO

7.3. CCS

7.4. Tesla Supercharger

7.5. Y-O-Y Growth trend Analysis By Connector Type

7.6. Absolute $ Opportunity Analysis By Connector Type, 2025-2030

Chapter 8. Electric Vehicle Infrastructure Market – By Installation Type

8.1. Introduction/Key Findings

8.2. Public

8.3. Private

8.4. Y-O-Y Growth trend Analysis By Installation Type

8.5. Absolute $ Opportunity Analysis By Installation Type, 2025-2030

Chapter 9. Electric Vehicle Infrastructure Market – By Application

9.1. Introduction/Key Findings

9.2. Commercial

9.3. Residential

9.4. Y-O-Y Growth trend Analysis By Application

9.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 10. Electric Vehicle Infrastructure Market – By Vehicle Type

10.1. Introduction/Key Findings

10.2. Battery Electric Vehicle

10.3. Plug-In Hybrid EV

10.4. Y-O-Y Growth trend Analysis By Vehicle Type

10.5. Absolute $ Opportunity Analysis By Vehicle Type, 2025-2030

Chapter 11. Electric Vehicle Infrastructure Market, By Geography – Market Installation Type, Forecast, Trends & Insights

11.1. North America

11.1.1. By Country

11.1.1.1. U.S.A.

11.1.1.2. Canada

11.1.1.3. Mexico

11.1.2. By Charging Type

11.1.3. By Connector Type

11.1.4. By Installation Type

11.1.5. By Application

11.1.6. By Vehicle Type

11.1.7. Countries & Segments – Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Charging Type

11.2.3. By Connector Type

11.2.4. By Installation Type

11.2.5. By Application

11.2.6. By Vehicle Type

11.2.7. Countries & Segments – Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.1. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Charging Type

11.3.3. By Connector Type

11.3.4. By Installation Type

11.3.5. By Application

11.3.6. By Vehicle Type

11.3.7. Countries & Segments – Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Charging Type

11.4.3. By Connector Type

11.4.4. By Installation Type

11.4.5. By Application

11.4.6. By Vehicle Type

11.4.7. Countries & Segments – Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.8. Egypt

11.5.1.9. Rest of MEA

11.5.2. By Charging Type

11.5.3. By Connector Type

11.5.4. By Installation Type

11.5.5. By Application

11.5.6. By Vehicle Type

11.5.7. Countries & Segments – Market Attractiveness Analysis

Chapter 12. Electric Vehicle Infrastructure Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

12.1. BTC Power

12.2. Tesla Inc

12.3. ABB Ltd

12.4. Delta Electronics

12.5. Bp Puls

12.6. Tritium DCFC Ltd

12.7. Siemens

12.8. Schneider Electric

12.9. Eaton Corp

12.10. Webasto Group

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Electric Vehicle Infrastructure Market was valued at USD 31.87 billion in 2024 and is projected to reach a market size of USD 104.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 26.8%.

Government initiatives, regulatory mandates, and substantial public investment programs are the primary drivers propelling the global electric vehicle infrastructure market.

Based on Charging Type, the Global Electric Vehicle Infrastructure Market is segmented into AC Charging and DC Fast Charging.

Asia-Pacific is the most dominant region for the Global Electric Vehicle Infrastructure Market.

Tesla Inc., ChargePoint Holdings Inc., EVgo Services LLC, and Electrify America LLC are the key players operating in the Global Electric Vehicle Infrastructure Market.