Global AI In Cybersecurity Market Research Report – Segmentation By Component (Software, Hardware, Services), By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Others), By Deployment Mode (Cloud, On-premises, Hybrid), By End-Use Industry (BFSI, Healthcare, IT & Telecom, Retail, Government & Defense, Energy & Utilities, Others), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-3225

Format:

Region: Global

Market Size and Overview:

The Global AI In Cybersecurity Market was valued at USD 31.48 billion and is projected to reach a market size of USD 93.75 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.4%.

Sophisticated cyberattack proliferation, ransomware, supply‑chain exploits, AI‑powered phishing, and the need for automated, real‑time threat detection and response drive this rapid expansion. Solutions based on artificial intelligence combine machine learning, natural-language processing, and behavioral analytics to supplement conventional security tools, simplify SOC operations, and reduce risks across network, endpoint, application, and cloud settings.

Key Market Insights:

The threat detection, which is based on Machine Learning, holds around 42% of the technology mix. This is due to its ability to analyze streams of telemetry and identification of zero-day anomalies.

Approximately 60% of market revenues come from AI-enhanced security software, namely UEBA, SOAR, and NGAV, since companies give ready-to-use solutions priority over hardware or expert services.

Offering quick scalability, centralized administration, and seamless integration with hybrid‑cloud systems, cloud‑native AI security solutions make up approximately 55% of deployments.

Driven by legal requirements and high-value cyber-threat exposures, banking, financial services, and insurance head vertical adoption with around 28% of spend.

AI In Cybersecurity Market Drivers:

The escalation in the sophistication of the threat is driving the demand for this market.

Recent research reveals that 76.4% of phishing efforts now utilize AI‑generated polymorphic content, designing ongoing changing emails and URLs that bypass signature‑based defenses, while ransomware payloads distributed via phishing have increased 22.6% in only six months. Real-time automated artificial intelligence scanners can investigate thousands of applications and network endpoints, detecting vulnerabilities and launching exploits without human involvement. With attackers synthesizing executive voicemails to persuade workers into sending money, deepfake‑powered voice and video phishing (“vishing”/“smishing”) provides another level of complexity. A warning has been given that by 2026, 70% of companies would experience at least one AI-driven attack, highlighting the great necessity for similarly AI-native defensive systems able to provide adaptive threat intelligence and autonomous incident response.

The need for the cloud and remote work security is driving the need for this market.

The mass shift to hybrid‑work models (65% of companies) and multi‑cloud infrastructures (75%) has erased conventional network perimeters, thereby exposing unmanaged endpoints and misconfigurations. AI‑driven Cloud Security Posture Management (CSPM) tools now automatically monitor IaC templates, container images, and cloud permissions to spot and correct misconfigurations. Microsoft Defender for Cloud reports a 40–50% decrease in cloud‑breach events when CSPM recommendations are promptly deployed. Similarly, Secure Access Service Edge (SASE) platforms enhanced with ML monitor user behavior across VPNs and Zero Trust networks, flagging anomalous access patterns that could indicate credential compromise. By automating compliance checks and dynamic policy enforcement across dispersed endpoints, these AI‐powered solutions have reduced misconfiguration‑related breaches by up to 50%, according to industry benchmarks.

The pressure from the regulations and compliance is considered a major market driver.

Global regulations, including GDPR (EU), CCPA (California), PCI DSS (payments), and HIPAA (healthcare), demand strict access control, encryption, and auditability of data. Traditional manual compliance processes are labor-intensive and error-prone; however, AI-driven Data Loss Prevention (DLP) and automated compliance reporting platforms streamline evidence collection and policy enforcement. After implementing AI-powered DLP solutions that classify data flows in real time and produce audit-ready logs, financial organizations report a 30% drop in manual compliance effort. AI models continuously adapt to new legal requirements, such as e‑privacy directives and growing digital assets frameworks, automatically generating stress‑test scenarios and risk‑report narratives, so reducing the risk of fines (up to 4% of global turnover under GDPR). For companies trying to remain audit-ready in changing legal environments, this real-time, policy-aware monitoring is vital.

The shortage faced in the number of cybersecurity talent is driving the need for this market.

Having 4 million unfilled cybersecurity jobs and only 74 certified applicants per 100 vacancies, a major worldwide skills gap has left Security Operation Centers (SOCs) overburdened and understaffed. By automating regular triage, threat hunting, and incident-playbook execution, Artificial Intelligence (AI)-driven Security Orchestration, Automation, and Response (SOAR) solutions help to close this gap by lowering mean time to detect (MTTD) by 40% and enabling rare human analysts to concentrate on strategic investigations and threat-hunting activities. The O’Reilly 2024 State of Security Survey shows that 33% of companies do not have enough AI-literate personnel to fend off adversarial-ML attacks, therefore highlighting the need for automatic defenses. Embedded machine learning for anomaly detection and prioritization not only improves detection capabilities but also provides directed remediation steps, therefore expanding the influence of already-existing security teams.

AI In Cybersecurity Market Restraints and Challenges:

The problems related to the privacy of the data and the existence of model bias are major market challenges.

AI-driven cybersecurity systems use enormous amounts of telemetry, network logs, endpoint activities, and application events to train anomaly-detection and threat-prediction algorithms. AI systems can, however, grow blind spots that either miss real threats or produce too many false positives if the underlying data is incomplete, obsolete, or skewed towards benign activity. A recent Varonis analysis of 1,000 corporate settings revealed that 99 percent had exposed sensitive data that AI could surface, emphasizing both the risk of data leakage and the difficulties of compiling representative training sets. Moreover, source‑data bias, that is, under‑sampling attacks on particular geographical areas or device types, can result in discriminatory outcomes whereby less‑represented assets get fewer protections. To reduce these risks, companies are making significant investments in data‑lineage tracking, fairness‑aware machine learning frameworks (e.g., adversarial‑debiasing algorithms), and synthetic‑data augmentation pipelines.

The problems related to explainability and regulatory trust are major hurdles for this market.

Often acting as "black boxes," deep learning models, especially huge transformer and convolutional‑net architectures, generate threat scores or mitigation recommendations without clear explanations. Still, internal risk committees and regulators (GDPR "right to explanation," CCPA audits) want understandable decision paths for any automated activity affecting data access or incident response. Using Explainable AI (XAI) systems like SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model‑agnostic Explanations offers feature‑attribution insights but calls for extensive instrumentation and developer skill. Incorporating XAI frameworks into cybersecurity systems can increase deployment complexity and licensing expenses by up to 20%, as businesses not only need to use the XAI libraries but also create governance dashboards to convert technical results into auditor-ready stories. Organizations risk regulatory noncompliance, diminished stakeholder confidence, and possible legal exposure without these investments when AI-driven activities cannot be fully justified.

The market faces a challenge in integrating this system with the existing ones, which slows down its operations.

Most businesses still use on‑premises, monolithic security stacks, conventional SIEMs, legacy firewalls, and custom endpoint agents, none of which were created with contemporary AI‑native integrations in mind. Incorporating artificial intelligence modules into these settings requires tailored middleware to ingest logs in nearly real time, standardize diverse data schemas, and transmit improved warnings back into current consoles. According to industry studies, 55% of companies name legacy‑system integration as their main obstacle to artificial intelligence acceptance; projects are usually delayed by 20–30% due to unexpected API gaps and schema mismatches. The need to restructure ETL pipelines, create dual‑write adapters for split‑data flows, and conduct concurrent validation phases to guarantee backward compatibility also adds additional financial burden, projects that might boost integration expenditures by 15–25% and lengthen time‑to‑value over multiple quarters.

The initial investment needed for this market is very high, which makes it less adaptable.

Often requiring specific hardware, GPU or ASIC-accelerated servers able of training and inferencing deep-learning models at scale, deploying a contemporary AI-powered security operations center (SOC) is A case study of a 90‑GPU inference rack shows that standard setups (22 CPU nodes + 88 GPUs) consume 65 kW, whereas optimized fabric solutions (90 GPUs) can lower power to 42 kW, but still require USD 1–2 million in initial CAPEX per rack with annual total cost of ownership (TCO) exceeding USD 0. 5 million. This degree of investment is too high for small and medium businesses (SMEs) and budget‑restricted organizations, hence many postpone or drop AI cybersecurity initiatives. Vendors are investigating GPU‑sharing pools, cloud‑bursting techniques, and AI‑as‑a‑Service (AIaaS) subscriptions to overcome this obstacle; yet even these OPEX‑centric strategies need dedicated minima that can put tight security budgets under pressure.

AI In Cybersecurity Market Opportunities:

The emergence of Automated Threat Intelligence as a Service is seen as a major market growth opportunity.

With a strong compound annual growth rate of 24. 7%, the market for AI-driven threat intelligence (TI) is projected to grow from USD 6.31 billion in 2024 to USD 7.87 billion in 2025 and to reach USD 18. 82 billion by 2029. The rising number of complex attacks and the demand for real‑time, predictive indicators drive this expansion. Managed TI-as-a-Service systems use AI/ML to constantly intake global telemetry, malware signatures, phishing campaigns, dark-web chatter, and enrich it with threat predictions and tactical playbooks. Businesses sign up for these services to balance internal data-collection needs, therefore promptly getting access to selected, practical intelligence. Vendors create recurring revenue streams by means of tier subscription models (e.g., basic feed vs. SOC‑integrated APIs), therefore facilitating fast deployment across distributed security stacks.

The use of AI-powered zero-trust platforms has presented the market with new growth opportunities.

With a 16. 7% CAGR from USD 42.28 billion in 2025 to USD 124.50 billion by 2032, the global Zero Trust Security market is expected to grow. Through continuous, context‑aware risk scoring and behavioral baselining for every user, device, and workload, AI integration enhances Zero Trust architectures. Machine‑learning models examine authentication logs, application usage patterns, and network flows to assign dynamic trust levels—automatically enforcing micro‑segmentation policies when anomalies arise. According to pilot studies, as businesses embrace hybrid environments, AI-driven Zero Trust systems provide a single security fabric that streamlines policy administration and lowers lateral-movement risks and facilitates adaptive policy changes without human involvement by up to 60% improvement in breach containment times.

The recent rapid expansion of OT and IoT security is considered a great opportunity for the market to bring in innovation.

With a 16.5% compound annual growth rate, the Operational Technology (OT) security market is expected to increase from USD 23.47 billion in 2025 to USD 50.29 billion by 2030. Each sensor and actuator becomes a possible attack vector as industrial IoT (IIoT) devices spread in manufacturing, energy grids, and crucial infrastructure. AI‑based anomaly‑detection systems use ML algorithms on real‑time telemetry, temperature readings, control‑loop commands, and network packets to find variations from anticipated "digital‑twin" behavior. Early implementations in petrochemical facilities have identified pump‑control scams with 95% accuracy, hence avoiding operational disruptions. Offering AI‑driven OT security suites as both on‑premises devices and cloud‑managed services, vendors may capitalize on equipment sales and subscription income sources with increasing regulatory pressure on critical‑infrastructure resilience.

The emergence of cross-industry managed security services is said to be a major market development opportunity.

At USD 27.2 billion, and expected to reach USD 87 billion. 51 billion by 2030, growing at a CAGR of 15. 4%. While 70% now provide cloud‑native SOC‑as‑a‑Service, over 48% of MSS providers have already included AI‑based threat detection into their products, therefore lowering false positives by 30% on average. SMEs and controlled industries (healthcare, finance) outsource 24×7 AI‑augmented monitoring, incident response, and compliance management to MSSPs more often to avoid the expensive costs of in‑house staff and infrastructure. This presents MSSPs a growing chance to provide tiered AI‑driven service bundles, combining real‑time analytics, automated playbooks, and regulatory reporting, hence expanding market reach and ensuring predictable, recurring revenue.

AI In Cybersecurity Market Segmentation:

Market Segmentation: By Component

• Software

• Hardware

• Services

The Software segment is said to dominate this market. As businesses embrace ready-made solutions for automated threat detection and reaction, software dominates revenues at nearly 60% via AI-enhanced security software, that is, UEBA, SOAR, and NGAV. The Services segment is the fastest-growing segment, driven by the complexity of artificial intelligence installations and the scarcity of cybersecurity expertise. Managed-security products and professional services (integration, consulting) are growing at roughly 26% CAGR. When it comes to the Hardware segment, it is said to be growing as companies invest in on‑prem GPU/ASIC equipment for model training and inference, which consists of specialized AI accelerators and security devices.

Market Segmentation: By Security Type

• Network Security

• Endpoint Security

• Application Security

• Cloud Security

• Others

The Network Security segment is said to be the dominant one, reflecting the quantity of network telemetry and the urgency of perimeter defenses, AI‑powered network‑security solutions (intrusion detection/prevention, anomaly scanning) control almost 37% of the market. The Cloud Security segment is said to be the fastest-growing one, driven by artificial intelligence, cloud‑security solutions (CSPM, CWPP) are expanding at around 28% CAGR to solve misconfigurations and policy implementation across dispersed systems as multi-cloud adoption picks up pace.

In the Endpoint Security segment, using behavioral analytics, AI-based endpoint solutions (NGAV, EDR) cover around 25% to identify fileless and zero‑day threats. At 18%, application-layer defenses, RASP, and API security protect against OWASP Top 10 vulnerabilities and code injection. The other segment, which has about 10% market share, fills niche use cases including DLP, email security, and identity and access analytics.

Market Segmentation: By Deployment Mode

• Cloud

• On-premises

• Hybrid

The Cloud segment dominates the market. This segment leads the market with a 55% market share due to its rapid scalability, continuous updates, and centralized analytics. The Hybrid Segment is said to be the fastest-growing one. This mode, combining on‑prem agents with cloud analytics, is increasing at about 24% CAGR, so striking a balance between data sovereignty and agility. The On-premises segment is referred to by highly regulated businesses for full control, on-premises solutions, and on-prem AI devices make up approximately 21%.

Market Segmentation: By End-Use Industry

• BFSI

• Healthcare

• IT & Telecom

• Retail

• Government & Defense

• Energy & Utilities

• Others

The BFSI segment is the dominant segment of the market. Driven by compliance requirements and great‑value asset protection, banking, financial services, and insurance lead with around 28% of spending. The Healthcare segment is the fastest-growing one, with around 27% CAGR, as medical data breaches and IoT device vulnerabilities drive artificial intelligence security expenditure.

When it comes to the IT & Telecom segment, the companies are using artificial intelligence (AI) to protect subscriber data and 5G networks. The Defense and Government segment includes public‑sector cyber budgets that support AI‑augmented threat intelligence and critical‑infrastructure protection. Retail companies apply artificial intelligence to e-commerce fraud prevention and POS security. The energy and Utilities segment consists of smart-grid anomalies, and SCADA networks are watched by artificial intelligence systems. Others include manufacturing and education, using artificial intelligence for campus security and OT/IT convergence.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

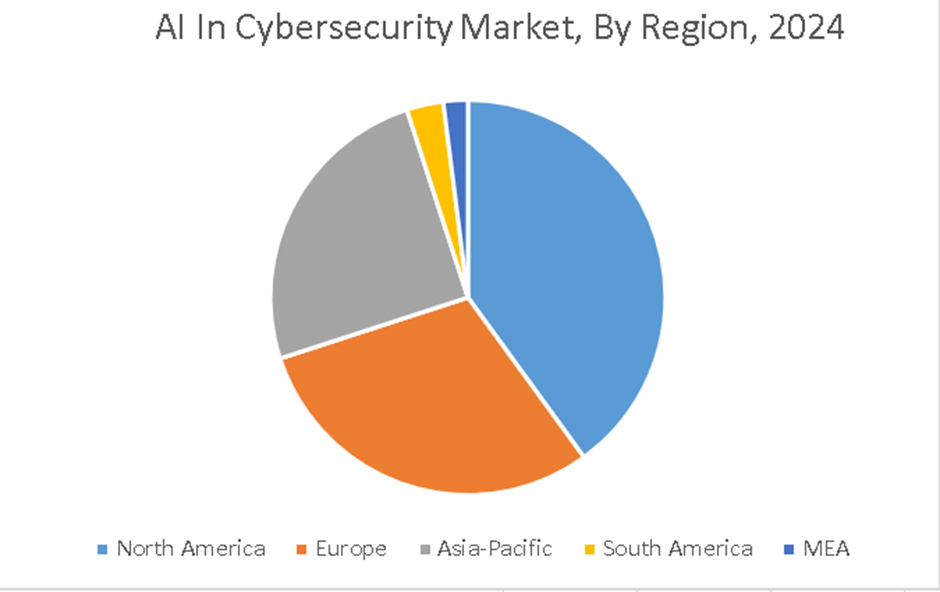

North America leads this market. Early AI adoption, established cloud environments, and strict data-privacy laws help North America lead with roughly 40%. The Asia-Pacific region is the fastest-growing region of the market. Asia Pacific (nearly 25% CAGR), driven by government-led cybersecurity initiatives in China, India, and Southeast Asia, is growing at around 25% CAGR.

Europe makes up around 30% of the total share. In the EU, Europe's GDPR-compliant security solutions propel significant uptake. South America, with about a 5% market share, growth is fueled by telecom‑security initiatives in Mexico and Brazil, as well as by digital‑transformation grants. Middle East and Africa (about 5% market share). For smart-city and energy-sector safeguards, MEA backs artificial intelligence security.

COVID-19 Impact Analysis on the Global AI In Cybersecurity Market:

As remote work and digital services grew, the pandemic highlighted severe cybersecurity shortcomings. In 2020, phishing and ransomware attacks soared by 300%, therefore speeding the adoption of AI-powered detection and response solutions. Businesses fast-tracked AI SOC automation to manage increased alert volumes and secure dispersed endpoints, which caused a 15% permanent boost in cybersecurity budgets allotted to AI technologies.

Latest Trends/ Developments:

Next‑generation systems employ artificial intelligence agents that hunt threats, launch countermeasures, and change policies automatically without human participation.

Collaborative ML models trained across decentralized data silos, preserving privacy while enhancing threat‑intelligence sharing.

Cross-layer analysis and automated incident workflows are being embedded with artificial intelligence by extended detection and response (XDR) solutions.

Placement of artificial intelligence (AI) managed honeypots and deception grids dynamically adjusts to attacker patterns, raising threat-intelligence collection.

Key Players:

• Acalvio Technologies, Inc.

• Amazon Web Services, Inc.

• Cylance Inc. (BlackBerry)

• Darktrace

• FireEye, Inc.

• Fortinet, Inc.

• IBM Corporation

• Intel Corporation

• LexisNexis

• Micron Technology, Inc.

Chapter 1. Global AI In Cybersecurity Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global AI In Cybersecurity Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global AI In Cybersecurity Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global AI In Cybersecurity Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global AI In Cybersecurity Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global AI In Cybersecurity Market- By Component

6.1. Introduction/Key Findings

6.2. Software

6.3. Hardware

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global AI In Cybersecurity Market– By Security Type

7.1 Introduction/Key Findings

7.2. Network Security

7.3. Endpoint Security

7.4. Application Security

7.5. Cloud Security

7.6. Others

7.7. Y-O-Y Growth trend Analysis By Security Type

7.8. Absolute $ Opportunity Analysis By Security Type, 2025-2030

Chapter 8. Global AI In Cybersecurity Market– By Deployment Mode

8.1. Introduction/Key Findings

8.2. On-premises

8.3. Cloud-based

8.4. Hybrid

8.5. Y-O-Y Growth trend Analysis By Deployment Mode

8.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 9. Global AI In Cybersecurity Market– By End-Use Industry

9.1. Introduction/Key Findings

9.2. BFSI

9.3. Healthcare

9.4. IT & Telecom

9.5. Retail

9.6. Government & Defense

9.7. Energy & Utilities

9.8. Others

9.9. Y-O-Y Growth trend Analysis By End-Use Industry

9.10. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 10. Global AI In Cybersecurity Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Security Type

10.1.4. By Deployment Mode

10.1.5. By End-Use Industry

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Security Type

10.2.4. By Deployment Mode

10.2.5. By End-Use Industry

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Security Type

10.3.4. By Deployment Mode

10.3.5. By End-Use Industry

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Security Type

10.4.4. By Deployment Mode

10.4.5. By End-Use Industry

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Security Type

10.5.4. By Deployment Mode

10.5.5. By End-Use Industry

10.5.6. By Region

Chapter 11. Global AI In Cybersecurity Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Acalvio Technologies, Inc.

11.2. Amazon Web Services, Inc.

11.3. Cylance Inc. (BlackBerry)

11.4. Darktrace

11.5. FireEye, Inc.

11.6. Fortinet, Inc.

11.7. IBM Corporation

11.8. Intel Corporation

11.9. LexisNexis

11.10. Micron Technology, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Rapid market expansion is driven by increasing artificial intelligence-augmented threat actors, the need for remote-work security, and regulatory compliance pressures.

Software leads the market with about 60% market share as businesses embrace AI‑powered security solutions.

Capturing around 55% of installations, cloud provides elastic scalability, less CapEx, and constant updates.

By 300%, COVID‑19 increased phishing threats and sped up remote work security demands, therefore triggering AI SOC automation uptake.

Driven by digital transformation and national cybersecurity programs in China and India, Asia Pacific leads at around 25% CAGR.