Global Distributed Energy Resource Management Systems (DERMS) Market Research Report – Segmentation By End User (Utilities, Commercial & Industrial, Residential); By Application (Grid Balancing, Voltage & Frequency Regulation, Energy Storage Management, Others); By Components (Software, Services); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16557

Format:

Region: Global

Market Size and Overview:

The Distributed Energy Resource Management Systems (DERMS) Market was valued at USD 0.67 billion in 2024 and is projected to reach a market size of USD 1.54 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 18.11%.

Foremost among these changes is the Global Distributed Energy Resource Management Systems (DERMS) market, which is transforming the modern energy landscape in favor of smart, flexible, and resilient power grids. As more distributed renewable energy resources, such as solar, wind, and battery storage, are integrated, the DERMS will need to monitor, optimize, and control these decentralized energy assets in real-time. The utilities and grid operators are looking up to DERMS to ensure the stabilization of the grid, provide operational cost savings, and satisfy increasing sustainability demands. The greater the emphasis on energy decentralization, electrification, and digitalization, the greater DERMS will become as an enabler of future smart grids that ensure the efficient distribution of energy to the benefit of customers and utilities.

Key Market Insights:

DERMS can reduce power outage durations by up to 50%, helping utilities maintain service continuity during extreme weather events and grid disruptions. This capability is crucial as climate-related outages become more frequent.

Advanced DERMS improve renewable energy integration efficiency by around 40%, making it easier for grids to handle higher shares of solar and wind power. This supports global decarbonization and net-zero targets.

Distributed Energy Resource Management Systems (DERMS) Market Drivers:

A major driver fueling the DERMS market is the global surge in renewable energy adoption and the transition toward decentralized energy systems.

The world is witnessing a huge upsurge in renewable energy installation and the transition toward decentralized energy systems, which form the major driving force for the DERMS market. As solar and wind power installations are rapidly growing worldwide, the grid operators face difficulties balancing intermittent and variable gaps of generation sources with reliability and stability. With advanced real-time visibility and control over distributed energy resources (DERs), DERMS allows power-system controllers to integrate high renewables penetration seamlessly. By forecasting and coordinating the output of solar rooftops, wind farms, and battery storage systems, DERMS increases grid flexibility while preventing overloads and blackouts. Also, while various nations are pushing for ambitious net-zero targets and carbon-neutrality commitments, maximizing the penetration of renewables becomes increasingly important. DERMS will enable utilities to move toward a more dynamic, distributed, and cleaner energy generation system instead of a centralized fossil-fuel-based generation. This allows consumers to develop into "prosumers" actively trading on energy markets by generating and selling surplus power. Hence, with the ever-increasing share of renewables and in support of decentralization of generation, DERMS will be the backbone of the future sustainable smart grid.

Another key driver for the DERMS market is the growing global focus on improving grid resilience and reliability in the face of rising energy demand and extreme weather events.

The global emphasis on improving grid resilience and reliability is also another supporting factor for DERMS. In this era of increasing energy demand and extreme weather events, the grids are not designed to handle the unpredictable generation coming from distributed sources with bi-directional flow from centralized plants. DERMS thus involve advanced monitoring, quick detection of faults, and automated response strategies, enabling enhanced dimension stability and downtime minimization to improve overall grid performance. DERMS can efficiently balance loads, fine-tune voltages and frequencies, and proactively mitigate the consequences of outage or overload. The unprecedented increase in the frequency of heat waves, storms, and wildfires due to climate change has changed from a phenomenon that only science and hazard scientists now presents models and warnings about. The continuity of power supply has turned into one of the most critical objectives, one that governments and energy providers scramble to get back on track at best. It is here that DERMS provides advantages through dynamic islanding along with microgrids that allow grid sections to function autonomously in the face of emergencies, leading to better disaster recovery capabilities.

Distributed Energy Resource Management Systems (DERMS) Market Restraints and Challenges:

One of the major challenges restraining the widespread adoption of DERMS is the complexity involved in its implementation and the lack of interoperability among diverse energy assets and systems.

Another of the constant obstacles facing full adoption of DERMS lies in the complexity of implementation and lack of interoperability within the various energy assets and systems. DERMS had to integrate a myriad of distributed energy resources: rooftop solar, battery storage, and electric vehicles, as well as smart appliances, with all the different communication protocols, different data formats, and control systems. All of these complicate seamless interfacing, especially with an aging grid infrastructure that was never designed to allow bi-directional flows or real-time data processing. The customization has involved different utility environments, which is another factor prolonging and costly for a small or medium-sized utility in the large-scale adoption of DERMS. Another limitation in smooth installation is less technical manpower who understand DERMS architecture, cybersecurity, and analytics. Deregulated as well as acquired industry national standardization and open-source solutions will clear the air on the interoperability hindrance for making DERMS operationally efficient. Solving this issue will activate the full potential of DERMS, delivering economically and scalable solutions in the long run.

Distributed Energy Resource Management Systems (DERMS) Market Opportunities:

The transition of global energy systems such that they are decentralized, digitalized, and decarbonized creates enormous opportunities for the DERMS market. Utilities and grid operators will be able to take advantage of these DERMS features to generate new revenue sources through sophisticated demand response programs, virtual power plants, and dynamic pricing models. Whereas large numbers of electric vehicles become more popular and energy storage prices continually drop, DERMS would integrate large fleets of EVs and distributed batteries as grid-supporting assets by offering frequency regulation, peak shaving, and backup services. Notably, DERMS also enables utilities to allow consumers to become active and engaged market participants ("prosumers") in generating, storing, and trading energy related to their localities, which in turn encourages customer engagement and loyalty. Developing regions and rural areas also have excellent prospects for DERMS microgrid applications, which would scale up energy access and resilience improvements in remote communities. Government incentives and global policy pushes for smarter, more resilient grids further boost the market's growth potential.

Distributed Energy Resource Management Systems (DERMS) Market Segmentation:

Market Segmentation: By End User

• Utilities

• Commercial & Industrial

• Residential

DERM markets are segmented by their end users, which are utilities, commercial & industrial (C&I), and residential sectors, each with very different needs and growth drivers. Utilities, being the largest segment, find themselves in a classic dilemma while dealing with the rapid growth of distributed energy resources, such as rooftop solar, wind farms, battery storage, and electric vehicles. The DERMS platform gives utilities real-time visibility and control to improve grid stability while providing enhanced outage management features via automation and predictive analytics. In addition, DERMS is providing a completely new platform for fast growth in commercial & industrial segments, wherein large energy users seek to lower their operating costs and carbon footprints by integrating onsite generation and energy storage. Also, companies are starting to opt for demand response programs and local energy markets with aid from DERMS, in optimizing these resources while guaranteeing reliability. Although it is the smallest today, the residential segment is expected to grow with lightning speed as prosumer trends gain traction and consumers start adopting rooftop solar, home batteries, and EV chargers. In addition to these residential incentives, there is increasing interest in homeowners joining local energy trading and self-consumption strategies due to rising prices of energy prices.

Market Segmentation: By Application

• Grid Balancing

• Voltage & Frequency Regulation

• Energy Storage Management

• Others

Through applications, DERMS solutions are classified into grid balancing, voltage & frequency regulation, energy storage management, and others. The major application, grid balancing, is when operators need to manage increasing variability from renewable energy sources and changing demand profiles. DERMS allows dynamic load management, real-time coordination of assets, and optimization of distributed energy generation to reduce the risk of blackouts and curtailment of energy. Voltage & frequency regulation holds another important application in that it allows operators to address power quality and system stability in complex grid operations with bidirectional energy flows. Energy storage management has exponentially gained importance through utilities and large consumers, enabling them to derive maximum value from the battery systems being implemented for peak shaving, backup power alternatives, and ancillary services. The remaining category contains such emerging applications as EV charging coordination, microgrid islanding, and local energy trading platforms. The pace at which transport and buildings are being electrified means that the importance of full-spectrum DERMS applications is set to rise exponentially. These varied application areas are a testimony to DERMS's flexibility and scalability in the outreach for the future-proof, decentralized, and decarbonized power systems.

Market Segmentation: By Component

• Software

• Services

The genesis of the semiconductor market can be classified into two factions, namely software and services, both of which are vital for the successful deployment and operation phase of DERMS. Software dominates the market as there is a rise in demand for modern platforms that provide real-time monitoring and automated control, advanced analytics, and diverse-integrated capabilities to various energy assets. Smart software systems enable an operator to perform load forecasting, standalone generation/storage optimization, and rapid response to variable grid conditions. It also facilitates predictive maintenance and enables dynamic pricing models, further enhancing value to utilities and end users. The services segment includes system design, integration, consulting, training, and maintenance, all of which are the backbone of an effective implementation and long-term performance of DERMS. With the escalating complexity and customization of DERMS solutions to cater to specific regional and operational needs, the role of service providers in assisting utilities and C&I customers in navigating technical, regulatory, and operational challenges becomes crucial.

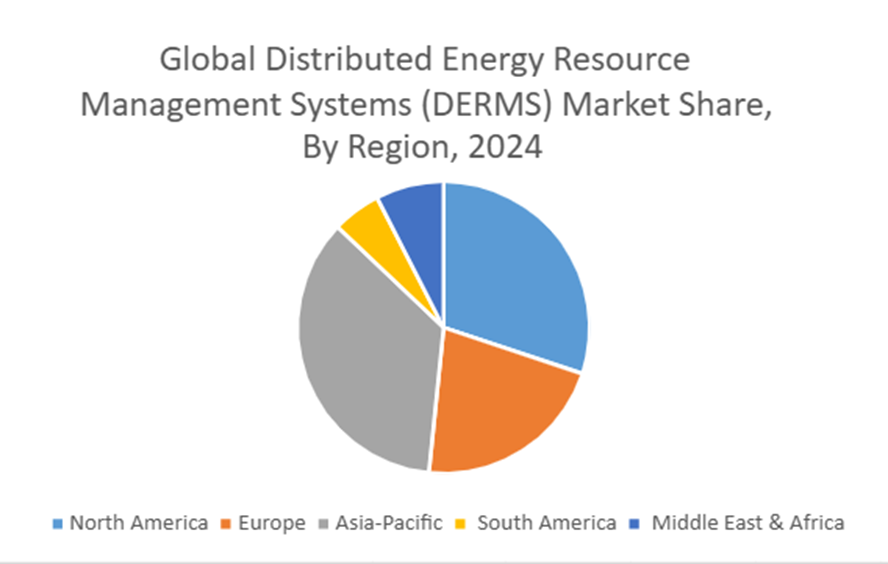

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

The Distributed Energy Resource Management Systems (DERMS) market is thriving in multiple regions, with Asia-Pacific taking the front seat due to key initiatives in China, India, and Japan for grid modernizations and integration of large quantities of renewable energy. North America closely follows, with the U.S. standing out for aggressive grid modernization efforts, electric vehicle infrastructure expansion, and supportive policies favoring decentralized energy systems. Europe also plays a significant role with a strong emphasis on decarbonization, energy resilience, and large-scale integration of distributed renewable resources. In the Middle East & Africa, countries such as those in the Gulf region are investing in smart grids and solar-based DERMS solutions for diversification of energy sources and reliability enhancement. Meanwhile, South America is steadily rising, with Brazil and Chile at the forefront, working to integrate solar and wind resources while advancing local DERMS capabilities to improve grid stability and support their renewable energy goals.

COVID-19 Impact Analysis on the Distributed Energy Resource Management Systems (DERMS) Market:

While COVID-19 positively influenced the long-term potential of the DERMS market, it temporarily interrupted the market in the short run. The global delay affecting DERMS deployment lasted only for the initial months of the pandemic in 2020, when supply chains were disrupted, and the workforce was limited in its scope of work due to lockdowns and other challenges. Many utilities focused instead on essential maintenance and emergency measures to keep things working, delaying investment in new technologies. However, the crisis also gave credence to the need for resilient, flexible, and intelligent energy systems and positioned DERMS as a strategic way of future-proofing grids. Utilities accelerated their digital transformation efforts, looking to limit onsite workforce dependency and improve real-time grid management, as remote operations and automation gained significance. The pandemic has intensified the push for decentralized energy solutions and local energy independence by encouraging investment in distributed energy resources that necessitate advanced management platforms. In summation, while COVID-19 slowed down physical project rollouts in the interim, it consolidated the strategic significance of DERMS and created an auspicious environment for strong market growth in the following years.

Latest Trends/ Developments:

The DERMS market is undergoing rapid change with the integration of AI, edge computing, and 5G for ultra-low latency control and predictive optimization over distributed assets. Utilities are now increasingly deploying DERM solutions for transactive energy systems and virtual power plants that facilitate peer-to-peer energy trading and dynamic grid services. Another trend is the expansion of DERMS in the Asia-Pacific region, backed by large renewable-scale-up and investments into smart infrastructure. Meanwhile, breakthroughs in edge computing appliances and cloud-native platforms are enabling real-time orchestration of thousands of DERs with high scalability and reliability. Furthermore, DERMS systems are becoming popular for 5G-enabled connectivity, which ensures secure, ultra-reliable, low-latency communication between grid controllers and distributed devices. Lastly, utilities are piloting blockchain-based platforms for peer-to-peer energy transactions and smart contracts, establishing the framework for decentralized energy markets. In summary, these developments shape DERMS into a cornerstone for resilient, intelligent, and decentralized energy systems around the globe.

Key Players:

Siemens (Germany)

• Emerson Electric Co. (US)

• Honeywell International Inc. (US)

• Schneider Electric (France)

• Itron Inc. (US)

• Oracle (US)

• General Electric Company (US)

• Enel Spa (Italy)

• AutoGrid Systems, Inc. (US)

• Mitsubishi Electric Power Products Inc. (US)

Chapter 1. Global Distributed Energy Resource Management Systems (DERMS) Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Distributed Energy Resource Management Systems (DERMS) Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Distributed Energy Resource Management Systems (DERMS) Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Distributed Energy Resource Management Systems (DERMS) Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Distributed Energy Resource Management Systems (DERMS) Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Distributed Energy Resource Management Systems (DERMS) Market – By End User

6.1. Introduction/Key Findings

6.2. Utilities

6.3. Commercial & Industrial

6.4. Residential

6.5. Y-O-Y Growth trend Analysis By End User

6.6. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 7. Global Distributed Energy Resource Management Systems (DERMS) Market – By Application

7.1. Introduction/Key Findings

7.2. Grid Balancing

7.3. Voltage & Frequency Regulation

7.4. Energy Storage Management

7.5. Others

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Distributed Energy Resource Management Systems (DERMS) Market – By Components

8.1. Introduction/Key Findings

8.2. Software

8.3. Services

8.4. Y-O-Y Growth trend Analysis By Components

8.5. Absolute $ Opportunity Analysis By Components, 2025-2030

Chapter 9. Global Distributed Energy Resource Management Systems (DERMS) Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By End User

9.1.3. By Application

9.1.4. By Components

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By End User

9.2.3. By Application

9.2.4. By Components

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By End User

9.3.3. By Application

9.3.4. By Components

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By End User

9.4.3. By Application

9.4.4. By Components

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By End User

9.5.3. By Application

9.5.4. By Components

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Distributed Energy Resource Management Systems (DERMS) Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Siemens

10.2. Emerson Electric Co.

10.3. Honeywell International Inc.

10.4. Schneider Electric

10.5. Itron Inc.

10.6. Oracle

10.7. General Electric Company

10.8. Enel Spa

10.9. AutoGrid Systems, Inc.

10.10. Mitsubishi Electric Power Products Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Distributed Energy Resource Management Systems (DERMS) Market was valued at USD 0.67 billion in 2024 and is projected to reach a market size of USD 1.54 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 18.11%.

Key drivers include the rapid growth of renewable energy and the urgent need for advanced grid stability solutions. Rising electrification trends and demand for resilient, flexible grids further boost DERMS adoption.

The DERMS market by application is segmented into grid balancing, voltage & frequency regulation, energy storage management, and others. These segments support efficient integration of renewables, improve power quality, and optimize distributed assets.

Asia-Pacific is the most dominant region for the Distributed Energy Resource Management Systems (DERMS) Market.

Siemens (Germany), Emerson Electric Co. (US), Honeywell International Inc. (US), Schneider Electric (France), Itron Inc. (US), Oracle (US), General Electric Company (US), Enel Spa (Italy), AutoGrid Systems, are the key players in the Distributed Energy Resource Management Systems (DERMS) Market.