Global Electric Commercial Vehicle Market Research Report – Segmentation By Vehicle Type (Electric Trucks, Electric Vans, Electric Buses); By Propulsion Type (Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Fuel Cell Electric Vehicles); By End-Use Application (Last-Mile Delivery, Distribution & Logistics, Public Transport, Municipal Services); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-4351

Format:

Region: Global

Market Size and Overview:

The Electric Commercial Vehicle Market was valued at USD 59.23 billion in 2024 and is projected to reach a market size of USD 166.28 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.93%.

The Electric Commercial Vehicle market is rapidly reshaping the future of global transport due to an aggressive push for sustainability, stringent emission regulations, and expensive fuel prices. Today, from delivery vans to city buses and heavy-duty trucks, businesses around the world have found electric alternatives for their fleets to save operating expenses and achieve environmental goals. With newer technologies evolving into less costly batteries with longer ranges, commercial electric fleets are slowly turning into a real picture rather than a dream, hence, ushering in a new era of clean, efficient, and noiseless commercial transport.

Key Market Insights:

Electric commercial vehicles have shown a 30–50% reduction in maintenance costs compared to their diesel counterparts. With fewer moving parts and no engine oil or exhaust systems, fleet uptime improves dramatically. This translates into higher operational efficiency and lower lifetime expenses.

Electric buses and delivery vehicles can reduce urban CO₂ emissions by up to 75%. In addition to cleaner air, they lower noise pollution, enhancing city livability. Municipalities worldwide are introducing incentives and restrictions to accelerate this transition.

Electric Commercial Vehicle Market Drivers:

One of the most significant drivers accelerating the adoption of electric commercial vehicles is the tightening global emission regulations.

The pressure of tightening global emission regulations sustains one of the most significant drivers for the adoption of electric commercial vehicles. All around the world, governments are enacting tighter CO₂ and NOx emission limits to address climate change and improve urban air quality. Cities like London, Paris, and New Delhi are now implementing low-emission or zero-emission zones in which only electric or clean vehicles are permitted to operate, thereby hastening the transition of fleet operators to electric options. Government support is also extending to attractive incentives in terms of subsidies, tax rebates, and reduced registration fees to electrify fleets. China's aggressive new energy vehicle mandates are rapidly accelerating electric fleet penetration. In addition, conforming to ESG (environmental, social, and governance) norms has become imperative for companies wishing to preserve their reputational standing in the marketplace and to maintain investor confidence. Consequently, sustainability commitments now have a pronounced impact on procurement strategies in the logistics, retail, and public transportation sectors. Thus far, a strong regulatory thrust will likely continue driving demand for electric commercial vehicles over the next decade.

Another major factor fueling the growth of electric commercial vehicles is their substantially lower operating costs compared to diesel and petrol counterparts.

Another reason behind the propulsion of electric commercial vehicles is that they are highly cost-effective in running. Electric vehicles have fewer moving parts compared to petrol and diesel engines, so the engine does not need much maintenance, which includes costly oil changes, an exhaust system, and engine maintenance. Maintenance costs have been reduced by fleet owners maintaining up to 50 percent of the traditional fuel's maintenance costs, which increases the uptime and reliability of vehicular operations. Again, electricity as a fuel is cheaper and far more predictable than diesel or gasoline, thus allowing better control of costs over relatively longer periods for the operators. It has also enabled companies to integrate renewable energy sources into their charging infrastructure for further reduction in energy cost and carbon footprint. As fuel prices vary greatly, and emission penalties are expected to rise, the strong economic case provides a good argument for businesses working towards savings in operations, following this long-term economic justification of ECVs. Economic advantages such as these are converting electric commercial vehicles from being niche pilot projects to a 'common fleet solution' in no time across the globe.

Electric Commercial Vehicle Market Restraints and Challenges:

Despite rapid advancements in battery technology and growing enthusiasm for fleet electrification, the limited availability of robust charging infrastructure remains one of the most critical challenges for the electric commercial vehicle market.

The electric CV market in the wake of fleet electrification seems to be buoyed with a vigorous atmosphere created by rapid advancements in battery technology, but the scant availability of robust charging infrastructures still holds the prime challenge. Many regions still lack developed fast-charging stations to cater to large commercial fleets, particularly in developing countries and rural settings. The huge cost of investment to set up a depot or dedicated fleet charging infrastructure further denies a smooth entry to small and medium enterprises into the arena. Last but not least, many regions having less robust yet aging power grids fear that the sudden additional load coming from commercial fleets could destabilize their utilities and even cause downtime. Further complex coordination, planning, capitalization, and regulation hurdles await in terms of upgrading the grids and installing chargers. Thus, without the successful unlocking of these bottlenecks, the infrastructure and grid readiness pathways will continue to be the hurdles slowing down the large-scale adoption of commercial electric vehicles and, therefore, hindering the transition into fully electric logistics and public transport systems.

Electric Commercial Vehicle Market Opportunities:

The electric commercial vehicle market is opening up to countless possibilities through combining the advanced applications of digital technologies with renewable energy solutions. Fleet Operators can benefit from the use of advanced telematics, AI-powered route optimization, and predictive maintenance systems - all to maximize efficiency in operations and extend the lifetime of vehicles. They are assistive tools that help in intelligent fleet management by minimizing downtimes and improving safety and energy consumption monitoring for valuable operational efficiencies, as it relates to cost savings. Another major opportunity channel is attaching electric fleets with renewable energy sources, such as solar and wind, installed on-site to ensure self-sufficient and low-carbon charging ecosystems. With increasing commitments to net zero, the big companies in the world have adopted much more demanding targets for end-to-end sustainable green transport solutions. Presently, fleets can use vehicle-to-grid (V2G) technology, allowing their electric trucks and vans to push surplus energy back into the grid during peak demand periods, thus creating additional income avenues for fleet owners. The early investors in electric fleets will enjoy the benefits of competitive advantage, brand equity, and better affiliations with consumers who possess an environmentally-focused sensibility. Overall, the fruits of these technological and sustainability innovations leave fertile soil for companies to create their futures and achieve sustainable long-term growth in commercial transport.

Electric Commercial Vehicle Market Segmentation:

Market Segmentation: By Vehicle Type

• Electric Trucks

• Electric Vans

• Electric Buses

The international electric commercial vehicle market is broadly divided into electric trucks, electric vans, and electric buses. Each vehicle has distinct parameters for operational requirements and customer demand. For electric trucks, the development has mainly been directed towards long-haul freight and heavy-duty applications, gaining popularity mainly with the advent of larger battery capacity and charging infrastructure. Tesla, Volvo, and Daimler have been frontrunners in this segment for high-range, high-load electric truck models that promise lower operating costs and emissions. Electric vans are mainly used in last-mile delivery and urban logistics, since their compact design allows for quick maneuvers with lower emissions in highly congested city centers. Government intervention to replace diesel fleets for urban air pollution and noise abatement greatly fosters electric bus adoption. In addition, electric minibuses and shuttles are being rolled out for airport transfers and corporate commuting, further opening market opportunities. Fleet operators now give more prioritization to TCO (total cost of ownership) benefits along with regulatory compliance, thus accelerating the vehicle replacement cycle. All these types of vehicles together are closing the loop for diverse commercial transport requirements and enhancing the overall market.

Market Segmentation: By Propulsion Type

• Battery Electric Vehicles

• Plug-in Hybrid Electric Vehicles

• Fuel Cell Electric Vehicles

The market is segmented into: Battery Electric Vehicles (BEVs), Plug-In Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs) - the three technologies having slightly different operational advantages. Of these three variants operating on certain principles, battery electric vehicles (BEVs), which run purely on electricity stored in onboard batteries, are the most advanced and commercially developed, owing to advancements in technology and decreasing costs of batteries. BEVs produce zero tailpipe emissions and require lower maintenance. They are getting increasing support from the local urban community for the charging infrastructure. PHEVs are a hybrid of combustion engine and electric motors, giving operators needing longer range a freer way to reduce emissions on shorter trips. Thus, it is a kind of transitional arrangement in regions where much development of charging networks is still in the works. FCEVs are currently gaining attention for heavy-duty and long-range applications due to quick refueling and long-range capabilities, as they use hydrogen to generate electricity on board. Each propulsion type addresses specific operational challenges and regional readiness, enabling fleet managers to pick solutions that best match their route networks and sustainability objectives. Provided their future is assured with policy support and technology improvements, these propulsion technologies would co-exist and transform to cater to the varied commercial needs across the globe.

Market Segmentation: By End-Use Application

• Last-Mile Delivery

• Distribution & Logistics

• Public Transport

• Municipal Services

The electric commercial vehicle market is segmented based on end applications like last-mile delivery, distribution & logistics, public transportation, and municipal services. The last-mile delivery, in itself, has been exponentially growing in view of rising e-commerce demand and tightening urban environmental regulations. Electric vans and small trucks are preferred for their gentle glide through busy streets and don't pollute before delivery because of tailpipe emissions; thereby facilitating faster and greener deliveries. Distribution & logistics applications are concerned with medium and long-haul routes between regional warehousing and retail hubs, where range and payload capacity become key factors; so, electric trucks are increasingly being designed with larger battery packs and advanced charging solutions to address these concerns. Public transport is another big segment within which electric buses are revolutionizing urban commuting by abatement of air and noise pollution, thereby contributing to net-zero emission targets. Municipal authorities worldwide are doling out subsidies and mandates for converting aging diesel fleets into electric ones. Municipal services have garbage collection trucks, street sweepers & maintenance vehicles that all benefit from predictable routes and centralized depot charging, thereby supporting city sustainability agendas and offsetting operational costs for local governments.

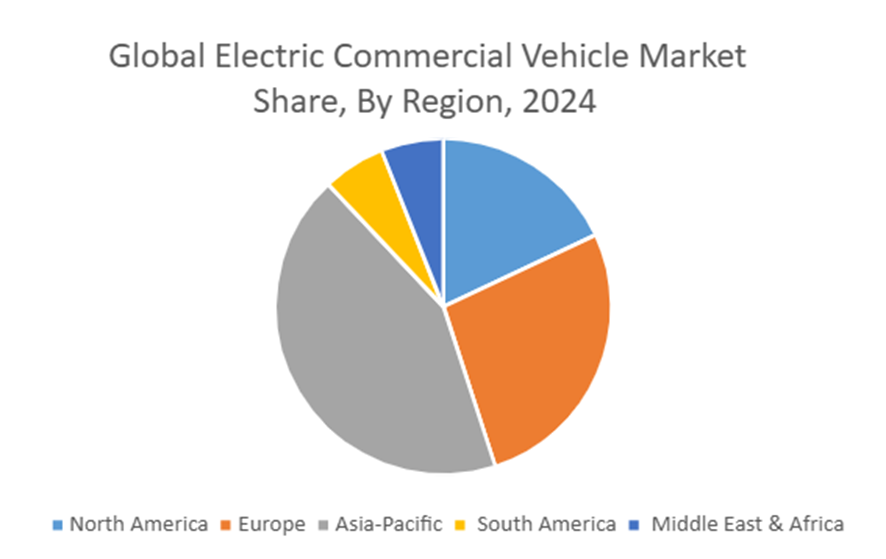

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

With strong government mandates and rapid urbanization, the Asia-Pacific region is at the forefront of the global electric commercial vehicle market, with major manufacturing facilities like China dictating both production and domestic adoption. Europe closely follows due to stringent emission standards set by the EU Green Deal, coupled with generous incentives, to hasten fleet operators' shift to electric solutions. In North America, state-level support, corporate sustainability commitments, and investments in charging infrastructure are making steady contributions to market growth, especially for larger logistics and delivery fleets. Adoption is emerging in South America due to pilot programs and increasing focus on urban sustainability initiatives to curb air pollution. The Middle East and Africa are still in the nascent stage of market development, primarily driven by green city projects, government-led clean transport pilot projects, and rising awareness around environmental benefits. Even with such regional dynamics at play, the world is seemingly making a shift toward cleaner commercial transport, albeit at different paces and with varied focus areas across different regions.

COVID-19 Impact Analysis on the Electric Commercial Vehicle Market:

Right from the start, the COVID-19 pandemic presented enormous challenges for the electric commercial vehicle market, interrupting supply chains across the world, stopping production lines, and postponing the launch of new vehicles. Lockdowns and restrictions led to a temporary decrease in fleet demand since logistics and public transport operations were cut back or halted altogether. However, the crisis also accelerated long-term shifts toward e-commerce and last-mile delivery, creating strong new demand for electric vans and light-duty trucks. Furthermore, governments across the globe formulated green recovery packages and stimulus measures, enshrining investments in clean mobility solutions, providing subsidies and grants for fleet electrification. Supply chains for batteries experienced some delays, but were also the causation behind localized manufacturing investments encompassing resiliency. To summarize, COVID-19 became both a disruptive force and an unplanned catalyst, thus fast-tracking the adoption curve for electric commercial vehicles in the post-pandemic period.

Latest Trends/ Developments:

The marketplace for electric commercial vehicles has seen profound innovations, partnered with collaboration between major automakers on the development of cutting-edge technology. Companies are forming strategic alliances like GM and Hyundai's joint forces on electric van and pickup development to cut costs and ramp up quicker production. Battery technology keeps developing at breakneck speed, while new models such as Volvo's FH Electric are offering applications with ranges of more than 373 miles per charge, thereby resolving age-old range limitations for heavy-duty trucks. In parallel, fleet operators are adopting AI-powered energy and fleet management systems that optimize routes, improve charging schedules, and enable on-demand predictive maintenance with reduced downtime, thereby saving costs and increasing efficiency. The integration of renewable energy sources and vehicle-to-grid (V2G) capabilities is also on the rise, enabling fleets to support grid stability and earn new forms of revenue from these services. All these trends indicate that the time is changing from pilot deployment to commercial application scale, thus putting electric commercial vehicles as imminent pillars in the next generation of global supply chain and urban transport systems.

Key Players:

• BYD

• Mercedes-Benz Group AG

• Yutong

• AB Volvo

• Ford Motor Company

• Rivian Automotive, Inc.

• Proterra Inc.

• Nikola Corporation

• Scania AB

• MAN Truck & BUS SE

Chapter 1. Global Electric Commercial Vehicle Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Electric Commercial Vehicle Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Electric Commercial Vehicle Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Electric Commercial Vehicle Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Electric Commercial Vehicle Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Electric Commercial Vehicle Market – By Vehicle Type

6.1. Introduction/Key Findings

6.2. Electric Trucks

6.3. Electric Vans

6.4. Electric Buses

6.5. Y-O-Y Growth trend Analysis By Vehicle Type

6.6. Absolute $ Opportunity Analysis By Vehicle Type, 2025-2030

Chapter 7. Global Electric Commercial Vehicle Market – By Propulsion Type

7.1. Introduction/Key Findings

7.2. Battery Electric Vehicles

7.3. Plug-in Hybrid Electric Vehicles

7.4. Fuel Cell Electric Vehicles

7.5. Y-O-Y Growth trend Analysis By Propulsion Type

7.6. Absolute $ Opportunity Analysis By Propulsion Type, 2025-2030

Chapter 8. Global Electric Commercial Vehicle Market – By End-Use Application

8.1. Introduction/Key Findings

8.2. Last-Mile Delivery

8.3. Distribution & Logistics

8.4. Public Transport

8.5. Municipal Services

8.6. Y-O-Y Growth trend Analysis By End-Use Application

8.7. Absolute $ Opportunity Analysis By End-Use Application, 2025-2030

Chapter 9. Global Electric Commercial Vehicle Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Vehicle Type

9.1.3. By Propulsion Type

9.1.4. By End-Use Application

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Vehicle Type

9.2.3. By Propulsion Type

9.2.4. By End-Use Application

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Vehicle Type

9.3.3. By Propulsion Type

9.3.4. By End-Use Application

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Vehicle Type

9.4.3. By Propulsion Type

9.4.4. By End-Use Application

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Vehicle Type

9.5.3. By Propulsion Type

9.5.4. By End-Use Application

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Electric Commercial Vehicle Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. BYD

10.2. Mercedes-Benz Group AG

10.3. Yutong

10.4. AB Volvo

10.5. Ford Motor Company

10.6. Rivian Automotive, Inc.

10.7. Proterra Inc.

10.8. Nikola Corporation

10.9. Scania AB

10.10. MAN Truck & BUS SE

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Electric Commercial Vehicle Market was valued at USD 59.23 billion in 2024 and is projected to reach a market size of USD 166.28 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.93%.

Stricter global emission regulations and government incentives are pushing fleets to adopt electric vehicles rapidly. Lower operating and maintenance costs make electric commercial vehicles economically attractive for businesses.

The Electric Commercial Vehicle market by end-use application is segmented into last-mile delivery, distribution & logistics, public transport, and municipal services. Each segment addresses different operational needs, from urban deliveries to city transit and specialized municipal tasks.

Asia-Pacific is the most dominant region for the Electric Commercial Vehicle Market.

BYD (China), Mercedes-Benz Group AG (Germany), Yutong (China), AB Volvo (Sweden), and Ford Motor Company (US) are the key players in the Electric Commercial Vehicle Market.