Chillers Market Research Report – Segmentation by Type (Screw Chillers, Scroll Chillers, Centrifugal Chillers, Absorption Chillers, Reciprocating Chillers); By Distribution Channel (Direct Sales, Distributors, Online Retail, OEM Partnerships, System Integrators); By Cooling Capacity (Less than 50 tons, 50-150 tons, 150-300 tons, 300-500 tons, Above 500 tons); By End-User Industry (Commercial Buildings, Industrial Manufacturing, Healthcare, Hospitality, Data Centers, Food and Beverage Processing); By Compressor Type (Scroll Compressors, Screw Compressors, Centrifugal Compressors, Reciprocating Compressors, Absorption Systems); By Refrigerant Type (HFC Refrigerants, HFO Refrigerants, Natural Refrigerants, Hydrocarbon Refrigerants, HCFC Refrigerants (Phasing Out)); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-7980

Format:

Region: Global

Market Size and Overview:

The Chillers Market was valued at USD 12.08 Billion in 2024 and is projected to reach a market size of USD 15.42 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 5%.

The global chillers market is experiencing robust growth in 2024, driven by increasing industrialization, growing HVAC demands in commercial buildings, and technological advancements in energy-efficient cooling solutions. Chillers, essential components in large-scale air conditioning systems, are witnessing heightened demand as urbanization accelerates worldwide and commercial infrastructure expands. The market has evolved significantly with the integration of smart technologies, IoT capabilities, and environmentally friendly refrigerants that comply with stringent global regulations on greenhouse gas emissions. Industrial sectors, particularly food processing, pharmaceuticals, and plastics manufacturing, continue to be major consumers of industrial chillers due to precise temperature control requirements in their production processes. Meanwhile, the commercial building sector maintains substantial demand for HVAC chillers in offices, hospitals, hotels, and educational institutions. Price sensitivity varies significantly across market segments, with industrial applications typically prioritizing performance and reliability over initial costs, while commercial applications often balance capital expenditure against long-term operational efficiency.

Key Market Insights:

Energy-efficient models now represent approximately 62% of new installations, reflecting growing sustainability concerns across industries. The average capacity of newly installed chillers has increased by 8.5% compared to previous years, indicating a trend toward larger cooling systems in commercial and industrial applications.

Water-cooled chillers maintain a dominant 54% market share based on cooling capacity, though air-cooled systems lead in unit sales with 61% of total unit shipments.

Scroll compressors featured in 47% of all chillers sold globally, with screw compressors accounting for 33% and centrifugal compressors claiming 18% of the market.

Approximately 38% of chillers now incorporate smart control systems enabling remote monitoring and predictive maintenance capabilities.

Market Drivers:

Stringent energy efficiency regulations and rising operational costs have propelled energy efficiency to the forefront of chillers market growth.

Commercial building owners and industrial operators face mounting pressure to reduce their carbon footprint while simultaneously cutting operational expenses, creating ideal conditions for high-efficiency chiller adoption. Modern chillers incorporating variable speed drives, improved heat exchangers, and advanced controls can deliver 30-40% energy savings compared to systems installed just a decade ago. This compelling economic proposition has accelerated replacement cycles even in markets traditionally resistant to capital expenditures. Additionally, various government incentive programs and tax benefits specifically targeting energy-efficient cooling systems have reduced payback periods significantly, making these premium solutions financially attractive even for budget-conscious customers. The emergence of building certification standards like LEED and BREEAM, which award points for efficient HVAC systems, has further cemented energy efficiency as the primary purchase consideration for new chillers in commercial applications.

The integration of smart technologies and IoT capabilities has fundamentally transformed the chillers market, driving growth through enhanced functionality and operational improvements.

Modern chillers increasingly feature sophisticated control systems that optimize performance based on real-time conditions, predictive maintenance capabilities that identify potential failures before they occur, and remote monitoring solutions that enable centralized management of distributed cooling infrastructure. These technological advances deliver tangible benefits including reduced downtime, extended equipment lifespan, and optimized energy consumption that can adapt to changing load requirements throughout the day. The data analytics capabilities built into these systems allow facility managers to generate comprehensive efficiency reports, identify performance trends, and implement continuous improvement strategies. Furthermore, the development of new compressor designs and improved refrigeration cycles has enabled manufacturers to achieve higher Coefficient of Performance values while reducing physical footprints, making advanced chillers suitable for installations with space constraints. These innovations have expanded the addressable market while creating new premium segments for technologically advanced solutions.

Market Restraints and Challenges:

The chillers market faces significant challenges including high initial investment costs for premium energy-efficient models, creating barriers particularly for small and medium enterprises. Supply chain disruptions continue to impact component availability and lead times. Shortages of skilled technicians for installation and maintenance of advanced systems hamper market growth, especially in emerging economies. Additionally, retrofitting existing buildings with modern chiller systems often requires extensive modifications to infrastructure, limiting replacement rates in established markets.

Market Opportunities:

Rapid growth in data centre cooling requirements presents substantial opportunities, with increasing server density demanding more efficient cooling solutions. The transition to low-GWP refrigerants creates a natural replacement cycle as regulations phase out traditional refrigerants. District cooling projects in urban development's offer large-scale implementation opportunities for industrial chillers. Growing demand for process cooling in pharmaceutical manufacturing, particularly for vaccine production, expands the addressable market. Integration with renewable energy systems, including solar cooling technologies, opens new market segments for environmentally conscious customers.

Market Segmentation:

Segmentation by Type:

• Screw Chillers

• Scroll Chillers

• Centrifugal Chillers

• Absorption Chillers

• Reciprocating Chillers

Scroll chillers command 41% of the global market share by units sold, dominating the small to medium capacity range (20-200 tons). Their popularity stems from excellent part-load efficiency, relatively compact footprint, and lower maintenance requirements compared to reciprocating alternatives. Healthcare facilities and small commercial buildings particularly favor scroll technology for its reliability and quieter operation.

Centrifugal chillers are experiencing the fastest growth at 14.2% annually, driven by increasing demand for large-capacity cooling solutions in district energy systems and extensive commercial complexes. Their superior efficiency at high capacities (above 300 tons), ability to operate with low-pressure refrigerants, and excellent performance in variable load applications make them increasingly attractive despite higher initial costs.

Segmentation by Distribution Channel:

• Direct Sales

• Distributors

• Online Retail

• OEM Partnerships

• System Integrators

Direct sales account for 46% of market revenue as manufacturers prioritize direct relationships with end users for large commercial and industrial installations. This channel provides manufacturers with higher margins while offering customers customized solutions, comprehensive service agreements, and direct technical support. Commercial buildings and industrial processors typically prefer direct relationships for mission-critical cooling infrastructure.

Online retail distribution is experiencing 18.7% annual growth, revolutionizing how smaller chillers reach the market. This channel's expansion is fueled by improved digital visualization tools, standardized specifications, and competitive pricing transparency. Small business owners increasingly purchase replacements and standardized units online, attracted by convenience, comparative shopping capabilities, and accelerated procurement processes.

Segmentation by Cooling Capacity:

• Less than 50 tons

• 50-150 tons

• 150-300 tons

• 300-500 tons

• Above 500 tons

Small capacity chillers under 50 tons dominate the market with 54%-unit share, serving small commercial buildings, medical offices, and light industrial applications. Their popularity stems from lower capital costs, simplified installation requirements, and flexibility for zone-specific cooling. This segment benefits from standardization that enables more competitive pricing and faster replacement cycles.

Large capacity chillers exceeding 500 tons are growing at 16.3% annually, driven by expanding data centers, district cooling projects, and large manufacturing facilities. The efficiency advantages of centralized cooling for large facilities, coupled with improved variable-load performance of modern large chillers, make these systems increasingly attractive despite substantial initial investment requirements.

Segmentation by End-User Industry:

• Commercial Buildings

• Industrial Manufacturing

• Healthcare

• Hospitality

• Data Centers

• Food and Beverage Processing

Commercial buildings account for 39% of chiller installations globally, maintaining market dominance through consistent demand from offices, retail centers, and educational institutions. The segment's stability derives from ongoing construction in developing markets and replacement cycles in established regions. Energy efficiency requirements in building codes continue driving upgrades to more advanced chiller systems.

Data centers represent the fastest-growing end-user segment at 27.3% annual growth, driven by exponential increases in cloud computing capacity and edge computing infrastructure. The critical cooling requirements of high-density server installations demand precision cooling solutions with redundancy features. This segment increasingly adopts liquid cooling technologies and specialized chillers designed for continuous operation under heavy loads.

Segmentation by Compressor Type:

• Scroll Compressors

• Screw Compressors

• Centrifugal Compressors

• Reciprocating Compressors

• Absorption Systems

Scroll compressors lead the market with 47% share due to their versatility across various applications and capacity ranges. Their dominance stems from excellent reliability, good part-load efficiency, and relatively quiet operation. The technology's mature manufacturing processes enable competitive pricing while providing sufficient efficiency for most standard applications in commercial cooling.

Centrifugal compressor technology is growing at 15.1% annually, driven by advancements in magnetic bearings and variable speed capabilities. These innovations have dramatically improved efficiency while reducing maintenance requirements and extending operational lifespans. The technology particularly excels in large capacity applications where their superior efficiency at consistent loads creates compelling long-term operational savings.

Segmentation by Refrigerant Type:

• HFC Refrigerants

• HFO Refrigerants

• Natural Refrigerants

• Hydrocarbon Refrigerants

• HCFC Refrigerants (Phasing Out)

HFC refrigerants maintain 52% market share despite regulatory pressure, due to established infrastructure, technician familiarity, and proven reliability. Their continued dominance reflects the significant installed base and gradual nature of refrigerant transitions. Market leaders have optimized HFC chiller designs to maximize efficiency while complying with current regulations.

HFO refrigerants are experiencing 23.5% annual growth as the primary replacement for high-GWP alternatives. Their rapid adoption is driven by regulatory compliance advantages, minimal system modification requirements compared to natural refrigerants, and performance characteristics similar to HFCs. Manufacturing capacity expansion has improved availability while reducing the price premium over traditional options.

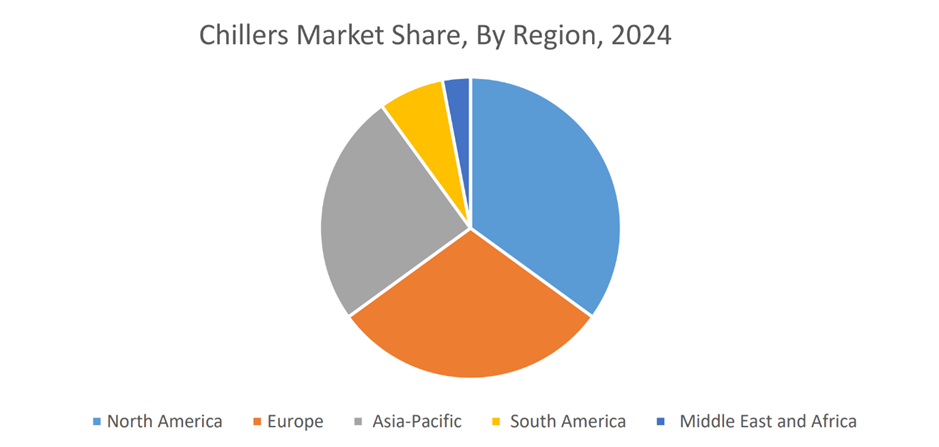

Segmentation by Regional Analysis:

• North America

• Europe

• Asia Pacific

• South America

• Middle East and Africa

The North American market holds 35% share, dominating global chillers revenue due to technological adoption and strict efficiency standards. Europe follows at 30%, with particular strength in sustainable cooling solutions. Asia-Pacific represents 25% of the market and demonstrates the fastest growth at 9.7% annually, driven by rapid industrialization in China and India. North America's dominance stems from aggressive replacement of aging infrastructure, while Asia-Pacific's growth reflects massive new construction and industrial expansion projects requiring state-of-the-art cooling systems.

COVID-19 Impact Analysis:

The pandemic initially disrupted the chillers market through supply chain complications and installation delays, causing a 6.8% contraction in 2020. However, 2021-2024 saw accelerated recovery driven by heightened awareness of indoor air quality and ventilation systems. Healthcare facility expansions created unexpected demand, while manufacturing relocations to ensure supply chain resilience generated new installation opportunities. The crisis ultimately accelerated digital transformation, with remote monitoring capabilities becoming standard requirements rather than premium features.

Latest Trends and Developments:

The integration of artificial intelligence for self-optimizing chiller systems represents the cutting edge of market innovation in 2024. Manufacturers are increasingly incorporating heat recovery functionality that captures and repurposes waste heat for domestic water heating or other processes. Low-charge ammonia systems are gaining traction in industrial applications, offering natural refrigerant benefits with improved safety profiles. Modular, prefabricated chiller plants that reduce installation complexity and time are seeing increased adoption. Additionally, thermal energy storage integration allows chillers to operate during off-peak hours, reducing operational costs while providing grid stabilization benefits.

Key Players in the Market:

• Johnson Controls International

• Daikin Industries

• Trane Technologies

• Carrier Global Corporation

• Mitsubishi Electric Corporation

• LG Electronics

• Midea Group

• Danfoss

• Ingersoll Rand

• York (Johnson Controls)

Chapter 1. CHILLERS MARKET – Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. CHILLERS MARKET – Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-19 Impact Analysis

2.3.1. Impact during 2023 – 2030

2.3.2. Impact on Supply – Demand

Chapter 3. CHILLERS MARKET – Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4. CHILLERS MARK ET - Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. CHILLERS MARKET - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. CHILLERS MARKET – By Type

6.1. Screw Chiller

6.2. Scroll Chiller

6.3. Centrifugal Chiller

6.4. Others

Chapter 7. CHILLERS MARKET – By Product Type

7.1. Air Cooled Chiller

7.2. Water Cooled Chiller

Chapter 8. CHILLERS MARKET – By Power Range

8.1. Less than 50 kW

8.2. 50-200 kW

8.3. More than 200 kW

Chapter 9. CHILLERS MARKET – By End User

9.1 Chemicals & Petrochemicals

9.2. Food & Beverages

9.3. Medical

9.4. Others

Chapter 10. CHILLERS MARKET – By Region

10.1. North America

10.2. Europe

10.3.The Asia Pacific

10.4.Latin America

10.5. Middle-East and Africa

Chapter 11. CHILLERS MARKET– Company Profiles – (Overview, Product Portfolio, Financials, Developments)

11.1. Company 1

11.2. Company 2

11.3. Company 3

11.4. Company 4

11.5. Company 5

11.6. Company 6

11.7. Company 7

11.8. Company 8

11.10. Company 10

11.10. Company 10

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Stringent regulations and rising operational costs are pushing building owners and industrial operators to adopt high-efficiency chillers that can deliver 30-40% energy savings compared to older systems. Government incentives, tax benefits, and building certification standards like LEED further encourage adoption.

Premium energy-efficient models have substantial upfront costs, creating adoption barriers particularly for small and medium enterprises.

The global chillers market is dominated by fifteen key manufacturers: Johnson Controls International, Daikin Industries, Trane Technologies, Carrier Global Corporation, Mitsubishi Electric Corporation, LG Electronics, Midea Group, Danfoss, Ingersoll Rand, York (Johnson Controls), Hitachi, Thermax Limited, Kirloskar Chillers, Arctic Chiller Group, and Blue Star Limited.

North America currently holds the largest market share, estimated around 35%.

Asia Pacific has shown significant room for growth in specific segments.