Global Carbon Nanotubes Market Research Report – Segmentation by Product Type (Multi-Walled Carbon Nanotubes (MWCNTs), and Single-Walled Carbon Nanotubes (SWCNTs)), Application (Polymers and composites, Electrical & electronics, Energy storage, Biomedical and healthcare, Aerospace and Defence, Construction and infrastructure, and Others), Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16509

Format:

Region: Global

Market Size and Overview:

The Global Carbon Nanotubes Market was valued at USD 6.6 billion in 2024 and will grow at a CAGR of 13% from 2025 to 2032. Forecasts project market by USD 12.16 billion by 2030.

The Carbon Nanotubes Market focuses on cylindrical carbon allotropes with extraordinary mechanical strength, electrical and thermal conductivity, and high aspect ratio characteristics. These materials, available as single-walled (SWCNT) and multi-walled (MWCNT) types, are increasingly used in polymers, electronics, energy storage, aerospace, automotive components, biomedical devices, and environmental applications. The market expansion is underpinned by the scaling of CVD-based industrial production, innovation in composite materials, and rising government-backed nanotech funding in major regions worldwide.

Key market insights:

Multi-walled carbon nanotubes (MWCNTs) dominate product-wise, accounting for over 93% of market share in 2024 due to their cost-effectiveness, mechanical performance, and scalable production.

Polymers and composites represent the leading application segment, capturing nearly 70% of demand in 2024; CNTs are used to enhance mechanical, thermal, and electrical properties.

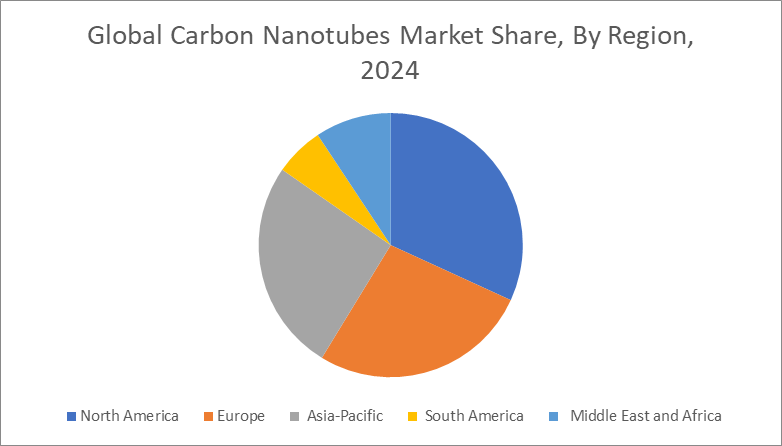

Asia-Pacific leads geographically, with 33–54% of market share in 2024, driven by China, Japan, and South Korea’s electronics, automotive, and solar industries.

North America and Europe are growing rapidly: North America is expected to grow at ~12–13% CAGR led by R&D and battery/defense demand; Europe emphasizes traceability in aerospace and semiconductor uses.

High-performance SWCNTs, though currently just 6–7% of the market, are the fastest-growing segment (~11–16% CAGR) driven by demand in electronics, energy storage, and biomedical research.

Major manufacturing methods rely on chemical vapor deposition (CVD), especially catalytic versions (CCVD), favored for high purity and scale.

Increasing investment in nanotech from governments (China, US, India, Japan) and corporations is fostering partnerships and infrastructure to support industrial-scale CNT manufacture.

Emerging biomedical and energy storage applications—like drug delivery systems, biosensors, and ultra-capacitors—are expected to substantially broaden CNT utilization.

Global Carbon Nanotubes Market Drivers

Expanding use in composites for automotive and aerospace is driving the market growth

The carbon nanotubes market is propelled by their extensive application in advanced polymer, metal, and ceramic composites across automotive and aerospace industries. MWCNTs are favored due to their superior mechanical strength, thermal conductivity, and electrical performance, which help reduce weight while maintaining structural integrity. In vehicles and aircraft, weight savings directly translate into improved fuel efficiency or range. The demand is surged by the automotive industry's shift toward lightweight electric vehicle components and aerospace’s push for high-strength, lightweight materials in airframes and satellites. Governments and industry associations support composite technology through funding and regulatory initiatives emphasizing safer, greener transport. As CNT composites are integrated into structural parts, heat exchangers, adhesives, and coatings, OEMs increasingly collaborate with CNT suppliers to co-develop tailored material grades. These partnerships deepen adoption and accelerate market growth across value-added mobility sectors.

Construction of scalable CVD plants and manufacturing infrastructure is driving the market growth

Global CNT production is scaling up, driven by expansion of catalytic chemical vapor deposition plants capable of delivering high purity MWCNTs and SWCNTs at industrial volumes. Led by companies in China, U.S., Europe, and India, capacity expansions increase output while reducing costs. Technological innovations such as flame-assisted CVD allow mass production of SWCNTs at significantly lower prices—estimations point to potential cost reduction from over USD 1,000/kg to around USD 80/kg. Major investments, such as Serbia’s new facility for TUBALL SWCNT, coupled with government-backed nanotech grants and partnerships, strengthen manufacturing ecosystems. This improving economy of scale makes CNT technology accessible to more industrial applications, fueling further demand and integration in established markets.

Diversification into energy storage and biomedical sectors is driving the market growth

Carbon nanotubes are entering high-value application verticals like energy storage and healthcare. Biomedical uses include drug delivery systems, biosensors, hyperthermia cancer treatments, and bioscaffolds, leveraging CNTs’ high surface area, tunability, and ability to penetrate cells. Energy applications exploit the high conductivity and surface properties of SWCNTs in battery anodes, supercapacitors, and high-density energy storage—recent research shows twisted CNTs storing three times more energy per mass than lithium-ion equivalents. As researchers and firms develop scalable production methods and regulatory frameworks for medical-grade CNTs, these application areas promise to significantly widen the market beyond industrial uses into consumer health and energy innovation.

Global Carbon Nanotubes Market Challenges and Restraints

High production cost and scalability limitations is restricting the market growth

Despite growing capacity, CNT production remains relatively costly compared to traditional materials. SWCNTs are particularly expensive, with early sub-kilogram pricing exceeding USD 1,000/kg. While recent innovations in flame-CVD may lower costs, these require further validation at scale. CVD plants involve high capital investment and technical complexity. Controlling uniformity, purity, and nanotube length distribution remains difficult and adds to cost. This restricts commercial adoption to high-value applications where premium prices are justified. Until costs decline significantly and standardized supply systems emerge, CNTs may struggle to penetrate medium-performance composites and lower-margin markets.

Health and environmental safety concerns is restricting the market growth

Toxicology studies highlight potential health hazards of CNT exposure, particularly those that mimic asbestos-like behavior in lung tissue and cross biological membranes. Chronic inhalation or dermal exposure can cause inflammation, fibrosis, or granulomas in animal models. Regulatory scrutiny is increasing as CNT-enabled medical and consumer products approach the market. Companies must perform detailed risk assessments, implement occupational safety protocols, and track life-cycle impacts. Public acceptance may be hindered by safety concerns. These factors increase time-to-market and regulatory compliance costs, discouraging some enterprises from investing in CNT technologies until safety profiles are fully established.

Lack of standardization and regulatory frameworks is restricting the market growth

The diverse nature of CNT products—varying by wall count, length, purity, and functionalization—complicates standardization efforts. In the absence of unified industry norms, applications in regulated sectors like aerospace and medical devices face additional entry barriers due to the need for traceability and certifications. Europe is pushing for cradle-to-gate emissions reporting and safety validation; the U.S. National Nanotechnology Initiative and REACH registration in Europe drive transparency, but global harmonization is lacking . This fragmentation hinders cross-border trade and delays large-scale industry adoption, particularly in government procurement or international supply chains that require unified compliance standards.

Market opportunities

Opportunities in the carbon nanotubes market span across technological, regional, and application-driven dimensions. One of the most promising paths lies in SWCNT production cost reduction through innovative manufacturing like flame-assisted CVD and scalable catalytic CVD platforms. Lower cost per kilogram will allow SWCNTs to penetrate broader electronics, energy storage, and sensor markets, currently dominated by MWCNTs—creating a new wave of adoption in flexible electronics, capacitors, transparent conductive films, and medical devices. Biomedical applications offer another expanding frontier. CNT-enabled drug delivery systems, biosensors, tissue scaffolds, and hyperthermia therapies are gaining traction as research advances show precise targeting, enhanced bioavailability, and unique thermal properties suitable for applications like Boron Neutron Capture Therapy. As FDA and EMA guidelines evolve and safety data accumulates, expect partnerships between nanotech firms and pharmaceutical/medical device companies to increase. Licensed SWCNT-based therapies or diagnostics may significantly broaden commercial deployment and drive investment. Energy storage is a further growth engine. SWCNT-based or twisted CNT electrodes are under investigation to improve capacity and energy density in batteries, supercapacitors, and implantable energy sources . Integration into next-gen battery chemistries, e.g., sodium-ion, lithium-sulfur, or flexible formats, will create high-growth niche markets. As renewable energy systems expand, materials enabling efficient grid storage and EV performance will gain traction. Environmental remediation and smart infrastructure also present opportunities. CNT-enhanced concrete, with improved strength and lower carbon footprints, can transform construction—research has shown tensile and compressive improvements of 14–35% with low CNT loading . CNT water filtration membranes for desalination or anti-microbial coatings can address water scarcity and infrastructure resilience priorities. Combined with growing green building regulations, these applications could yield high-value commercialization scales.

Market segmentation

By Type

• Multi-Walled Carbon Nanotubes (MWCNTs)

• Single-Walled Carbon Nanotubes (SWCNTs)

Multi-walled carbon nanotubes (MWCNTs) dominate the product segment, comprising over 93% of market revenue in 2024. They are preferred due to their balance of performance, scalability, and cost. MWCNTs enhance composite strength, conductivity, and thermal stability at lower prices than SWCNTs. Their production via established CVD methods is mature, industrial-scale, and widely available. As such, MWCNTs are the base for most industrial applications, from automotive composites to conductive polymers. Ongoing volume-based cost reductions further solidify their lead. While SWCNTs are gaining traction in niche sectors, MWCNTs remain the backbone of CNT commercialization, spanning low- to high-value markets due to their versatility and cost advantage.

By Application

• Polymers and composites

• Electrical & electronics

• Energy storage

• Biomedical and healthcare

• Aerospace and defense

• Construction and infrastructure

• Others (filters, coatings)

Polymers and composites lead application segmentation, accounting for nearly 70% of global CNT use in 2024. CNTs are incorporated into polymer matrices to reinforce structural parts, improve thermal and electrical conductivity, and reduce weight in sectors like automotive, aerospace, electronics, and consumer goods. Composites enabled by CNTs deliver performance levels unattainable with conventional fillers, making them critical in lightweight and high-strength material development. Supply chains are well-established, with CNT-infused resins, masterbatches, and prepregs available commercially. The dominance stems from the broad industrial need for enhanced material properties and the relative ease of integrating CNTs into polymer systems at scale.

Regional segmentation

• North America

• Asia Pacific

• Europe

• South America

• Middle East & Africa

Asia-Pacific is the dominant region in the global CNT market, accounting for 33–54% of revenue in 2024. China leads with industrial-scale production driven by low-cost CVD plants, government funding, and demand from electronics, solar panels, and automotive manufacturers. Japan and South Korea also contribute through advanced SWCNT technologies and electronics applications. India is emerging fast with an 18% CAGR projected from USD 117 million in 2024 to USD 317 million in 2030. The region benefits from abundant raw materials, skilled nanotech talent, and aggressive public-private R&D programs. Europe and North America follow, focusing on high-value aerospace, defense, medical, and semiconductor uses. However, Asia-Pacific’s combination of scale, pricing, and policy support firmly establishes it as the center of gravity for CNT growth.

COVID-19 Impact Analysis on the Carbon Nanotubes Market

The COVID-19 pandemic had mixed effects on the carbon nanotubes market. Early disruptions in 2020 caused production slowdowns due to locked-down CVD facilities, material supply chain interruptions, and global logistics constraints. This led to temporary shortages and delays in composite parts and CNT-enabled products. However, governments in China, North America, and Europe continued funding nanotech research—such as stimulus through national nanomaterials programs—which cushioned the impact. As industries pivoted to healthcare applications, interest in CNT-based biosensors, PPE coatings, and high-performance medical composites increased. By late 2021, operations rebounded, aided by improved plant safety protocols and diversified supply chains. Pandemic-era innovations like contactless manufacturing and remote monitoring enhanced facility efficiency. By 2022–2023, CNT demand in electronics and energy sectors surged, propelled by the global semiconductor shortage and green energy investments. Application growth outpaced early-year downturns, supporting market CAGR recovery. Supply chain resilience investments—onshoring, dual sourcing, and inventory buffers—were implemented by key producers. Overall, pandemic-era turbulence slowed but did not derail long-term CNT adoption. Instead, it prompted structural changes in production and application that strengthened market fundamentals for future growth.

Latest trends/Developments

Recent years have seen transformative trends in the carbon nanotubes market across manufacturing, application, and sustainability dimensions. Production innovations include flame-assisted and catalytic CVD methods for SWCNTs that reduce costs dramatically—potentially lowering SWCNT pricing to USD 80/kg . Serbia-based facility expansions and TUBALL T100-ton shifts are revitalizing Europe’s CNT manufacturing capacity. In applications, biomedical breakthroughs using CNTs for targeted drug delivery, biosensing, and hyperthermia therapies are gaining research traction. Energy storage sees CNTs used in novel battery and supercapacitor designs, including twisted-CNT electrodes with triple lithium-ion energy density. CNT-enhanced concrete and autoclave-free curing methods are emerging in construction, improving strength while reducing carbon emissions.

Sustainability-driven innovation shines through efforts to derive CNTs from plastic waste using energy-efficient flash Joule heating—offering potential to produce high-performance CNTs from mixed plastic waste with drastically lower emissions. This aligns with circular economy goals and could decentralize CNT production in emerging markets. Finally, digital and blockchain tracing of CNT supply chains is growing to ensure purity, origin, and life cycle transparency—especially important for medical and aerospace customers. As standardization and regulatory clarity improve, these trends collectively indicate a smarter, safer, and more sustainable future for CNT technologies.

Key Players:

• OCSiAl

• Cabot Corporation

• Arkema SA

• Hanwha Solutions Chemical Division

• CHASM Advanced Materials

• Nanocyl SA

• Jiangsu Cnano Technology

• Nan-meta (CarbonMeta)

• Kumho Petrochemical

• LG Chem

Chapter 1. Global Carbon Nanotubes (CNT) Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Carbon Nanotubes (CNT) Market – Executive Summary

2.1. Market Size & Forecast – (2025–2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Carbon Nanotubes (CNT) Market – Competitive Landscape

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Strategic Alliances, M&A, Joint Ventures

3.4. Vendor Mapping & Ecosystem Overview

Chapter 4. Global Carbon Nanotubes (CNT) Market Entry Scenario

4.1. Regulatory Landscape

4.2. Key Start-up Case Studies

4.3. Customer Adoption & Analysis

4.4. PESTLE Analysis

4.5. Porter’s Five Forces Analysis

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Power of Buyers

4.5.3. Threat of New Entrants

4.5.4. Threat of Substitutes

4.5.5. Industry Rivalry

Chapter 5. Global Carbon Nanotubes (CNT) Market – Key Market Dynamics

5.1. Market Drivers

5.2. Market Restraints

5.3. Market Opportunities

5.4. Emerging Technologies & Innovations

Chapter 6. Global Carbon Nanotubes (CNT) Market – By Type

6.1. Multi-Walled Carbon Nanotubes (MWCNTs)

6.2. Single-Walled Carbon Nanotubes (SWCNTs)

6.3. Y-o-Y Growth Analysis by Type

6.4. Absolute $ Opportunity by Type (2025–2030)

Chapter 7. Global Carbon Nanotubes (CNT) Market – By Application

7.1. Polymers and Composites

7.2. Electrical & Electronics

7.3. Energy Storage

7.4. Biomedical and Healthcare

7.5. Aerospace and Defense

7.6. Construction and Infrastructure

7.7. Others

7.8. Y-o-Y Growth Analysis by Application

7.9. Absolute $ Opportunity by Application (2025–2030)

Chapter 8. Global Carbon Nanotubes (CNT) Market – Regional Analysis

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Type

8.1.3. By Application

8.1.4. Country-level Attractiveness

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Type

8.2.3. By Application

8.2.4. Country-level Attractiveness

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia Pacific

8.3.2. By Type

8.3.3. By Application

8.3.4. Country-level Attractiveness

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Type

8.4.3. By Application

8.4.4. Country-level Attractiveness

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. UAE

8.5.1.2. Saudi Arabia

8.5.1.3. South Africa

8.5.1.4. Nigeria

8.5.1.5. Egypt

8.5.1.6. Kenya

8.5.1.7. Rest of MEA

8.5.2. By Type

8.5.3. By Application

8.5.4. Country-level Attractiveness

Chapter 9. Global Carbon Nanotubes (CNT) Market – Company Profiles

(Overview, Product Portfolio, Financials, Strategies & SWOT)

9.1. OCSiAl

9.2. Cabot Corporation

9.3. Arkema SA

9.4. Hanwha Solutions Chemical Division

9.5. CHASM Advanced Materials

9.6. Nanocyl SA

9.7. Jiangsu Cnano Technology

9.8. Nan-meta (CarbonMeta)

9.9. Kumho Petrochemical

9.10. LG Chem

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Carbon Nanotubes Market was valued at USD 6.6 billion in 2024 and will grow at a CAGR of 13% from 2025 to 2032. Forecasts project market by USD 12.16 billion by 2030.

Drivers include expanding use in automotive/aerospace composites, scaled CVD production infrastructure, and emerging biomedical/energy applications.

Segments by product include MWCNTs and SWCNTs; by application, they include polymers/composites, electronics, energy storage, biomedical, aerospace, and infrastructure.

Asia Pacific leads, accounting for about one third to one half of global demand in 2024 due to China, Japan, South Korea, and India’s manufacturing and policy support.

Leading players include OCSiAl, Cabot Corporation, Arkema, CHASM, Nanocyl, Jiangsu Cnano, LG Chem, Showa Denko, and CarbonMeta.