Global Direct Drive (Gearless) Wind Turbine Market Research Report – Segmentation By Capacity (up to 3 MW, 3-5 MW, Above 5 MW); By Rotor Diameter (Up to 100 meters, 100-150 meters, Above 150 meters); By Application (Onshore, Offshore); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16554

Format:

Region: Global

Market Size and Overview:

The Direct Drive (Gearless) Wind Turbine Market was valued at USD 32.95 billion in 2024 and is projected to reach a market size of USD 63.61 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.06%.

A paradigm shift in renewable energy is being heralded by the Global Direct Drive (Gearless) Wind Turbine Market with innovative, efficient, and reliable technology. In contrast to the conventional wind turbine design, which is geared towards complex gearbox systems, the direct drive turbine design eliminates gearboxes. Therefore, it has fewer moving parts, lower maintenance requirements, and better operational lifetimes. This radically improves performance, particularly offshore and in harsh environments, where accessibility is challenging and reliability is paramount. The fast-growing global demand for clean energy, stringent carbon reduction targets, and an increase in investments toward sustainable infrastructure have made direct drive wind turbines the preferred option for many large-scale wind power projects.

Key Market Insights:

Gearless turbines can lower maintenance costs by up to 30–40%, helping operators save millions annually and improve project profitability, especially in remote or offshore locations.

Noise levels are reduced by nearly 90%, making direct drive turbines more suitable for onshore installations near populated areas and contributing to faster project approvals.

Direct Drive (Gearless) Wind Turbine Market Drivers:

A major driver for the growth of the direct drive (gearless) wind turbine market is the increasing demand for low-maintenance and highly reliable renewable energy systems.

The strong demand for minimal maintenance and high reliability from renewable energy systems is the greatest driving force behind the growth of the direct drive (gearless) wind turbine market. Most traditional wind turbines rely on complex gearbox assemblies, which are not only prone to mechanical failures but also entail high maintenance costs, especially in offshore environments where accessibility is difficult and downtime costs can be astronomical. Direct drive turbines eliminate the need for gearbox assemblies, thus significantly reducing the number of moving parts and minimizing the chances of mechanical breakdowns. Thus, it leads to reduced operational costs and higher incidental availability rates, increasing the attractiveness of projects over their lifetime. This gives a competitive edge to the resounding trend of attracting wind farm investors and operators as the world continues to move toward maximizing yield harvests while minimizing operational costs.

The rapid expansion of offshore wind energy is another key driver propelling the direct drive wind turbine market forward.

Soon to be a huge factor boosting the direct-drive wind turbine sector is offshore wind energy's fast-rising tendency worldwide. The offshore wind installations face harsh weather conditions, saltwater, and corrosion, not to mention restricted access by maintenance crews, therefore requiring reliability in any selected technology. Compared with the presence of gearboxes, direct drive turbines have simpler designs and, hence, avouch significantly superior durability and performance under demanding marine conditions. As governments worldwide make aggressive renewable energy targets aligned with climate commitments, offshore wind has become a focus of clean energy strategy, especially in Europe, China, and new Asian markets. In addition, the new larger diameter rotors and more powerful turbines-near half the size of 10 MW-are often preferred over gearless designs because they handle variable wind loads better than gear designs and largely reduce system configuration complexity. Their ability to provide stable, high-efficiency generation with very low service makes them very much compatible with the economic and environmental targets of large-scale offshore developments. This accelerated offshore speed not only drives the instant uptake of efforts, but it also stimulates constant innovation in technologies related to direct drives.

Direct Drive (Gearless) Wind Turbine Market Restraints and Challenges:

One of the major restraints facing the direct drive (gearless) wind turbine market is the high initial capital cost associated with their advanced generator systems and specialized components.

The massive cost of the advanced generator systems and specialized components is one of the major restraining factors on the market for direct drive (gearless) wind turbines. Unlike conventional geared turbines, large permanent magnet synchronous generators (PMSG) in the direct drive models are more difficult to manufacture and also require expensive rare-earth materials, in particular, neodymium and dysprosium. Due to the absence of a gearbox, however, the generator itself needs to be very large and heavy to directly carry the full torque from the rotor-this makes the nacelle bulky. The additional weight makes transportation, installation, and tower design more difficult logistically, especially in offshore projects, where cranes and vessels would have to tackle everything at an increased load. Especially when markets are developing or highly price-sensitive, these systems need to find the strength to challenge that barrier. This also calls for continuous upgradation of lighter-weight materials, magnet technology, and manufacturing processes, to enable the economic competitiveness of gearless designs from the outset.

Direct Drive (Gearless) Wind Turbine Market Opportunities:

There exists a significant opportunity for the direct drive (gearless) wind turbine market on account of global initiatives to invest in large-scale offshore wind projects and increased renewable energy adoption in emerging markets. The offshore installations are rapidly picking up an edge due to higher and more consistent wind speeds, with direct drive turbines being ideally fitted in these environments due to their low maintenance and highly reliable characteristics. Aggressive decarbonization goals are pushing investments wherein many countries are now using offshore wind farms as a crucial ingredient of their energy mix and thereby opening substantial growth opportunities for gearless solutions. Many of the emerging economies of Asia, Latin America, and the Middle East are awakening to the use of renewable energy to meet surging power demands and reduce dependency on fossil fuels. Such regions present excellent opportunities for direct drive turbines, particularly in coastal and island applications where grid expansion is an issue. In addition, advancements in lightweight materials and permanent magnet generators further enable the manufacture of larger, more efficient gearless turbines, making them economically viable even in new markets. All these trends combined provide a great opportunity for direct drive technology to command a larger share of the global wind energy expansion, thereby contributing immensely to the worldwide drive of sustainable energy transition.

Direct Drive (Gearless) Wind Turbine Market Segmentation:

Market Segmentation: By Capacity

• Up to 3 MW

• 3-5 MW

• Above 5 MW

Global direct drive (gearless) wind turbine markets are segmented in terms of capacity into three categories of below 3 MW, 3-5 MW, and above 5 MW. Turbines below the 3-MW range are mainly used for smaller onshore projects and distributed renewable energy applications, especially in rural or community-scale setups, where grid integration becomes easier. These turbines enable power generation at a local level and are appreciated for their lower logistical complexities and easier permitting. The room for the 3-MW- to 5-MW-rated machines is characterized as the mainstream for mid-scale onshore and nearshore installations, balancing output, reliability, and cost. They are well recognized in Europe and North America, where land availability is constrained and moderate wind energy flows prevail. The above 5 MW category is the fastest-growing, driven by the offshore wind boom and the favor towards higher capacity turbines to maximize energy capture in highly windy and consistent wind zones. Developers prefer larger turbines as they can lower the number of units required per farm, thus reducing overall installation and maintenance expenditures. Constant research and development on lightweight materials and modular nacelle designs further encourage the development of this high-capacity segment. On the whole, capacity-based segmentation shows how the market is moving toward bigger, more powerful, and efficient turbines designed for various site-specific needs and policy-driven renewable targets.

Market Segmentation: By Rotor Diameter

• Up to 100 meters

• 100-150 meters

• Above 150 meters

Turbines are further segmented based on rotor diameter: up to 100 meters, 100-150 meters, and above 150 meters. Turbines with rotor diameters below 100 meters are normally employed in some small-scale projects or space-constrained projects, for instance, local onshore farms or island installations, where minimizing land use and visual impacts is paramount. The 100-150 meters category is quite possibly the biggest segment for offshore and nearshore projects around the globe in terms of the optimal mix of swept area for energy capture against structural feasibility. These turbines are especially attractive in areas of moderate wind speeds, allowing operators to increase capacity factors without increasing tower height considerably. On the other hand, turbines above 150 meters in rotor diameter are mainly applicable to large-scale offshore wind farms, where maximizing wind capture from steady and strong ocean winds is crucial. Such ultra-large rotors enhance annual energy production (AEP) to a high extent, thus reducing project cost and allowing the developer to meet stringent renewable energy quotas. Increasing rotor diameters seem to represent a trend that the industry has focused on for maximizing output per turbine while minimizing the environmental and logistical footprints. Segmentation based on rotor diameter, therefore, highlights the influence of design innovation upon the global energy demand and internationally driven paths toward decarbonization.

Market Segmentation: By Application

• Onshore

• Offshore

Meanwhile, in terms of application, the market is split between onshore and offshore segments for deployment. Onshore wind is perhaps the most important application area, benefiting from lower costs of installation, easier conditions for grid integration, and generally more mature regulatory frameworks. Directly driven turbines are gaining increasing popularity in the onshore sector because of low maintenance and relatively higher efficiency, which translates into long-term savings, even though initial investment costs are higher. Within European and North American borders, onshore farms further contribute significantly to national renewable energy strategies, particularly in inland and hilly terrains. The offshore is, however, emerging as the fastest growing, helped by strong government intervention, favorable winds, and the need for massive clean energy generation next to coastal demand centers. Direct drive technology brings a massive advantage for offshore wind farms because the withdrawal of gearbox systems reduces maintenance problems in harsh marine environments and makes the turbines more readily available. Countries, such as China, the U.K., and South Korea, have invested much in offshore wind infrastructures, making the segment marked for dramatic growth till 2030. Application-oriented segmentation indicates the two-pronged approach of the market: Robustly building onshore capacity while growing aggressively offshore to meet global decarbonization and energy security targets.

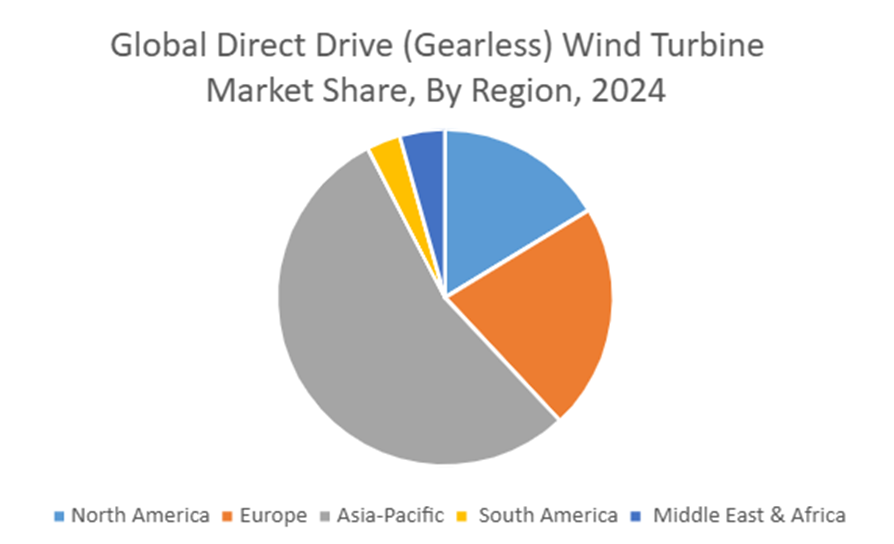

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

Asia-Pacific is the key region for the global direct drive (gearless) wind turbine market, supported by a robust manufacturing ecosystem, the growing number of offshore wind projects in China, and the rapid push by India toward renewable energy to meet its burgeoning power demand. Europe follows closely behind, supported by ambitious decarbonization targets, considerable expansion of offshore wind in the North Sea and Baltic region areas, and a continuous uptick in technological innovation that enhances efficiency and scalability. In North America, a buoyant market is finding further traction due to supportive clean energy policies in the U.S., ongoing grid modernization efforts, and new waves of repowering projects to replace older turbines with newer and more efficient gearless designs. In the Middle East and Africa, the market develops gradually, supported by hybrid solar-wind projects, infrastructure modernization, and coastal wind initiatives that meet sustainability goals. At the same time, growth is steady in South America as an increasing volume of investments by countries like Brazil and Chile in wind energy will diversify their energy mix while reducing reliance on fossil fuels. These developments in all regions represent a global transition toward cleaner and more reliable wind power solutions, of which gearless technology plays a major role in the support of long-term global energy transition strategies.

COVID-19 Impact Analysis on the Direct Drive (Gearless) Wind Turbine Market:

The pandemic of COVID-19 brought in its initial stages big challenges for the direct drive (gearless) wind turbine market, causing havoc in global supply chains, delaying project timelines, and forming a labor shortage with respect to manufacturing and installation. Such lockdowns and travel restrictions made it difficult to transport some of the critical components, such as large permanent magnet generators and specialized tower sections, especially on offshore projects, which heavily rely on coordinated international logistics. Thus, many wind farm development projects saw cost overruns and schedule delays. With a government thrust on economic recovery through green infrastructure investments, the industry initially began recovering quickly. Stimulus packages and renewed policy support in Europe, China, and North America were explicitly in favor of renewable energy and helped accelerate the demand for new wind capacity in the region. Furthermore, the added concern for energy security and decarbonization during the course of the pandemic has only added more optimism to the market for gearless turbines, given that they have less maintenance and higher reliability. Therefore, COVID-19 presented a very short-term challenge in the operations and ultimately added pressure to the strategic importance of resilient clean energy systems, laying the groundwork even for a stronger long-term growth opportunity for the direct drive wind turbine market.

Latest Trends/ Developments:

The global direct drive (gearless) wind turbine market is witnessing phenomenal technological evolution manifested in the fabulous development of ultra-large turbines with high capacity and advanced digital solutions. Manufacturers are truly going to the edge with turbines above 15 MW, and some prototypes above 25 MW, aimed at maximizing offshore energy capture while working to cut down the levelized cost of electricity (LCOE). Innovations in rotor blade materials and designs—such as blades longer than 150 meters—are enhancing aerodynamic efficiency and operational durability, particularly in harsh offshore conditions. On the parallel, the incorporation of digital technologies like IoT-based condition monitoring, predictive maintenance, and AI-driven performance optimization is changing the face of operational reliability and slashing maintenance expenses. There is also a focus on using permanent magnet generators with rare-earth materials to boost efficiency and minimize weight. These trends point to a global surge in larger, smarter, and more resilient turbines that meet high ambitions of renewable energy targets with better economic returns. In this dynamic global scenario of countries pouring investment into offshore wind and coastal projects, these novel gearless designs would act as an important engine for driving sustainable energy into the future.

Key Players:

• Avantis Energy Group

• Enercon

• Godecke Energy

• Siemens Wind Power A/S

• Emergya Wind Technologies B.V

• GE Energy

• Northern Power Systems

• Goldwind Science & Technology Co. Ltd

• Leitwind AG

Chapter 1. Global Direct Drive (Gearless) Wind Turbine Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Direct Drive (Gearless) Wind Turbine Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Direct Drive (Gearless) Wind Turbine Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Direct Drive (Gearless) Wind Turbine Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Direct Drive (Gearless) Wind Turbine Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Direct Drive (Gearless) Wind Turbine Market – By Capacity

6.1. Introduction/Key Findings

6.2. Up to 3 MW

6.3. 3-5 MW

6.4. Above 5 MW

6.5. Y-O-Y Growth trend Analysis By Capacity

6.6. Absolute $ Opportunity Analysis By Capacity, 2025-2030

Chapter 7. Global Direct Drive (Gearless) Wind Turbine Market – By Rotor Diameter

7.1. Introduction/Key Findings

7.2. Up to 100 meters

7.3. 100-150 meters

7.4. Above 150 meters

7.5. Y-O-Y Growth trend Analysis By Rotor Diameter

7.6. Absolute $ Opportunity Analysis By Rotor Diameter, 2025-2030

Chapter 8. Global Direct Drive (Gearless) Wind Turbine Market – By Application

8.1. Introduction/Key Findings

8.2. Onshore

8.3. Offshore

8.4. Y-O-Y Growth trend Analysis By Application

8.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 9. Global Direct Drive (Gearless) Wind Turbine Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Capacity

9.1.3. By Rotor Diameter

9.1.4. By Application

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Capacity

9.2.3. By Rotor Diameter

9.2.4. By Application

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Capacity

9.3.3. By Rotor Diameter

9.3.4. By Application

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Capacity

9.4.3. By Rotor Diameter

9.4.4. By Application

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Capacity

9.5.3. By Rotor Diameter

9.5.4. By Application

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Direct Drive (Gearless) Wind Turbine Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Avantis Energy Group

10.2. Enercon

10.3. Siemens Wind Power A/S

10.4. Godecke Energy

10.5. Emergya Wind Technologies B.V

10.6. GE Energy

10.7. Goldwind Science & Technology Co. Ltd

10.8. Northern Power Systems

10.9. M. Torres Olvega Industrial, S.A. (Spain-based)

10.10. Leitwind AG

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Direct Drive (Gearless) Wind Turbine Market was valued at USD 32.95 billion in 2024 and is projected to reach a market size of USD 63.61 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.06%.

Growing demand for low-maintenance, high-reliability turbines boosts adoption. Rapid offshore wind expansion accelerates the need for gearless technology worldwide.

The Direct Drive (Gearless) Wind Turbine Market by application is segmented into onshore and offshore. Onshore focuses on land-based farms, while offshore targets large-scale marine wind projects.

Asia-Pacific is the most dominant region for the Direct Drive (Gearless) Wind Turbine Market.

Avantis Energy Group, Enercon, Godecke Energy, Siemens Wind Power A/S, Emergya Wind Technologies B.V., GE Energy, Northern Power Systems, and Goldwind Science & Technology Co., Ltd are the key players in the Direct Drive (Gearless) Wind Turbine Market.