Global Battery Materials Market Research Report – Segmentation By Battery Type (Lithium-ion Batteries, Solid-state Batteries, Nickel-metal Hydride Batteries); By Material Type (Cathode Materials, Anode Materials, Electrolytes); By Application (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial & Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-5764

Format:

Region: Global

Market Size and Overview:

The Battery Materials Market was valued at USD 59.45 billion in 2024 and is projected to reach a market size of USD 84.99 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 7.41%.

The battery materials market forms the backbone of the electrification and renewable energy storage shifts globally. The growing demand for electric cars, personal electronics, and large-scale energy storage systems has increased the need for advanced, high-performance materials, such as lithium, nickel, cobalt, and graphite, as well as the newer solid-state alternatives. The performance of a battery relies significantly on these materials, as they are used in increasing battery efficiency, safety, service life, and energy density. The growing environmental concerns and stringent regulations are further fueling the investments into sustainable, recycled-grade battery materials, pushing manufacturers for a fast pace in innovations. Since nations and industries started pledging to net-zero goals, the battery materials market has become a critical enabler of the clean energy transition as of today, which makes it a pillar of the future global economy.

Key Market Insights:

High-nickel cathode chemistries, such as NMC 811, now account for over 25% of EV battery production. These materials improve energy density and reduce reliance on cobalt, aligning with automakers' goals for longer range and lower costs.

Graphite, both natural and synthetic, holds about 95% of the anode material market share today. As demand for higher-capacity batteries grows, producers are exploring advanced alternatives like silicon and graphene composites to further enhance performance.

Battery Materials Market Drivers:

The explosive growth in electric vehicle adoption is one of the most powerful forces driving the battery materials market.

The adoption of electric vehicles has exploded and has become one of the major driving forces in the battery materials market. Automakers worldwide are investing billions in electrifying their fleets, with the goal of ending internal combustion engine vehicle sales by the end of the following decade. For instance, global EV sales climbed over 10 million units in 2023 alone and are projected to triple by 2030. This has a direct positive impact on the fueling requirements of the key battery materials: lithium, nickel, cobalt, and graphite, which are used to manufacture high-energy-density batteries. As consumers become more demanding on range performance and charge times, they will drive automakers into more aggressive configurations as nickel-rich NMC and solid-state batteries. Such chemistries will invariably increase the need for special materials. Finally, government initiatives, along with ever-stricter emission limits and growing charging infrastructures, also put lower barriers on the path to mainstream acceptance by many buyers and thus add market momentum.

Another significant driver of the battery materials market is the rapid global shift toward renewable energy generation and storage.

First, renewable power generation and storage have become the other major force driving the battery materials market. The need for effective and large-scale energy storage systems to stabilize grid power and provide a reliable supply during dips is greatly required as wind and solar installations ramp up. The deployment of battery storage, particularly at the utility scale, globally would surpass 500 GWh by 2030, and hence, massive amounts of advanced materials are needed. These systems rely on various technologies such as lithium-ion batteries and next-generation solid-state batteries, both of which require vast quantities of lithium, nickel, and manganese to provide high capacity and long cycle life. Battery material demand has also been supported by the billions being invested by governments and private investors into renewable integration projects to achieve carbon neutrality targets. Additionally, decentralized energy systems and home energy storage solutions are gaining more acceptance among the masses, creating further demand for battery materials on residential and community levels. The world is moving toward cleaner energy options while giving tremendous long-term growth opportunities to the battery materials industry as battery cost decreases, increasing the attractiveness of renewable storage systems and their uptake.

Battery Materials Market Restraints and Challenges:

One of the most critical challenges facing the battery materials market is the vulnerability of global supply chains and the scarcity of key raw materials.

The fragility of supply chains and the scarcity of raw materials represent two of the scariest problems in battery materials. Important elements like lithium, cobalt, and nickel are concentrated in specific regions and countries, like the Democratic Republic of the Congo produces over 70% of cobalt in the world. The reasons for this concentration are that when supply sources are very limited, makers become dependent on other nations as sources. To that extent, they can suffer from geopolitical and trade risks or disruptions due to the instability prevailing in the locality. Furthermore, the exponential growth in demand for electric vehicles alongside storage systems caused their exceeding current mining and refining capacities, leading to shortages of materials and volatile price swings. Complicating these conditions have been global events, such as the COVID-19 pandemic or regional conflict, which have highlighted how fragile these supply chains can easily become. As the rush for long-term contracts and investments in localized supply continues, these challenges present real hurdles to meeting the ever-growing global demand for advanced batteries. These will also require solving if the present and future are going to see stable, ethical, and sustainable development in the battery materials market.

Battery Materials Market Opportunities:

The battery materials market is a real treasure trove awaiting exploitation through advanced recycling processes, innovative materials development, and regional diversification of the supply chain. The battery materials recycling operation can minimize the use of new mining resources to a large extent, as modern processes can recover approximately 95% of critical metals like lithium, cobalt, and nickel. This reduces the environmental impact of mining, promotes more stable raw material costs, and supports the circular economy model. Innovations in new materials such as silicon anodes, solid-state electrolytes, and high-nickel cathodes hold the promise of delivering batteries with greater energy density, faster charging, and longer lifetimes, opening up new revenue streams for the suppliers of materials. Growing operations in non-traditional mining regions for local battery material production mitigate geopolitical risks and stimulate regional economies. Countries such as Australia, Canada, and various EU nations are fast-tracking lithium and nickel projects to build a more resilient supply chain. Strong supportive policies and tax incentives for green investments across the globe will continue to fuel the research and exploitation of next-generation sustainable materials. Thus, all these opportunities finally place the battery materials market as a strategic enabler for future clean energy systems and global electrification.

Battery Materials Market Segmentation:

Market Segmentation: By Battery Type

• Lithium-ion Batteries

• Solid-state Batteries

• Nickel-Metal Hydride Batteries

The global market for battery materials is segmented by battery technology types that include lithium-ion battery, solid-state battery, and nickel-metal hydride (NiMH) battery, all fulfilling different roles in the energy landscape. Traditionally, lithium-ion batteries are used in electric vehicles, consumer electronics, and energy storage systems, and, as the most popular battery type today, find equal encouragement for their properties of high energy density, long cycle life, and rapidly declining costs. New developments in lithium-ion chemistries and battery formulations, such as high-nickel and low-cobalt materials, continue to enhance their performance while concurrently mitigating supply chain vulnerabilities. Solid-state batteries are attracting considerable attention owing to their enhanced safety, higher energy density, and the promise of very fast charging, although still in early commercialization. Solid-state batteries eliminate the use of liquid electrolytes, which could leak, hence increasing thermal stability, a possible game changer for EVs of the future. Nickel-metal hydride batteries have been widely utilized in hybrid vehicles and certain industrial equipment because of their sturdy safety and moderate cost; however, they are slowly fudging their way into obsolescence next to lithium technologies. Nevertheless, their importance remains in niche applications, needing very high power outputs and durability.

Market Segmentation: By Material Type

• Cathode Material

• Anode Material

• Electrolytes

The battery materials market, according to the types of materials, includes cathode materials, anode materials, and electrolytes, which have their own roles in making the performance of a battery worthwhile and safe. The cathode materials, such as lithium nickel manganese cobalt oxide (NMC), lithium iron phosphate (LFP), and lithium cobalt oxide (LCO), decide the energy density, life span, and cost profile of a battery. In response to the growing demand for a better range and less dependence on cobalt, manufacturers are moving toward adopting nickel-rich cathode chemistries. Anode materials, which for now are exclusively graphite (natural and synthetic), meanwhile, have been designed with silicon-doped and graphene-enhanced versions to improve their capacities and speeds of charge speeds. Advances in anode technology are central to improving cycle life and reducing battery size without compromising performance. The electrolytes include liquid, gel, or solid-state, facilitating ion transport and having a direct impact on battery safety and temperature range under operation. The development of solid-state electrolytes calls for the transformation of safety standards in batteries and next-generation battery designs.

Market Segmentation: By Application

• Electric Vehicles

• Consumer Electronics

• Energy Storage Systems

• Industrial & Others

Electric vehicles, consumer electronics, energy storage systems, and industrial and other segments-the names of segments in which the market is segmented on application. Each section offers its special growth and raw material needs. Of these, the fast-emerging application segment is electric vehicles (EVs) propelled by mature decarbonization ambitions at the national level, government incentives, and accelerated technology developments. This eagerly pursued and awaited transition toward extended-range EVs has created high-performance battery materials designed for increasing energy density per unit weight. Compactness and dependability high energy density with safety metrics are still in demand from consumer electronics (mobile phones, laptops, and wearables). As the mobile device functionality expands, these advanced materials are necessary for improved charging speeds and longer running times. Energy Storage Systems (ESS) are quickly evolving business segments, based each application segment urges specific innovations in battery materials, linking the world supply chain and inspiring continuous materials science breakthroughs to meet evolving use cases that are increasingly diverse and demanding.

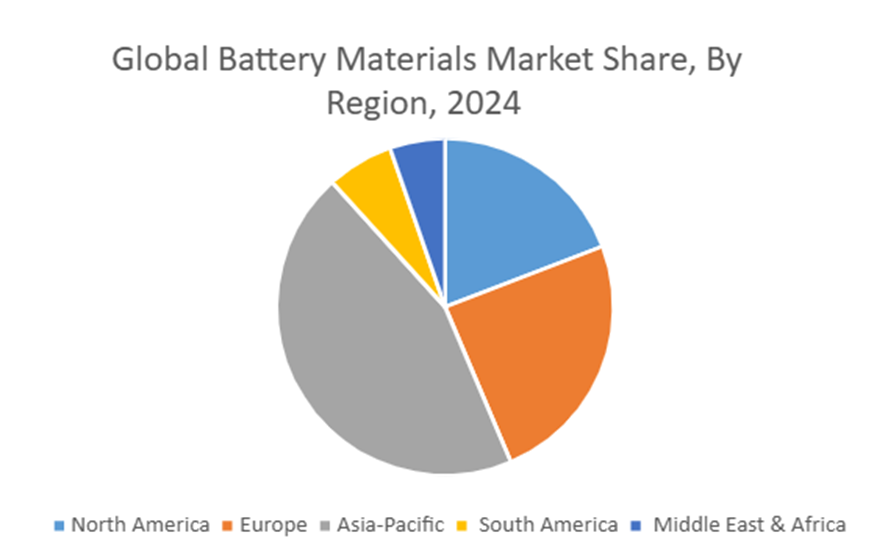

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

Asia-Pacific is leading the pack in terms of global battery materials owing to its capacities in electric vehicle manufacturing, solid base in electronics manufacturing, and mineral resources that China and Australia possess. Europe comes next, accelerated by aggressive EV mandates, rapid build-out of battery gigafactories, and ambitious circular economy initiatives focused on recycling and sustainability. The North American region is making strong progress with the support of solid policy incentives, increasing adoption of EVs, and great efforts towards localization of battery supply chains, preventing heavy reliance on imports. In South America, countries endowed with vast lithium resources, particularly Chile and Argentina, are working towards enhancing their export capabilities while attracting global investment to consolidate their standing in the battery value chain. In parallel, the Middle East and Africa position themselves as potential mining hubs in the advanced stages of cobalt and nickel production, particularly, formations are already being established in the Democratic Republic of the Congo and South Africa-coupled with early investment in battery production locally.

COVID-19 Impact Analysis on the Battery Materials Market:

The COVID-19 pandemic disrupted the materials manufacturing market for batteries from the start by disrupting raw materials supply chains, stopping mining activities, and delaying manufacturing. Lockdowns and transport restrictions led to a shortage of certain raw materials, including lithium, cobalt, and nickel, giving rise to price volatility and delays in production with battery manufacturers worldwide. Many projects were put on hold or delayed as the workforce availability dipped, and international logistics became erratic. However, during this time, heavy investments started pouring into the electric vehicle and renewable energy storage sectors, being promoted by governments in their green recovery plans to revive their pandemic-hit economies. This renewed interest accelerated the demand for advanced battery materials even faster than was predicted before the pandemic. In light of this, companies began to make diversification of supply chains and local sourcing a priority to avoid future risks, pushing projects for regional mining and refining.

Latest Trends/ Developments:

The landscape of battery materials is rapidly evolving with breakthroughs in next-generation chemistries and the scaling of more sustainable supply chains. Solid-state and sodium-ion batteries are gaining some real traction: for example, QuantumScape's new "Cobra" separator represents a critical production milestone for solid-state cells, whereas sodium-ion technology, particularly led by CATL, is targeting niche market adoption by 2027. Recycling vanguards like Redwood Materials are carving new circular-economy pathways to convert used EV batteries into grid storage systems for AI data centers. Lithium prices have tanked over 90%, with supply worries clouding this demand surge and becoming a spur for innovations in cheaper extraction technologies. On the international front, China is set to overtake Australia as the top lithium producer by 2026, while the U.S. is backing companies like Novonix in establishing domestic graphite supply chains free from China dependence.

Key Players:

• Umicore (Belgium)

• Asahi Kasei Corporation (Japan)

• Mitsubishi Chemical Holdings Corporation (Japan)

• POSCO Holdings Inc. (South Korea)

• Johnson Matthey (UK)

• BASF SE (Germany)

• Albemarle Corporation (US)

• LG Chem Ltd. (South Korea)

• Sumitomo Metal Mining Co., Ltd. (Japan)

• Contemporary Amperex Technology Co., Limited (China)

Chapter 1. Global Battery Materials Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Battery Materials Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Battery Materials Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Battery Materials Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Battery Materials Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Battery Materials Market – By Battery Type

6.1. Introduction/Key Findings

6.2. Lithium-ion Batteries

6.3. Solid-state Batteries

6.4. Nickel-metal Hydride Batteries

6.5. Y-O-Y Growth trend Analysis By Battery Type

6.6. Absolute $ Opportunity Analysis By Battery Type, 2025-2030

Chapter 7. Global Battery Materials Market – By Material Type

7.1. Introduction/Key Findings

7.2. Cathode Materials

7.3. Anode Materials

7.4. Electrolytes

7.5. Y-O-Y Growth trend Analysis By Material Type

7.6. Absolute $ Opportunity Analysis By Material Type, 2025-2030

Chapter 8. Global Battery Materials Market – By Application

8.1. Introduction/Key Findings

8.2. Electric Vehicles

8.3. Consumer Electronics

8.4. Energy Storage Systems

8.5. Industrial & Others

8.6. Y-O-Y Growth trend Analysis By Application

8.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 9. Global Battery Materials Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Battery Type

9.1.3. By Material Type

9.1.4. By Application

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Battery Type

9.2.3. By Material Type

9.2.4. By Application

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Battery Type

9.3.3. By Material Type

9.3.4. By Application

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Battery Type

9.4.3. By Material Type

9.4.4. By Application

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Battery Type

9.5.3. By Material Type

9.5.4. By Application

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Battery Materials Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Umicore

10.2. Asahi Kasei Corporation

10.3. Mitsubishi Chemical Holdings Corporation

10.4. POSCO Holdings Inc.

10.5. Johnson Matthey

10.6. BASF SE

10.7. Albemarle Corporation

10.8. LG Chem Ltd.

10.9. Sumitomo Metal Mining Co., Ltd.

10.10. Contemporary Amperex Technology Co., Limited

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Battery Materials Market was valued at USD 59.45 billion in 2024 and is projected to reach a market size of USD 84.99 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 7.41%.

Surging electric vehicle adoption and renewable energy storage needs are fueling rapid demand for advanced battery materials. Technological innovations in battery chemistries are driving the need for higher-performance, safer, and more sustainable materials.

The Battery Materials Market by application is segmented into Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial & Others. Each segment drives unique material demands, from high energy density for EVs to long cycle life for grid storage.

Asia-Pacific is the most dominant region for the Battery Materials Market.

Umicore, Asahi Kasei, Mitsubishi Chemical Holdings, Posco, and Johnson Matthey are the key players in the Battery Materials Market.