Global Biofertilizers Market Research Report – Segmentation by Product (Nitrogen Fixing, Phosphate Solubilizing, Other Products); By Application (Seed Treatment and Soil Treatment); By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Other Crop Types); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-3643

Format:

Region: Global

Market Size and Overview:

The Global Biofertilizers Market was valued at USD 2.53 billion in 2024 and is projected to reach a market size of USD 6.11 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 19.3%.

The Biofertilizers market is rapidly gaining momentum as agriculture shifts toward more sustainable, eco-friendly, and organic farming practices. Biofertilizers are natural substances containing living microorganisms that enhance soil fertility by fixing atmospheric nitrogen, solubilizing phosphorus, and stimulating plant growth through the synthesis of beneficial substances. Unlike chemical fertilizers, biofertilizers improve soil health over time, reduce environmental harm, and promote balanced nutrient cycles. Growing concerns over soil degradation, chemical runoff, and climate change are encouraging farmers, policymakers, and agribusinesses to adopt biological alternatives that support long-term productivity without harming ecosystems. With growing global food demand and rising awareness of organic produce, the biofertilizers market is poised to play a crucial role in reshaping the future of sustainable agriculture.

Key Market Insights:

The global shift toward organic and sustainable farming is accelerating biofertilizer adoption, with over 70% of organic farms now using bio-based inputs to maintain soil health and improve crop yields. Farmers are increasingly seeking alternatives to chemical fertilizers to meet both environmental standards and consumer demand for residue-free produce. As a result, the use of nitrogen-fixing and phosphate-solubilizing biofertilizers has seen a sharp rise in row crops, cereals, and pulses, especially in regions focused on soil conservation.

Governments and agricultural bodies across multiple countries are actively promoting biofertilizers through subsidies, awareness campaigns, and training programs, with more than 60 countries currently having national-level support initiatives in place. These efforts are not only improving adoption rates but also encouraging local production of biofertilizers, thereby reducing dependency on synthetic imports.

Technological advancements in microbial formulation and fermentation processes are improving the shelf life, potency, and field performance of biofertilizers, leading to wider acceptance among conventional and commercial farmers. About 55% of agri-input manufacturers are now investing in R&D to develop climate-resilient and crop-specific biofertilizer products. This innovation-driven approach is helping bridge the performance gap between bio and chemical fertilizers, making the former more competitive and attractive for large-scale farming operations.

Biofertilizers Market Drivers:

Increasing Demand for Organic Food and Sustainable Farming Practices Is Fueling the Adoption of Biofertilizers Across the Agriculture Sector

The rising consumer preference for organic and chemical-free produce is significantly boosting the demand for biofertilizers, as farmers and food producers respond to this shift with eco-friendly cultivation methods. Consumers are becoming more conscious of the environmental and health impacts of synthetic inputs, prompting a strong move toward sustainable farming. Biofertilizers, which rely on living microorganisms to naturally enhance soil fertility and crop productivity, align perfectly with the core principles of organic agriculture. As organic food demand rises in both developed and developing countries, farmers are under increasing pressure to reduce their reliance on chemical fertilizers and adopt more sustainable alternatives. This transition is further supported by retail and export markets that favor organically certified products, positioning biofertilizers as a vital input in the global shift toward greener food production.

Government Initiatives, Subsidies, and Policy Support Are Strengthening the Role of Biofertilizers in National Agricultural Frameworks

Many governments around the world are actively promoting the use of biofertilizers through favorable policies, financial subsidies, and training programs aimed at reducing chemical fertilizer dependency and improving soil health. These initiatives are often part of broader national agendas focused on sustainable agriculture, environmental conservation, and rural development. Public sector support is playing a crucial role in rising awareness among farmers, particularly in developing regions where access to agricultural education and alternative inputs is limited. Through demonstration projects, farmer workshops, and incentive schemes, governments are helping accelerate biofertilizer adoption across different crop types and agro-climatic zones. This top-down encouragement is creating a supportive ecosystem for local biofertilizer producers and encouraging innovation, ensuring the long-term viability and scalability of the sector.

Rising Awareness of Soil Health Degradation and the Need for Eco-Friendly Inputs Are Driving a Shift Away from Synthetic Fertilizers

With increasing concerns over soil degradation, nutrient depletion, and the long-term impact of chemical fertilizers on agricultural ecosystems, there is a growing awareness of the benefits of biofertilizers in restoring and maintaining soil vitality. Prolonged use of synthetic fertilizers has been linked to reduced microbial diversity, soil compaction, and declining crop responsiveness—all of which threaten the sustainability of food production. In contrast, biofertilizers promote natural nutrient cycling, improve soil structure, and enhance microbial life, making them an essential tool for regenerative agriculture. Farmers and agronomists are beginning to recognize that sustainable yields require healthy soil biology, and biofertilizers offer a proven, nature-aligned solution. As this awareness grows, especially among large-scale commercial growers and export-oriented farms, the market for biofertilizers is seeing steady expansion.

Technological Advancements in Microbial Research and Product Development Are Enhancing the Efficiency and Commercial Viability of Biofertilizers

Advances in biotechnology, fermentation processes, and microbial strain development are making biofertilizers more potent, reliable, and user-friendly than ever before. Research institutions and agri-tech companies are investing in crop-specific and region-specific formulations that deliver consistent results across varied soil types and climates. These modern biofertilizers come with improved shelf life, better packaging, and ease of application, helping them compete directly with chemical alternatives. In addition, innovations like encapsulated microorganisms, liquid biofertilizers, and smart delivery systems are addressing the previous limitations of traditional products. With better performance and stronger scientific validation, farmers are gaining confidence in the efficiency of biofertilizers as both a standalone and complementary input.

Biofertilizers Market Restraints and Challenges:

Limited Farmer Awareness, Lack of Standardization, and Variable Field Performance Are Hindering the Widespread Adoption of Biofertilizers

Despite their environmental and agronomic advantages, biofertilizers face several key restraints that challenge their large-scale adoption. One of the most persistent issues is the limited awareness among farmers—particularly small and marginal growers—regarding the correct application methods, benefits, and compatibility of biofertilizers with existing farming practices. This knowledge gap often leads to skepticism or misuse, resulting in inconsistent outcomes. Additionally, the lack of standardized regulations and quality control across manufacturers has led to market flooding with subpar or ineffective products, damaging farmer trust. Biofertilizers also face challenges in achieving uniform results due to varying soil conditions, microbial survival rates, and climate influences, which can affect their performance compared to chemical fertilizers.

Biofertilizers Market Opportunities:

The biofertilizers market is poised for significant growth as opportunities emerge through the global expansion of organic farming, increasing investment in agricultural biotechnology, and the untapped potential in emerging economies. As consumers drive demand for residue-free and sustainably produced food, more farmers are transitioning to organic cultivation, creating a natural demand surge for microbial-based fertilizers. In parallel, advancements in microbial genomics and fermentation technology are leading to the development of more efficient, crop-specific, and climate-resilient biofertilizer products. This innovation is not only improving performance but also attracting interest from agri-tech startups and multinational agri-input companies. Additionally, large tracts of underutilized farmland in Africa, Southeast Asia, and Latin America offer fertile ground for biofertilizer adoption, especially as governments and NGOs promote environmentally friendly agricultural practices.

Biofertilizers Market Segmentation:

Market Segmentation: By Product:

• Nitrogen Fixing

• Phosphate Solubilizing

• Other Products

In the biofertilizers market, nitrogen-fixing biofertilizers hold the dominant share due to their widespread use in enhancing the nitrogen content of soil, which is essential for plant growth. These biofertilizers contain beneficial microorganisms such as Rhizobium, Azotobacter, and Azospirillum, which convert atmospheric nitrogen into forms usable by crops. They are particularly effective in leguminous crops like soybeans, pulses, and peas, but are also being increasingly applied to cereals, vegetables, and oilseeds. As nitrogen is one of the most crucial macronutrients for plants, the ability of these biofertilizers to reduce dependency on synthetic urea-based fertilizers makes them highly attractive to both small and commercial farmers.

On the other hand, phosphate-solubilizing biofertilizers are emerging as the fastest-growing segment, driven by their role in making insoluble phosphates available to plants. These biofertilizers include microbial strains like Pseudomonas and Bacillus that release organic acids to dissolve bound forms of phosphorus in the soil. With phosphorus being vital for root development and flowering, and with natural phosphorus resources becoming increasingly scarce, these biofertilizers are gaining traction, especially in regions with phosphorus-deficient soils. Their growing use in horticultural crops, vegetables, and high-value fruits, combined with increasing awareness of their benefits, is fueling rapid adoption.

Market Segmentation: By Application:

• Seed Treatment

• Soil Treatment

In the biofertilizers market, seed treatment stands as the dominant application segment, primarily because of its ease of use, lower application costs, and direct impact on early plant development. Applying biofertilizers to seeds before sowing ensures that beneficial microorganisms are present from the very beginning of the plant’s lifecycle, enhancing root colonization, boosting germination rates, and improving resistance to early-stage stress. This method is particularly popular among farmers growing pulses, cereals, oilseeds, and legumes, as it allows for more uniform distribution of microbes and requires significantly less product compared to soil-based application. Moreover, seed treatment minimizes wastage, enhances efficiency, and is well-suited to both smallholder and large-scale farming operations, making it a practical and widely adopted practice globally.

Meanwhile, soil treatment is emerging as a fast-growing segment, driven by the increasing recognition of soil health as a cornerstone of sustainable agriculture. Biofertilizers applied directly to the soil help restore microbial balance, increase nutrient availability, and improve soil structure over time. This method is particularly useful in fields with depleted microbial activity or where long-term soil fertility is a key concern. While it may require a higher volume of application compared to seed treatment, soil treatment is gaining momentum in organic farming systems, horticulture, and commercial crop production, especially in areas where nutrient loss and chemical degradation are pressing issues. As awareness of soil regeneration and long-term productivity rises, soil treatment is expected to gain significant ground in the coming years.

Market Segmentation: By Crop Type:

• Cereals & Grains

• Oilseeds & Pulses

• Fruits & Vegetables

• Other Crop Types

In the biofertilizers market, cereals and grains represent the dominant crop type segment due to the large-scale cultivation and global demand for staple crops like wheat, rice, and maize. These crops form the foundation of food security in most regions and require substantial nutrient support, particularly nitrogen, to achieve high yields. Biofertilizers such as nitrogen-fixing microbes are extensively used in cereal farming to reduce dependency on synthetic fertilizers while maintaining productivity. Government policies encouraging sustainable practices in cereal production, combined with rising consumer need for organically grown staples, have contributed significantly to the adoption of biofertilizers in this segment. Additionally, large-scale commercial farms and export-oriented producers are increasingly integrating biofertilizers into their nutrient management programs to improve soil health, enhance crop quality, and meet regulatory standards for sustainable agriculture.

Fruits and vegetables are emerging as the fastest-growing segment in the biofertilizers market, fueled by their high economic value, shorter cultivation cycles, and the rising global preference for fresh, chemical-free produce. Farmers growing horticultural crops are adopting biofertilizers not only to meet organic certification requirements but also to improve crop color, taste, and shelf life—factors that directly influence marketability. Phosphate-solubilizing and potassium-mobilizing biofertilizers are commonly used to enhance flowering and fruiting stages, while plant growth-promoting rhizobacteria (PGPR) help improve nutrient uptake and stress resistance. The shift in consumer diets toward more plant-based and health-conscious options is boosting demand for organically grown fruits and vegetables, especially in urban markets.

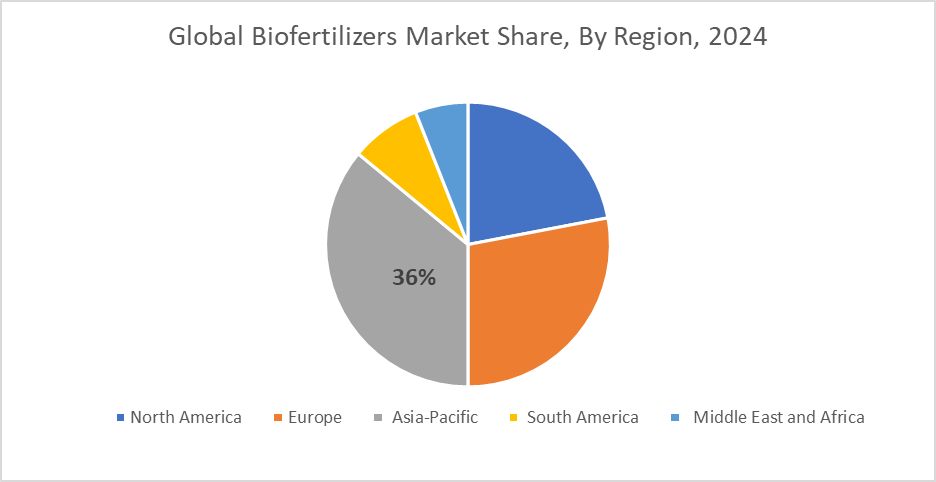

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

In the biofertilizers market, Asia-Pacific holds the dominant position with a 36% share, owing to its vast agricultural base, supportive government policies, and increasing awareness of sustainable farming practices. Countries like India and China are leading the charge, driven by strong government-led initiatives promoting organic farming, rising demand for residue-free food, and large populations engaged in agriculture. India, in particular, has launched national programs and subsidy schemes encouraging farmers to switch from chemical inputs to bio-based alternatives. Additionally, a growing network of local biofertilizer manufacturers, research institutions, and agri-tech startups is boosting product accessibility and farmer adoption.

Europe is emerging as the fastest-growing region in the global biofertilizers market, driven by stringent environmental regulations, robust support for organic agriculture, and rising consumer preference for sustainably produced food. The European Union has been actively promoting reduced chemical usage under its Common Agricultural Policy (CAP) and Green Deal, encouraging member states to adopt bio-based farming inputs. Countries like Germany, France, Italy, and Spain are rapidly expanding organic farmland, with biofertilizers becoming a central component in achieving climate and soil health goals. With ongoing investments in research and innovation, and policy alignment toward carbon-neutral agriculture, Europe is seeing a swift and steady increase in biofertilizer adoption across both small farms and commercial agri-enterprises.

COVID-19 Impact Analysis on the Global Biofertilizers Market:

The COVID-19 pandemic had a mixed impact on the global biofertilizers market. While supply chain disruptions and labor shortages temporarily affected production and distribution, the crisis also highlighted the need for resilient and sustainable agricultural systems. As concerns over food security and health grew, there was a noticeable shift toward organic farming and natural inputs, leading to increased interest in biofertilizers. Farmers began seeking cost-effective and eco-friendly alternatives to synthetic products, especially as global trade slowed and chemical fertilizer prices fluctuated. This shift in mindset ultimately strengthened the market’s long-term outlook, positioning biofertilizers as a vital component of post-pandemic agricultural recovery.

Latest Trends/ Developments:

One of the latest trends in the biofertilizers market is the growing focus on customized, crop-specific microbial formulations that address the unique nutrient needs of different plant types and soil conditions. Manufacturers are increasingly developing targeted solutions tailored for specific crops such as rice, wheat, soybeans, fruits, and vegetables to improve nutrient absorption and yield outcomes. These precision biofertilizers are formulated using advanced microbial strains that perform consistently across varied climates and soil textures, helping farmers reduce waste and optimize input usage. Additionally, there's a clear shift from traditional carrier-based products to liquid and encapsulated biofertilizers, which offer better shelf life, ease of application, and enhanced microbial survival during storage and transport.

Another major development is the integration of biofertilizers into smart and digital farming systems, where they are used alongside sensors, drones, and mobile-based platforms to monitor soil health and guide nutrient application in real time. This tech-driven approach allows farmers to make data-backed decisions, increasing the precision and efficiency of biofertilizer usage. Moreover, innovations in fermentation and biotechnology are enabling large-scale production of high-quality biofertilizers at competitive costs, supporting their commercial viability. As awareness around regenerative agriculture grows, industry players are also exploring blends that combine biofertilizers with biopesticides and organic soil conditioners, offering farmers a complete biological input solution that aligns with both productivity and sustainability goals.

Key Players:

• Novozymes (Denmark)

• UPL (India)

• Chr. Hansen Holding A/S (Denmark)

• Syngenta (Switzerland)

• T. Stanes and Company Limited (India)

• Lallemand Inc. (Canada)

• Rhizobacteria Argentina S.A. (Argentina)

• Vegalab SA (Switzerland)

• IPL Biologicals Limited (India)

• Kiwa Bio-Tech, product group cooperation (China)

Chapter 1. Global Biofertilizers Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Biofertilizers Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Biofertilizers Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Biofertilizers Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Biofertilizers Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Biofertilizers Market – By Product

6.1. Introduction/Key Findings

6.2. Nitrogen Fixing

6.3. Phosphate Solubilizing

6.4. Other Products

6.5. Y-O-Y Growth trend Analysis By Product

6.6. Absolute $ Opportunity Analysis By Product, 2025-2030

Chapter 7. Global Biofertilizers Market – By Application

7.1. Introduction/Key Findings

7.2. Seed Treatment

7.3. Soil Treatment

7.4. Y-O-Y Growth trend Analysis By Application

7.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Biofertilizers Market – By Crop Type

8.1. Introduction/Key Findings

8.2. Cereals & Grains

8.3. Oilseeds & Pulses

8.4. Fruits & Vegetables

8.5. Other Crop Types

8.6. Y-O-Y Growth trend Analysis By Crop Type

8.7. Absolute $ Opportunity Analysis By Crop Type, 2025-2030

Chapter 9. Global Biofertilizers Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Product

9.1.3. By Application

9.1.4. By Crop Type

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Product

9.2.3. By Application

9.2.4. By Crop Type

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Product

9.3.3. By Application

9.3.4. By Crop Type

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Product

9.4.3. By Application

9.4.4. By Crop Type

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Product

9.5.3. By Application

9.5.4. By Crop Type

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Biofertilizers Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Novozymes (Denmark)

10.2. UPL (India)

10.3. Chr. Hansen Holding A/S (Denmark)

10.4. Syngenta (Switzerland)

10.5. T. Stanes and Company Limited (India)

10.6. Lallemand Inc. (Canada)

10.7. Rhizobacteria Argentina S.A. (Argentina)

10.8. Vegalab SA (Switzerland)

10.9. IPL Biologicals Limited (India)

10.10. Kiwa Bio-Tech, product group cooperation (China)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Biofertilizers Market was valued at USD 2.53 billion in 2024 and is projected to reach a market size of USD 6.11 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 19.3%.

Rising demand for organic farming, soil health, and eco-friendly inputs.

Based on Application, the Global Biofertilizers Market is segmented into Seed Treatment and soil Treatment.

Asia-Pacific is the most dominant region for the Global Biofertilizers Market.

Novozymes (Denmark), UPL (India), Chr. Hansen Holding A/S (Denmark) are the leading players in the Global Biofertilizers Market.