Direct Methanol Fuel Cells Market – Segmentation by Application / End‑Use (Portable, Stationary, Transportation); By Component (Bipolar plates, Membranes (MEA), Catalysts and collectors); By Technology / Product Type (Passive DMFC, Active DMFC); By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16555

Format:

Region: Global

Market Size and Overview:

he Direct Methanol Fuel Cells Market was valued at $289.6 million in 2024 and is projected to reach a market size of $640.38 million by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.2%

Direct Methanol Fuel Cells (DMFCs) are changing fast because industries want small, good, and independent power to meet different energy needs. With better parts like plates, membranes, and catalysts, DMFCs can now turn methanol into electricity right where it's needed, even if there's no grid. This helps cut down on using old-fashioned power sources and makes things more trustworthy, especially if getting to a grid is hard or not steady. More gadgets, portable stuff, and faraway work are happening, so DMFCs are a must for giving steady, clean energy for things that need to happen now and last a long time. Things like electronics, travel, defense, and phone companies are using DMFCs for battery chargers, backup power, or to make electric cars and robots go farther. They're quiet, don't pollute much, and fill up fast, which makes them great for places that need to save time and space. New stuff like simple DMFC designs, small power systems, and mixes with green energy or batteries make them even better and easier to use. Also, DMFCs are coming together with new tech like IoT, AI energy controls, and light materials. This means smarter systems that use less power right where they're used. Because people want power that's easy to move and good for the planet in distant places, DMFCs are turning into a key part of important jobs that need trust, movement, and low pollution without needing gas or big batteries.

Key Market Insights:

Direct Methanol Fuel Cells (DMFCs) are getting more popular for portable and off-grid power. Right now, most of them (over 60%) are used in electronics and tiny backup systems. People want power sources that are small, light, and last a long time, mostly when batteries don't cut it, and it's a pain to recharge them. DMFCs are cool because you can fill them up fast, and they give you steady power. That's why they're great for being on the move or working in the field.

Passive DMFC systems are the big dogs, taking up about 80% of the market. They're liked because they're simple, cheap, and don't need much upkeep for smaller power needs. Since they don't need pumps or fancy controls, they're simple to stick in stuff like laptops, chargers, security gear, and military tools used way out in the sticks.

Bipolar plates make up more than 35% of all the money spent on DMFC parts. That means folks are trying hard to make sure power spreads right, heat is controlled, and everything holds together well. New stuff in materials and how things are made are helping DMFCs work better and cost less, which makes them a better deal for businesses.

More industries, such as phone companies, the military, and transportation, are using them. Over 70% of people in these fields are checking out DMFCs because they need power that’s quiet, clean, and keeps going even when there's no easy access to the power grid. As businesses look for something better than batteries and generators, DMFCs are becoming the go-to choice for power in tricky spots and pressing situations.

Direct Methanol Fuel Cells Market Key Drivers:

Why DMFCs Are Becoming More Popular in Portable Power Needs.

Because industries and people want power that works on the go or isn't tied to the grid, DMFCs are becoming a go-to option. They make power without needing to connect to anything. They're small, light, and give power consistently, which is great when you can't recharge batteries or there are no regular power sources around. You'll find them in military operations, disaster relief, out in the field, and even in wearable gadgets. They give quiet, clean, non-stop power wherever it's needed. The more we need power on the move, the faster this methanol fuel cell thing is catching on.

Clean Energy Focus Boosts DMFC Use.

Everyone's trying to be more sustainable and cut down on emissions. DMFCs are a good option because they don't pollute as much as generators that use fossil fuels or lithium-ion batteries. Methanol is easy to store and move, plus it doesn't make a lot of emissions when it's turned into energy, so it's good for the environment. Rules about reducing gases that harm the planet and companies wanting to be more energy-efficient are pushing them to check out other fuel cell options. DMFCs are turning out to be a clean and doable answer for portable and backup power needs.

More Gadgets Using DMFCs.

Since electronics are getting fancier and need more power, we need ways to keep them running longer without having to charge them all the time. DMFCs are being put in things like laptops, drones, security cameras, and ways to communicate. Because they can give power when you need it and work even when things get rough, they're great for when you need something that can perform well on its own. This need for strong, flexible power is why DMFCs are being used more in both business and personal tech.

Fuel Cell Improvements Mean Better Performance.

The technology in DMFCs keeps getting better, like the parts inside that help make power. This means they're more energy-efficient, last longer, and don't cost as much. New designs have made it easier to make DMFCs bigger and put them in all sorts of portable devices without needing complicated controls. These tech improvements are making DMFCs more available to different industries and improving how they work in the real world. Because of this, more companies and developers are seeing DMFCs as a good choice for small, sustainable power sources.

Direct Methanol Fuel Cells Market Restraints and Challenges:

High Costs, Fuel Handling Concerns, and Low Awareness Limit DMFC Adoption.

Even though Direct Methanol Fuel Cells could be great, some problems keep them from being used more. One big issue is that they cost a lot. The stuff inside, like catalysts and special parts, is pricey, and they're not made in huge numbers to bring the cost down. So, they're more expensive than batteries or generators that people already use. Also, DMFCs aren't as good at turning fuel into power as some other fuel cells. This means they might not work for things that need a lot of energy. Methanol, the fuel they use, is also tricky to handle because it's poisonous and can catch fire easily. This makes it harder to use them where everyone can get to them. If you're in a place where it's hard to get methanol, you might not be able to use DMFCs. And because not many people know about them or how they work, companies don't want to switch to them from what they already use. Until we fix the cost, safety, and knowledge problems, DMFCs will probably only become popular slowly.

Direct Methanol Fuel Cells Market Opportunities:

Expanding Off-Grid Demand and Innovation Fuel DMFC Growth.

The Direct Methanol Fuel Cells (DMFC) market has some good chances to grow since more industries want clean, portable energy that doesn't need to be connected to the grid. Since everyone is trying to cut down on carbon emissions and switch to green energy, DMFCs are a good choice to replace diesel generators and regular batteries. They're especially useful when you need something quiet, small, and dependable. New markets are starting to like DMFCs for things like cell towers, remote monitoring, and giving electricity to rural areas that don't have reliable grid access. There are also new ways to use DMFCs, like military gear, backup power, gadgets, and to help electric cars go farther. Scientists are making the technology better by improving how well the catalyst works, using simpler designs, and making methanol fuel easier to get. This boosts the system's performance and makes it cheaper, so DMFCs can be used more widely. As we need more ways to store energy and industries look for energy options that are flexible and green, DMFCs could become important for making power in different places.

Direct Methanol Fuel Cells Market Segmentation:

Market Segmentation: By Application / End‑Use:

• Portable

• Stationary

• Transportation

Right now, portable devices are the main use for Direct Methanol Fuel Cells (DMFCs) because they're good for small, light, off-grid power. You see them a lot in military radios, gadgets, backup power, and gear used in the field where regular batteries don't cut it, and there's no power grid. They give steady power for a while, which is great for devices that need to move around a lot and work on their own. Since people want power they can take anywhere, especially in defense and remote jobs, portable DMFCs are still number one in both rich and poor countries.

But, using DMFCs in transportation is catching up fast. Everyone wants cleaner energy for electric cars and extra power units. DMFCs are becoming popular to make light vehicles, drones, and forklifts go farther because they're small and easy to refuel, unlike hydrogen systems. You get more running time and less pollution without needing a lot of support systems. This is making them a hit for car and plane improvements that focus on being green and saving fuel.

Also, DMFCs are key for stationary stuff like backup and remote power. They're in cell towers, security, and monitoring gear in places far from civilization, where you need something reliable that doesn't need much fixing. These systems are quiet, don't pollute much, and pack a lot of power, so they're good for the countryside, mountains, or other isolated spots. It's not the biggest or fastest area, but stationary DMFCs still help the market grow and have potential for backup energy systems.

Market Segmentation: By Component:

• Bipolar plates

• Membranes (MEA)

• Catalysts and collectors

Bipolar plates are a key part of the DMFC market right now. They're super important for moving gases and electricity, plus they control heat and water. These plates keep the whole system working well and lasting long. People want better, lighter, and rust-proof plates as DMFC tech gets used in more things. Companies put money into materials like graphite and coated metals to help them work better and cost less.

Membrane Electrode Assemblies (MEAs) are the fastest-growing part of the DMFC world, especially the proton-conducting ones. MEAs make the cell reactions happen efficiently, so they're key to how well it works and how long it lasts. Better membrane stuff means better proton flow, less methanol crossover, and steadier heat control, which drives new ideas. Since industries need more power and reliability for gadgets, defense, and backup power, MEAs are getting lots of attention for research and sales.

Catalysts and current collectors are also needed in DMFCs. They help electrons flow and speed up reactions. They might not be the biggest or fastest growing, but they're key for overall system performance and lasting. New, cheaper catalysts and current collectors are bringing costs down and making these systems useful in more ways. They're vital for making cells better and using them in small, light devices.

Market Segmentation: By Technology / Product Type:

• Passive DMFC

• Active DMFC

Passive DMFCs lead the Direct Methanol Fuel Cells market because they're simple, small, and easy to use. Since they don't need pumps or compressors, they're great for things like military radios, sensors, and electronics. They're easy to install and maintain, making them a popular pick where light and reliable power are important. They're still a go-to for small, off-grid power when industries want quiet, self-powered options.

Active DMFCs are catching up fast because they're more efficient and can handle bigger jobs. They have pumps and fans to control methanol and air flow, boosting performance. This makes them good for backup power, transport, and industrial electronics that need more power. As they get cheaper and more reliable, they're being used more, especially where people want clean, scalable energy sources.

Market Segmentation: By Region:

• North America

• Europe

• Asia-Pacific

• Latin America

• Middle East and Africa

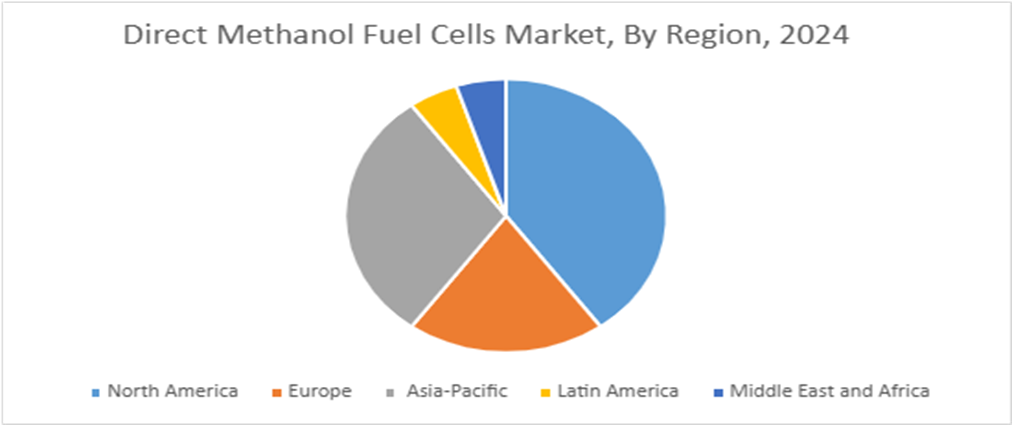

North America is still the biggest player in the Direct Methanol Fuel Cells (DMFC) market, grabbing about 40% of the world's share. This is mainly because the region is really into clean energy, DMFCs are commonly used in military and telecom stuff, and there's solid R&D support. Government help and private investments are also pushing DMFCs in areas that need off-grid and portable energy.

Asia-Pacific is the region that's growing the quickest, holding around 30% of the market. Quick industrial growth, higher energy needs, and more money being put into green tech—especially in countries such as China, Japan, and South Korea—are speeding up the use of DMFCs in things like consumer electronics, backup energy, and transportation.

COVID-19 Impact Analysis on the Direct Methanol Fuel Cells Market:

Because of the COVID-19 pandemic, more people got interested in Direct Methanol Fuel Cells (DMFCs). They saw them as a dependable, easy-to-carry, and clean way to get power, especially when there's no regular power or in emergencies. As healthcare, phone companies, and remote businesses needed more ways to make and store their power, DMFCs became popular since they are small and can use different kinds of fuel. The crisis showed that big power systems have weaknesses, which made industries and governments look for other power options. Now that the pandemic is over, the need for strong, low-pollution energy sources means DMFCs are still important for things like critical infrastructure, equipment used in the field, and portable devices. This strengthens their place in future energy plans.

Latest Trends/Developments:

Right now, the cool thing in the Direct Methanol Fuel Cells (DMFC) world is shrinking them down and fitting them into small gadgets. This is a game-changer for the military, phone companies, and anyone using electronics who needs reliable power when they're off the grid. Companies are working hard to make DMFCs smaller and lighter but pack more punch, so devices can run longer without being bulky. This change is all about meeting the need for light, portable power for things like field work, disaster relief, and wearable devices.

Also, more people are using methanol that comes from renewable sources like biomass, recycled CO₂, or green hydrogen. This fits with the push for being more eco-friendly and makes DMFCs more attractive as a clean way to get power. As countries try to cut down on carbon emissions, making green methanol is becoming a priority, and it works well with DMFC tech. Plus, better catalysts and longer-lasting membranes are making fuel cells more efficient and durable, which cuts costs and makes them a practical option for businesses. All these new things are helping DMFCs move from being a small, specialized item to being used more widely in cars, factories, and as backup power, making them a flexible way to handle local energy needs.

Key Players:

• SFC Energy AG (Germany)

• Ballard Power Systems, Inc. (Canada)

• Oorja Protonics (U.S.)

• TreadStone Technologies Inc. (US)

• Horizon Fuel Cell Technologies (Singapore)

• Hitachi Zosen Corporation (Japan)

• Antig Technology (Taiwan)

• MeOH Power (USA)

• Smart Fuel Cell GmbH (Germany)

• Ishikawajima-Harima Heavy Industries (IHI Corporation) (Japan)

Chapter 1. Direct Methanol Fuel Cells Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Direct Methanol Fuel Cells Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Direct Methanol Fuel Cells Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Direct Methanol Fuel Cells Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Direct Methanol Fuel Cells Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Direct Methanol Fuel Cells Market – By Application / End‑Use

6.1. Introduction/Key Findings

6.2. Portable

6.3. Stationary

6.4. Transportation

6.5. Y-O-Y Growth trend Analysis By Application / End‑Use

6.6. Absolute $ Opportunity Analysis By Application / End‑Use, 2025-2030

Chapter 7. Direct Methanol Fuel Cells Market – By Component

7.1. Introduction/Key Findings

7.2. Bipolar plates

7.3. Membranes (MEA)

7.4. Catalysts and collectors

7.5. Y-O-Y Growth trend Analysis By Component

7.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 8. Direct Methanol Fuel Cells Market – By Technology / Product Type

8.1. Introduction/Key Findings

8.2. Passive DMFC

8.3. Active DMFC

8.4. Y-O-Y Growth trend Analysis By Technology / Product Type

8.5. Absolute $ Opportunity Analysis By Technology / Product Type, 2025-2030

Chapter 9. Direct Methanol Fuel Cells Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Application / End‑Use

9.1.3. By Component

9.1.4. By Technology / Product Type

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Application / End‑Use

9.2.3. By Component

9.2.4. By Technology / Product Type

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Application / End‑Use

9.3.3. By Component

9.3.4. By Technology / Product Type

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Application / End‑Use

9.4.3. By Component

9.4.4. By Technology / Product Type

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Application / End‑Use

9.5.3. By Component

9.5.4. By Technology / Product Type

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Direct Methanol Fuel Cells Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. SFC Energy AG (Germany)

10.2. Ballard Power Systems, Inc. (Canada)

10.3. Oorja Protonics (U.S.)

10.4. TreadStone Technologies Inc. (US)

10.5. Horizon Fuel Cell Technologies (Singapore)

10.6. Hitachi Zosen Corporation (Japan)

10.7. Antig Technology (Taiwan)

10.8. MeOH Power (USA)

10.9. Smart Fuel Cell GmbH (Germany)

10.10. Ishikawajima-Harima Heavy Industries (IHI Corporation) (Japan)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Direct Methanol Fuel Cells Market was valued at $289.6 million in 2024 and is projected to reach a market size of $640.38 million by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.2%

The global DMFC market is driven by the rising need for lightweight, portable power sources and increasing adoption in off-grid, military, and electronic device applications.

Based on Technology, the Global DMFC Market is segmented into Passive DMFC and Active DMFC.

North America is the most dominant region for the Global Direct Methanol Fuel Cells Market.

SFC Energy AG (Germany), Oorja Fuel Cells (US), Ballard Power Systems (Canada), and TreadStone Technologies Inc. (US) are among the leading players in the Global DMFC Market.