Electric Bus Charging Infrastructure Market Research Report – Segmentation by Type (DC Fast Chargers, AC Chargers, Wireless Charging, Battery Swapping Stations); By Distribution Channel (Direct Sales, EPC Contractors, Charging Network Operators, Government Tenders, OEM Partnerships); By Deployment Model (On-depot Charging, On-route Charging, Public Charging Hubs); By Component (Charging Stations, Software & Services, Transformers & Switchgear, Cables & Connectors); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16564

Format:

Region: Global

Market Size and Overview:

The Electric Bus Charging Infrastructure Market was valued at USD 3.9 Billion in 2024 and is projected to reach a market size of USD 10.54 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.0%.

The Electric Bus Charging Infrastructure Market is experiencing a profound transformation, standing at the vanguard of sustainable urban mobility. This burgeoning sector is fundamentally reshaping how public transportation systems worldwide transition towards electrification, driven by an escalating global commitment to reducing carbon emissions and improving air quality in metropolitan areas. The market encompasses a comprehensive ecosystem of hardware, software, and services essential for powering electric bus fleets, ranging from sophisticated high-power charging stations and intelligent energy management systems to intricate grid integration solutions. As cities increasingly adopt electric buses to meet ambitious environmental targets and enhance public health, the demand for robust, scalable, and efficient charging infrastructure has surged, becoming a critical enabler for widespread electric bus deployment. The market's trajectory is intrinsically linked to global electrification efforts, policy support, and the continuous drive for technological innovation, making it a dynamic and strategically vital sector.

Key Market Insights:

The total investment in public and private electric bus charging infrastructure projects exceeded $4.5 billion in 2024, highlighting strong financial commitment.

Approximately 65% of new charging installations in 2024 were DC fast chargers, emphasizing the preference for rapid energy replenishment. Smart charging solutions, leveraging artificial intelligence for load management, saw an adoption rate of nearly 40% among new depot installations.

The average utilization rate of existing electric bus charging infrastructure reached 55% in 2024, indicating increasing fleet sizes and operational hours.

Over 80% of newly procured electric buses in 2024 were accompanied by planned charging infrastructure upgrades or new installations.

The market for charging management software alone surpassed $300 million in 2024, underscoring the importance of digital solutions. Public-private partnerships accounted for approximately 35% of total infrastructure investment in 2024, fostering collaborative development.

Market Drivers:

Government Initiatives and Emission Regulations

The escalating global imperative to combat climate change and mitigate urban air pollution is a primary catalyst for the electric bus charging infrastructure market. Governments worldwide are implementing stringent emission standards and offering substantial incentives, subsidies, and grants for the adoption of electric vehicles, particularly in public transport. These policy frameworks not only encourage the procurement of electric buses but also mandate the development of robust charging ecosystems, creating a predictable and supportive regulatory environment that drives investment and deployment in charging infrastructure.

Advancements in Battery and Charging Technology

Continuous innovation in battery energy density, charging efficiency, and power electronics is significantly propelling the market forward. Breakthroughs in battery technology are extending the range of electric buses, making them more viable for diverse routes, while simultaneous advancements in high-power charging solutions are drastically reducing charging times. This technological synergy addresses key operational concerns for bus operators, making the transition to electric fleets more practical and economically attractive, thereby increasing the demand for sophisticated charging infrastructure.

Market Restraints and Challenges:

The electric bus charging infrastructure market faces significant hurdles, primarily concerning the substantial initial capital investment required for high-power charging stations and grid upgrades. Integration complexities with existing power grids and managing peak load demand pose technical challenges. Furthermore, the lack of standardized charging protocols across different manufacturers can hinder interoperability, while limited space availability in urban depots for extensive charging infrastructure also presents a constraint.

Market Opportunities:

The burgeoning demand for smart charging solutions, integrating AI and IoT for optimized energy management, presents a substantial opportunity. The expansion into developing economies, where public transport electrification is gaining momentum, offers untapped growth potential. Additionally, the integration of renewable energy sources with charging infrastructure and the development of vehicle-to-grid (V2G) capabilities represent significant avenues for innovation and market expansion, creating new revenue streams and sustainable solutions.

Market Segmentation:

Segmentation by Type:

• DC Fast Chargers

• AC Chargers

• Wireless Charging

• Battery Swapping Stations

Wireless charging is emerging as the fastest-growing segment, driven by its inherent convenience, reduced physical footprint, and potential for seamless on-route charging without manual intervention. This technology eliminates the need for cables and connectors, offering operational efficiency and aesthetic advantages, particularly for urban environments where continuous operation and minimal disruption are paramount for public transport.

DC Fast Chargers currently dominate the market, holding the largest share due to their ability to rapidly replenish electric bus batteries, significantly reducing downtime and enabling more efficient fleet operations. Their high power output makes them ideal for both depot and on-route charging scenarios, providing the necessary speed and reliability for heavy-duty public transportation vehicles.

Segmentation by Distribution Channel:

• Direct Sales

• EPC Contractors

• Charging Network Operators

• Government Tenders

• OEM Partnerships

Charging Network Operators are rapidly expanding as a distribution channel, providing comprehensive, integrated solutions including installation, operation, and maintenance of charging infrastructure. Their ability to offer subscription-based services and manage large-scale networks appeals to public transport authorities seeking outsourced expertise and reliable, end-to-end charging solutions without significant upfront operational burdens.

Government Tenders remain the most dominant distribution channel, given that public transport electrification initiatives are largely driven by municipal and national policies. These tenders often involve large-scale projects, requiring comprehensive proposals and adherence to strict regulatory guidelines, making them the primary procurement method for major electric bus charging infrastructure deployments.

Segmentation by Deployment Model:

• On-depot Charging

• On-route Charging

• Public Charging Hubs

Public Charging Hubs are experiencing the fastest growth, driven by the need for flexible charging options beyond traditional depots, especially for longer routes or mixed-fleet operations. These hubs, often strategically located along bus corridors or at transport interchanges, provide accessible, high-power charging facilities that support operational flexibility and help alleviate range anxiety for bus operators.

On-depot Charging continues to be the most dominant deployment model, forming the backbone of electric bus operations due to its cost-effectiveness and operational simplicity. Buses can be charged overnight or during off-peak hours when electricity rates are lower, making it the most practical and widely adopted solution for managing large electric bus fleets efficiently and reliably.

Segmentation by Component:

• Charging Stations

• Software & Services

• Transformers & Switchgear

• Cables & Connectors

The Software & Services segment is the fastest-growing component, driven by the increasing complexity of managing large-scale charging networks and optimizing energy consumption. This includes intelligent charging management systems, predictive maintenance software, and data analytics platforms that enhance operational efficiency, reduce costs, and ensure the reliability of the entire charging ecosystem.

Charging Stations represent the most dominant component in the market, as they are the core physical infrastructure required for electric bus charging. This segment includes the power electronics, dispensers, and associated hardware that directly deliver electricity to the buses, forming the fundamental and most significant investment for any electric bus charging project.

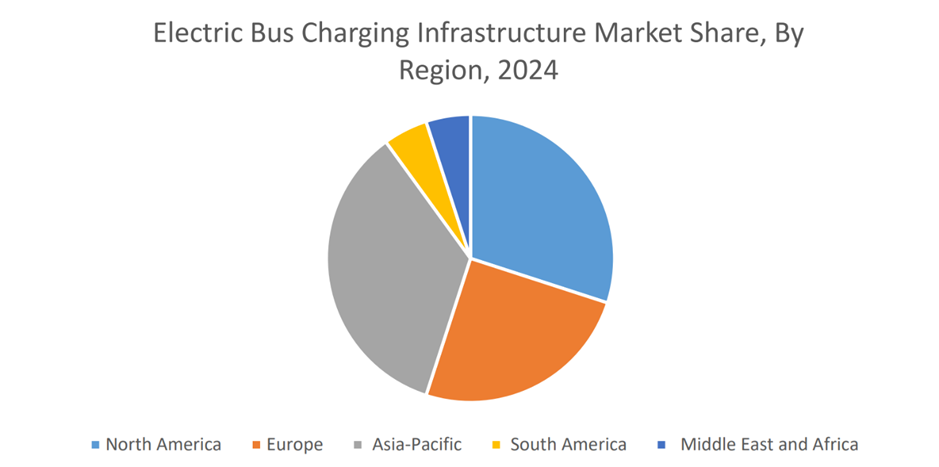

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

Most Dominant Region: Asia-Pacific maintains its dominance, primarily due to the sheer volume of electric bus deployments and associated infrastructure development, particularly in countries with large urban populations and proactive electrification policies.

Fastest-Growing Region: Asia-Pacific is also the fastest-growing region, experiencing exponential expansion fueled by massive government investments, rapid urbanization, and a burgeoning demand for sustainable public transport solutions across its diverse and populous economies.

COVID-19 Impact Analysis:

The COVID-19 pandemic initially caused disruptions in supply chains and project timelines for electric bus charging infrastructure. However, it also underscored the importance of resilient, localized supply chains and accelerated the global focus on green recovery initiatives. Governments prioritized investments in sustainable infrastructure, including electric public transport, to stimulate economic growth and meet climate targets. This led to a renewed impetus for electric bus adoption and, consequently, increased demand for charging infrastructure as part of broader environmental and economic recovery strategies.

Latest Trends and Developments:

The market is witnessing a strong trend towards higher power charging solutions, including megawatt charging systems, to support larger battery capacities and faster turnaround times. The integration of Vehicle-to-Grid (V2G) technology is gaining traction, allowing electric buses to return energy to the grid during off-peak hours, enhancing grid stability and creating new revenue streams. Furthermore, there's a growing emphasis on modular and scalable charging solutions that can be easily expanded as fleet sizes grow, alongside the increasing adoption of AI-driven smart charging platforms for optimized energy management and operational efficiency.

Key Players in the Market:

• ABB Ltd.

• Alstom SA

• BYD Auto Co. Ltd

• ChargePoint Inc.

• Efacec

• Furrer + Frey AG

• Heliox

• Liikennevirta Oy(Virta Global)

• Nuvve Corporation

• Proterra

Chapter 1. Global Electric Bus Charging Infrastructure Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Electric Bus Charging Infrastructure Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Electric Bus Charging Infrastructure Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Electric Bus Charging Infrastructure Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Electric Bus Charging Infrastructure Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Electric Bus Charging Infrastructure Market – By Type

6.1. Introduction/Key Findings

6.2. DC Fast Chargers

6.3. AC Chargers

6.4. Wireless Charging

6.5. Battery Swapping Stations

6.6. Y-O-Y Growth trend Analysis By Type

6.7. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global Electric Bus Charging Infrastructure Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Direct Sales

7.3. EPC Contractors

7.4. Charging Network Operators

7.5. Government Tenders

7.6. OEM Partnerships

7.7. Y-O-Y Growth trend Analysis By Distribution Channel

7.8. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global Electric Bus Charging Infrastructure Market – By Deployment Model

8.1. Introduction/Key Findings

8.2. On-depot Charging

8.3. On-route Charging

8.4. Public Charging Hubs

8.5. Y-O-Y Growth trend Analysis By Deployment Model

8.6. Absolute $ Opportunity Analysis By Deployment Model, 2024-2030

Chapter 9. Global Electric Bus Charging Infrastructure Market – By Component

9.1. Introduction/Key Findings

9.2. Charging Stations

9.3. Software & Services

9.4. Transformers & Switchgear

9.5. Cables & Connectors

9.6. Y-O-Y Growth trend Analysis By Component

9.7. Absolute $ Opportunity Analysis By Component, 2024-2030

Chapter 10. Global Electric Bus Charging Infrastructure Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By Deployment Model

10.1.5. By Component

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By Deployment Model

10.2.5. By Component

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By Deployment Model

10.3.5. By Component

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Application

10.4.4. By Deployment Model

10.4.5. By Component

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Distribution Channel

10.5.4. By Deployment Model

10.5.5. By Component

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Electric Bus Charging Infrastructure Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. ABB Ltd.

11.2. Alstom SA

11.3. BYD Auto Co. Ltd

11.4. ChargePoint Inc.

11.5. Efacec

11.6. Furrer + Frey AG

11.7. Heliox

11.8. Liikennevirta Oy (Virta Global)

11.9. Nuvve Corporation

11.10. Proterra

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The market's growth is primarily driven by stringent government emission regulations, increasing global commitments to sustainable urban mobility, and significant technological advancements in both battery and charging technologies that enhance the operational viability of electric buses.

Key concerns include the substantial initial capital investment required for infrastructure, complex grid integration challenges, the lack of widespread standardization in charging protocols, and the limited physical space available in urban bus depots for large-scale charging installations.

Prominent players include ABB Ltd., Siemens AG, ChargePoint Holdings, Inc., EVBox Group, Webasto Group, Heliox B.V., Alstom SA, Proterra Inc., BYD Company Ltd., Hitachi Energy Ltd., Kempower Oyj, Delta Electronics, Inc., Ekoenergetyka-Polska S.A., Shinry Technologies Co., Ltd., and XCharge Energy.

Asia-Pacific currently holds the largest market share, estimated at approximately 35%, driven by extensive electric bus adoption and infrastructure development in its populous nations.

Asia-Pacific is also expanding at the highest rate, fueled by substantial government investments, rapid urbanization, and a strong push towards sustainable public transportation across the region.