Global Binary Cycle Power Plant Market Research Report – Segmentation By Technology (Organic Rankine, Kalina), By Application (Electricity Generation, Direct-Use Heating), By Project Size (Small Scale, Large Scale), By End-Use Industry (Industrial, Residential, Commercial), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-16142

Format:

Region: Global

Market Size and Overview:

The Global Binary Cycle Power Plant Market was valued at USD 63 billion in 2024 and is projected to reach a market size of USD 96.35 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 8.86%.

By employing a second working fluid, such as isobutane or ammonia, that vaporizes at lower temperatures to power turbines, binary cycle systems let moderate-temperature geothermal sources (under 180 °C) generate electricity. Expanding geothermal viability, this technology lowers water consumption and surface footprint relative to flash facilities, so it is being used for both distributed industrial heating and central networks.

Key Market Insights:

Favored for their simplicity and modularity, ORC systems hold around 58% of the technology market share as manufacturers standardize skid-mounted units, which shorten project schedules.

Representing great demand for renewable baseload capacity in areas such as North America and Europe, power-generation projects account for nearly 72% of the market value.

Economies of scale account for roughly 65% of installed capacity in projects above 10 MW; nonetheless, the fastest-growing sector is small-scale (< 5 MW).

Driven by energy‑intensive industries looking for carbon reduction, industrial uses such as district heating and process steam make up around 40%.

Binary Cycle Power Plant Market Drivers:

The recent expansion of low-temperature Geothermal resources is a major market growth driver.

Previously, just high‑enthalpy fields (> 180 °C) powered flash plants economically, but recent improvements in binary‑cycle design now allow for effective use of 80–95 °C resources using optimized working fluids like R123 and n‑Pentane. Using thermo‑economic optimization techniques, case studies in Indonesia, New Zealand, and Italy show that these moderate-temperature reservoirs, formerly considered unproductive, can support ORC installations with payback times less than 7 years. With twenty-five new binary plants commissioned throughout countries, including Southeast Asia, Southern Europe, and Central America in 2024 alone, the whole binary capacity increased by 12% year over year. This resource expansion greatly expands the worldwide project pipeline by opening geothermal possibilities in areas without high-temperature aquifers.

The recent mandates by the government related to renewable energy are considered a major factor for market growth.

Binary cycle economics has been based on strong policy drivers in the main markets. While France's accelerated depreciation schedules let developers write off 60% of installed costs in year one, essentially lowering the LCOE of binary facilities to USD 0.08–0.12 per kWh, the Investment Tax Credit (ITC) for geothermal in the U. S. set at 10% for projects beginning in 2025 lowers preliminary capital hurdles. This makes them highly competitive with onshore wind (USD 0.033 per kWh) and solar PV (USD 0.049 per kWh). Meanwhile, European Renewable Energy Directive objectives and China's renewable‑portfolio standards require ≥ 20% geothermal quotas in some provinces, forcing utilities to include binary installations into their renewable mixes and so guarantee long‑term off‑take contracts.

The emergence of industrial heat integration processes acts as an important market growth driver.

Beyond electricity generation, binary cycle facilities are very good at cogenerating process heat for energy‑intensive businesses. Dry-steam turbines feeding ORC plants at New Zealand's Kawerau installation also provide 7 bar steam for paper-mill disinfection and wood drying, therefore lowering fuel expenditures by 20% and net CO₂ emissions by 15% for the integrated facility. Like configurations in Iceland's HS Orka and the Hellisheiði site co‑produce district heating and greenhouse heat, demonstrating that coupling binary electricity output with direct‑use thermal loops can improve overall plant efficiency from 12% (electric only) to 65% (total energy utilization).

The recent improvements seen in the field of technology and the emergence of modularization are said to be major market drivers.

The change to skid‑mounted ORC modules built in factories has simplified installation and lowered financial risk. Pre‑tested units from companies like Turboden and Exergy now provide a 30% reduction in on‑site erection time and a 15% cut in capex relative to custom construction. These modular systems, ranging from 250 kW micro‑plants to 20 MW arrays, allow developers to undertake distributed energy projects in distant locations with little civil work. Moreover, integrating digital‑twin simulations and AI‑driven performance analytics helps operators to forecast maintenance demands and maximize operational parameters in real time, hence supporting 98% availability numbers and stretching component life cycles by up to 20%.

Binary Cycle Power Plant Market Restraints and Challenges:

The high levels of capital expenditure are a huge challenge faced by the market, as it decreases its adoption rate.

Even with modern cost reductions, binary cycle power plants demand substantial upfront investment, averaging USD3,963 per kW for a 50-kW ORC unit. When scaled to utility sizes (10–20MW), total capex can range from USD 20 million to USD 60 million, depending on site‐specific civil works and fluid‐handling equipment. Financing these capital requirements often calls for long‐term power‐purchase agreements (PPAs) with investment‐grade offtakers, pushing smaller developers, who lack balance‐sheet strength, toward joint ventures or public‐sector partnerships. Even with modular ORC skids lowering installation costs by 15%, the remaining capital intensity remains a barrier, particularly in emerging markets where low-cost lending is scarce.

The high risk related to the exploration of resources hinders the growth potential of the market.

With single well expenses formerly ranging from USD 9.4 million to USD 4.8 million following recent Fervo Energy developments that reduced drill times by 70% and halved per‐well costs to USD 4.8 million, drilling and reservoir characterization make up to 75% of total costs for binary cycle plants. Despite these advancements, the success of a binary cycle project depends on verifying appropriate flow rates and temperatures before approving plant building. Unproductive exploratory wells or underperforming reservoirs can delay projects by more than a year and cause substantial cost overruns; research reveals that a mis‐sited well can raise P50 project expenditures by 30% and endanger debt coverage ratios if augmentation is necessary.

The problem of limited infrastructure for the grid poses a major challenge for the market.

In remote areas lacking transmission networks, such as the volcanic areas of Central America or the Rift Valley of East Africa, many high-temperature geothermal resources ideal for binary cycle development are found. In regions needing line extensions, substation upgrades, and long‐distance distribution, the Greenfield ESG analysis observes that the delivered cost of electricity might rise by USD 0.05 to USD 0.15 per kWh. For community‐scale projects (< 5 MW), microgrid or local distribution solutions can reduce these costs, but bigger developers often need to invest USD 3 million to USD 10 million in dedicated transmission infrastructure, further pinching project economics and prolonging payback periods.

The market faces a challenge from the permitting delays that happen due to the complex regulatory framework.

Binary cycle projects must negotiate multi‐tiered regulatory systems, environmental impact assessments, water-use licenses, seismic stability evaluations, and land-access agreements that might extend development timelines by 12 to 24 months. Even with recent permit‐streamlining measures under the U. S. Energy Act of 2020, the NREL Annual Technology Baseline notes that typical geothermal permitting in the U. S. still spans 18 to 36 months from initial investigation to plant commissioning. In geologically sensitive or protected areas, such as Iceland's national parks or Europe's Natura 2000 zones, additional biodiversity and cultural heritage reviews can impose further delays and mitigation requirements, inflating both pre‐construction costs and the risk profile for equity and debt investors.

Binary Cycle Power Plant Market Opportunities:

The recent retrofits of decommissioned oil and gas wells present a great opportunity for the market, as they will reduce the drilling risk by a good margin.

Repurposing mature or suspended hydrocarbon wells for binary‑cycle geothermal provides a strong means of reducing drilling risk and capex by as much as 40% since existing wellbores, surface installations, and subsurface rights can be employed instead of newly drilled ones. A Stanford-led techno-economic analysis revealed that finding "suspended" wells, those temporarily idle but still structurally sound, can save over USD 50,000 per well in retrofit expenses compared to wholly abandoned locations, therefore speeding well-depth and gradient analysis for site assessment. These changes are being tested by major oil-field operators and service companies right now. Fervo Energy in Nevada has successfully retrofitted a legacy oil well using horizontal drilling and closed-loop stimulation, producing 8 MWe of clean energy and demonstrating the O&G playbook's relevance to geothermal. This chance might unlock thousands of low-risk binary projects all around, therefore offering a quick scaling-up mechanism for renewable baseload generation as the worldwide inventory of oil wells surpasses 20 million.

The emergence of floating binary cycle platforms has given rise to the blue economy, which is a good market opportunity.

Emerging “blue‑economy” boundary, offshore binary plants on floating platforms utilize seabed thermal gradients and undersea volcanic seeps to create energy with the smallest coastal imprint. Conceptual studies by marine-engineering companies describe ideas whereby floating ORC modules are moored above submarine hydrothermal sources, sending heat through insulated riser pipes to surface heat exchangers and binary turbines. By utilizing floating production storage and offloading (FPSO) ships and subsea pipelines, these platforms may piggyback on already established oil and gas infrastructure, thereby lowering fresh construction demands. Early viability phases for pilot projects off Iceland and in the Caribbean seek to produce 5–10 MWe per unit, with projected LCOEs of USD 0.12–0.15 per kWh, competitive with offshore wind. Floating geothermal might become a key element of integrated coastal energy complexes as maritime jurisdictions search for renewable diversification and carbon‑neutral shipping fuels.

The growing popularity of Hybrid Solar-Geothermal projects is a major market development opportunity.

Hybrid constructions, including a 50 MW CSP tower with a 25 MW ORC facility, have confirmed round-the-clock generation profiles and lowered solar-PPA premiums as solar-thermal and geothermal developers seek co-location. When paired with thermal energy storage, hybrid plants offer a route to 24/7 renewables without depending only on batteries or grid backup. Economic simulations for dry-cooled CSP-binary hybrids in arid locations show LCOEs dropping to USD 0.07–0.09 per kWh compared to USD 0.11 per kWh for isolated geothermal. By 10 to 20 °C, hybrid designs enhance cycle-inlet temperatures and increase instantaneous power output by up to 30%. Combining concentrated solar power (CSP) with binary geothermal plants smooths output variation and raises capacity factors above 85%, hence producing dispatchable renewable baseload.

The developing nations show great potential for the growth of the market as they are considered to be emerging markets.

Substantial unused binary‑cycle capacity is present in Africa and Latin America, where geological and policy circumstances are converging to propel pilot initiatives toward commercial level. Enel's Cerro Pabellón plant, which houses 10% of the world's active volcanoes, has confirmed high‑altitude binary activities at 4,500 m above sea level, therefore promoting fresh 100 MW pipeline projects in the northern arc. Kenya, on the other hand, is investigating more binary modules to tap lower‑temperature reservoirs, targeting an extra 200 MW by 2030 alongside EU‑backed rural‑electrification projects, with 892 MW of installed geothermal capacity mostly at Olkaria. Government incentives like tax breaks and subsidized drilling in Peru and Ethiopia are starting to unlock feasibility studies for 5–20 MW community‑scale binary facilities. By 2030, these developing markets could add 400 to 600 MW of fresh binary capacity as project pipelines develop, so diversifying the renewables mix of global geothermal and supporting local skills development.

Binary Cycle Power Plant Market Segmentation:

Market Segmentation: By Technology

• Organic Rankine

• Kalina

The Organic Rankine segment is the dominant one in the market. With their established dependability, high maturity, and capacity to use a wide variety of medium-temperature geothermal and waste-heat sources, organic Rankine cycle (ORC) systems account for around 58% of the technology mix. The Kalina segment is considered to be the fastest-growing segment. With a CAGR of roughly 9%, Kalina Cycle technology is projected to expand more rapidly because of its higher theoretical thermal efficiency (10–15% gains over ORC) when run over varied temperature gradients.

Market Segmentation: By Application

• Electricity Generation

• Direct-Use Heating

The Electricity Generation segment is said to dominate this market with a high market share. As grid‑tied baseload capacity continues to be the main value driver for utilities and IPPs, more than 72% of binary cycle installations are aimed at generating electricity. The Direct-Use Heating segment is the fastest-growing segment of the market. At about 15% CAGR, direct-use heating applications, district heating, greenhouse warming, and process heat are growing thanks to high fuel-cost savings and industrial decarbonization rules.

Market Segmentation: By Project Size

• Small Scale

• Large Scale

The Large-Scale segment is said to dominate this market, and the Small-Scale segment is considered the fastest-growing segment. Economies of scale in drilling, turbine dimensioning, and heat-exchanger production account for around 65% of installed capacity in plants above 10 MW. The Small-Scale segment is the fastest-growing category with an 18% CAGR due to small-scale modular units (< 5 MW) that are factory-assembled ORC skids, which make finance easier and speed up installation in isolated or off-grid areas.

Market Segmentation: By End-Use Industry

• Industrial

• Residential

• Commercial

The Industrial segment dominates this market with a market share of around 40%. This is due to its increasing use in fields like food processing, mining, and pulp & paper industries. The Residential segment is said to be the fastest-growing segment of the market. At roughly 14% CAGR, residential and communal microgrid applications, providing combined heat and electricity for regional networks, are expanding as modular solutions reduce access barriers. For energy resilience, commercial structures like hotels, hospitals use binary cogeneration; utilities buy wholesale power; and remote telecom sites employ micro‑plants for off‑grid dependability.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

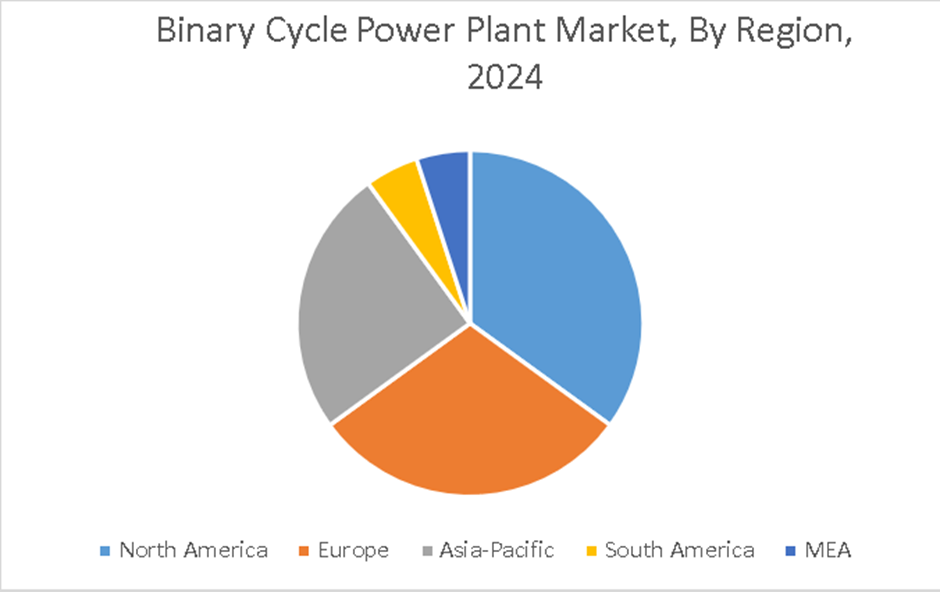

North America is the leader of the market. Backed by abundant geothermal resources, beneficial tax incentives (U. S. ITC), and robust utility off‑take programs, North America drives with around 35% of the world market value. The Asia-Pacific region is said to be the fastest-growing one for this market. Driven by Indonesia, the Philippines, and China meeting renewable objectives and extending rural electrification using modular binary plants, APAC is the fastest-growing area with roughly 25% CAGR.

The European market is defined by strong growth, which is driven by growing regulatory support for renewable energy, ambitious climate targets, and investments in geothermal energy technologies, especially in nations like Germany, Italy, and Iceland. Supported by growing investments and technical developments. Both South America and the MEA regions are considered emerging markets. Rising markets with growth potential as nations investigate geothermal energy as a feasible renewable source. Despite a lower market size, there is rising interest in binary cycle power stations as part of wider attempts to diversify energy sources and improve regional energy security.

COVID-19 Impact Analysis on the Global Binary Cycle Power Plant Market:

Due to lockdowns and labor limitations, the COVID‑19 pandemic upset the market for binary cycle power plants by delaying exploration, drilling, and equipment supply lines. For example, as movement limitations stopped or reduced fieldwork and well stimulation, Indonesia's geothermal goals had their commissioning dates postponed from 2020 into 2021. Though financing was obtained before the epidemic, six-month setbacks in reservoir injection testing for the United Downs project in the UK delayed performance‑qualification stages into mid‑2021. While COVID-era stimulus measures in the U. S. and EU thereafter rejuvenated funding for green projects, counteracting early setbacks and quickening modular binary deployments from 2022 onward, these delays temporarily limited capacity additions, and project completions slipped by an average of 9 months worldwide.

Latest Trends/ Developments:

Geothermal operators are using digital twin systems combining real-time production data with reservoir and surface-plant models to allow AI-powered predictive maintenance and performance tuning, increasing uptime beyond 98%.

Developers are switching from R245fa to low‑global‑warming‑potential refrigerants, including HFO‑1233zd and R1234ze, that cut lifetime GWP by more than 90% while preserving similar cycle efficiencies to satisfy environmental rules.

Utah's FORGE project, attempting for commercial-scale demonstration by 2030, is one example of how next-generation binary plants are increasingly combining with EGS technologies, fracturing hot dry rock to access deeper, higher-temperature resources.

Pilot projects are investigating blockchain systems for peer-to-peer trading of binary-plant power in local microgrids, thereby enhancing transaction transparency and enabling dynamic pricing for supplementary services in distributed energy networks.

Key Players:

• Ormat Technologies Inc.

• Enel Green Power S.p. A.

• Mitsubishi Heavy Industries Limited

• Exergy International Srl

• Turboden

• NEM S.p.A.

• Calpin Corp

• Fuji Electric Co. Ltd.

• Bosch Thermotechnology

• Siemens AG

Chapter 1. Global Binary Cycle Power Plant Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Binary Cycle Power Plant Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Binary Cycle Power Plant Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Binary Cycle Power Plant Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Binary Cycle Power Plant Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Binary Cycle Power Plant Market - By Technology

6.1. Introduction/Key Findings

6.2. Organic Rankine

6.3. Kalina

6.4. Y-O-Y Growth trend Analysis By Technology

6.5. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 7. Global Binary Cycle Power Plant Market – By Application

7.1 Introduction/Key Findings

7.2. Electricity Generation

7.3. Direct-Use Heating

7.4. Y-O-Y Growth trend Analysis By Application

7.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Binary Cycle Power Plant Market – By Project Size

8.1. Introduction/Key Findings

8.2. Small Scale

8.3. Large Scale

8.4. Y-O-Y Growth trend Analysis By Project Size

8.5. Absolute $ Opportunity Analysis By Project Size, 2025-2030

Chapter 9. Global Binary Cycle Power Plant Market – By End-Use Industry

9.1. Introduction/Key Findings

9.2. Industrial

9.3. Residential

9.4. Commercial

9.5. Y-O-Y Growth trend Analysis By End-Use Industry

9.6. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 10. Global Binary Cycle Power Plant Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Technology

10.1.3. By Application

10.1.4. By Project Size

10.1.5. By End-Use Industry

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Technology

10.2.3. By Application

10.2.4. By Project Size

10.2.5. By End-Use Industry

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Technology

10.3.3. By Application

10.3.4. By Project Size

10.3.5. By End-Use Industry

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Technology

10.4.3. By Application

10.4.4. By Project Size

10.4.5. By End-Use Industry

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Technology

10.5.3. By Application

10.5.4. By Project Size

10.5.5. By End-Use Industry

10.5.6. By Region

Chapter 11. Global Binary Cycle Power Plant Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Ormat Technologies Inc.

11.2. Enel Green Power S.p. A.

11.3. Mitsubishi Heavy Industries Limited

11.4. Exergy International Srl

11.5. Turboden

11.6. NEM S.p.A.

11.7. Calpin Corp

11.8. Fuji Electric Co. Ltd.

11.9. Bosch Thermotechnology

11.10. Siemens AG

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Binary Cycle Power Plant Market was valued at USD 63 billion and is projected to reach a market size of USD 96.35 billion by the end of 2030 with a CAGR of 8.86%.

Capturing around 58%, Organic Rankine Cycle systems provide modular, skid‑mounted designs, easy operation, and strong performance throughout various temperature ranges.

Governmental emphasis on renewable energy in Indonesia, Philippines, and China's rural electrification initiatives is helping Asia-Pacific to be the fastest-growing region (approx. 11% CAGR).

Up to a year, pandemic disturbances stalled drilling and supply chains, but green‑recovery financing since 2022 has revived investment and modular plant deployments.

Digital twins combined with artificial intelligence predict maintenance requirements and maximize operations in real time, thereby increasing uptime beyond 98 percent. Low-GWP refrigerants like HFO-1233zd reduce lifetime global-warming potential by over 90%. Enhanced geothermal systems extend resource temperatures via engineered reservoirs, while blockchain pilots enable transparent, peer-to-peer energy trading in local microgrids.